The outlook for business jet activity is softening in Europe as utilisation levels fall below 2019 levels, notably in Germany and France. The US market is relatively resilient, especially for large fleet operators in the charter and fractional space.

Global

In Week 17 (22nd-28th April), seventy-one thousand global bizjet sectors were flown, down 1% on the previous week, up 4% compared to week 17 in 2023. Part 135 & 91K sectors dropped 2% compared to the previous week, 1% below Week 17 in 2023. In contrast, private and corporate flight departments saw stronger activity year on year. By comparison with business aviation, scheduled flight activity was up 19% compared to the same dates in 2023, 10% ahead of 2019. Cargo operators are 6% ahead of the same dates last year, 26% ahead of 5 years ago.

Chart 1: 22nd – 28th April 2024 activity by sector, compared to same dates last year. (Business jets only)

United States

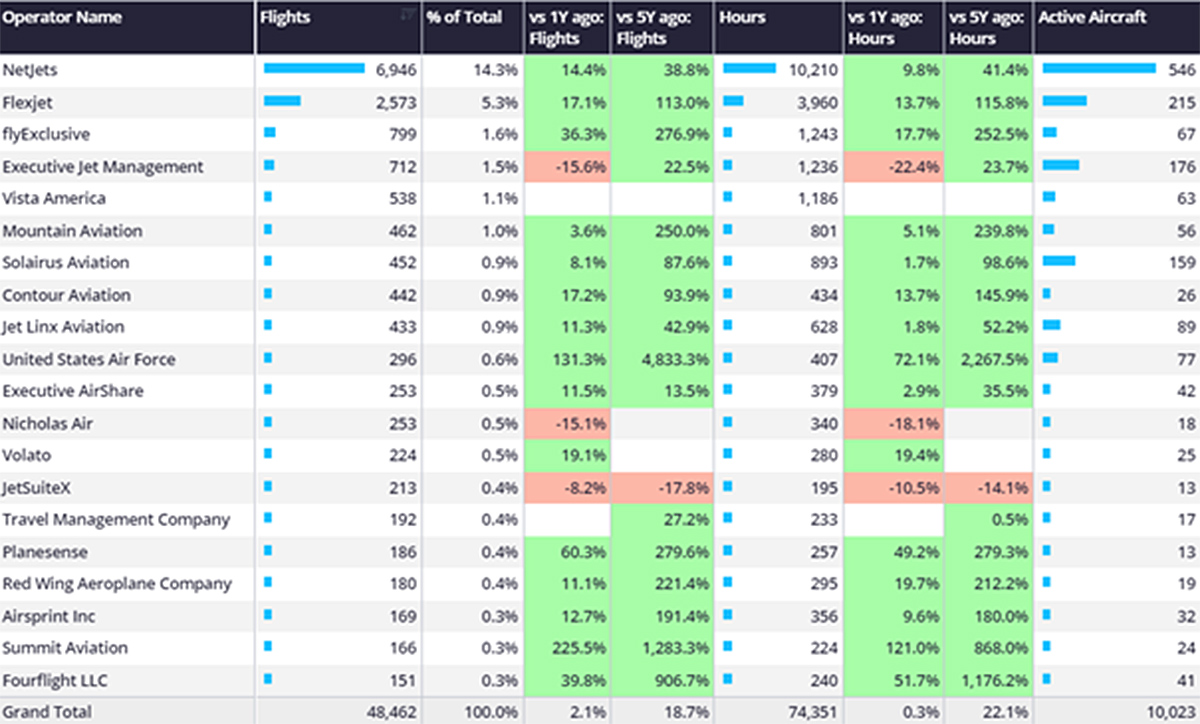

In Week 17, 48,462 business jet sectors were flown in the United States, 2% fewer than the previous week, 3% more than Week 17 in 2023. In Week 17 Teterboro was the busiest departure airport for bizjets in the US, almost 1,400 bizjet sectors were flown during the week. 86% of bizjet flights out of Teterboro in W17 were domestic US, top international connection was with Canada, 76 flights, followed by the Bahamas, 28 flights. Elsewhere across the United States, bizjet activity out of Florida last week fell 3% compared to the previous week, although 10% ahead of Week 17 in 2023. Busiest airport Palm Beach International Airport saw 966 bizjet departures last week, fractional operators accounting for 350 departures out of KPBI in Week 17. Part 135 & 91K sectors fell 2% compared to the previous week, although grew 2% ahead of Week 17 in 2023. 135 & 91K activity in Texas was on par with W16, 5% ahead of W17 in 2023. Florida saw 8% gains compared to W17 in 2023, California 2% declines.

Chart 2: Operator ranking, US bizjets, April 22 � 28th 2024.

Europe

In Week 17, European business jet activity fell 3% below comparable Week 17 2023, sectors down 4% on Week 16 this year. Aircraft on operating certificates (AOC) saw a significant fall in activity, 12% fewer flights year on year, with France, Germany, UK the weakest markets. Relatively, flights by private and corporate flight departments were resilient. Bizjet flights in Italy were down 38% compared to the previous week, although 3% ahead of Week 17 2023. In Italy, between Week 17 and Week 16 there were big swings in activity across the operator types. Aircraft Management fleets flew 240 less flights in Week 17 compared to Week 16, Branded Charter fleets flew 139 fewer flights.

Chart 3: Aircraft Management bizjet flights, Italy, 22nd � 28th April 2024

Trans-Atlantic (Europe � North America) bizjet activity through 28th April was 3% ahead of last year, 13% ahead of comparable 5 years ago. United Kingdom � United States is the top country flow, activity ahead of last year, but dropping 15% compared to 2022. Ireland and Switzerland connections to the US have fallen YOY, Italy, Spain and Germany to US connections are busier than any of the last 5 years.

Chart 4:� European Trans-Atlantic country flows, 1st � 28th April 2024 compared to previous years.

Rest of World

In Week 17, bizjet activity in the Middle East grew 16% compared to the previous week, growing 8% compared to Week 17 in 2023. Charter sectors flown from the Middle East jumped 11% from Week16 to Week 17, although 7% behind Week 17 in 2023. Arrivals of business jets into London from the Middle East are down 15% compared to April 2019.