The recovery in global business aviation appears to have hit a mid-summer ceiling of around 80% of normal activity

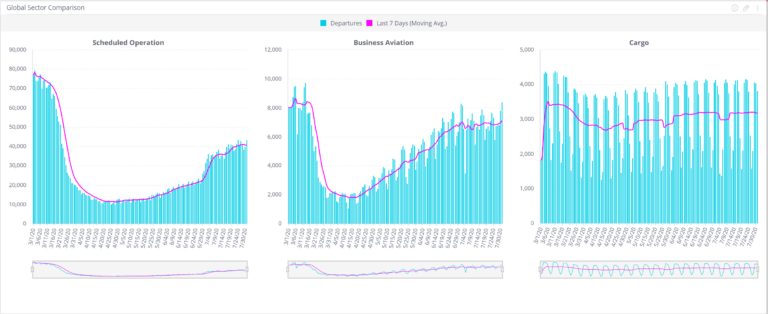

According to WINGX weekly Global Market Tracker, the recovery in global business aviation appears to have hit a mid-summer ceiling of around 80% of normal activity. From July through the first few days of August, just over 23,000 business aviation aircraft operated a combined total of 500K flight hours, 18% shy of the activity for the same period in 2019. The trend hasn´t been smooth, with some relapse in the 2nd half of July, then renewed recovery in the last week. But business aviation still looks in better shape than the Scheduled Airlines, where sectors flown over the same period are still down by almost 60%.

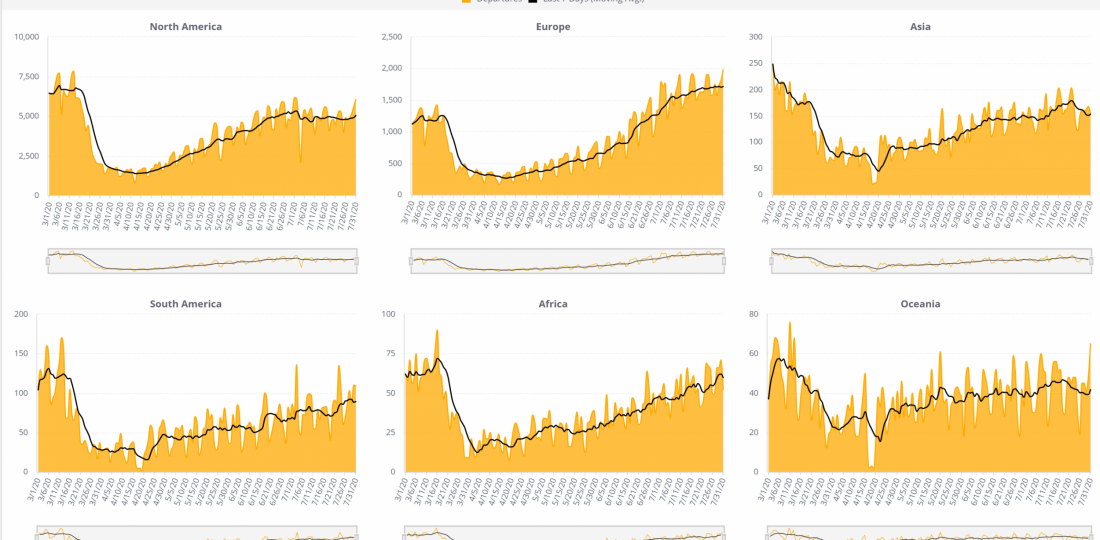

Europe continues to be the region where business aviation is coming back strongest, with July-August trends up to 89% of comparative 2019 activity. The 7-day rolling average daily activity climbed above 2,200 sectors by the end of July, compared to 1,800 at the start of the month, and just 452 in the April trough. The Hungarian and British Grand Prix events were two markers for the resumption of high-end travel. Both events limited fans´ attendance, so big drops in YOY arrivals would be expected, but in fact the Hungaroring´s closest 3 airports saw a 5% increase in business aviation flights compared to the 3 main race days last year, whilst flights into Silverstone´s closest 3 airports were only 9% down on 2019.

Regionally, Central Europe is seeing strongest recovery, with Germany slightly up YOY, flights from Austria and Switzerland around 5% up compared to last year. Croatia and Belgium are two other outliers trending above 2019. Core markets like France are in much better shape, flights within 10% of normal levels. Unsurprisingly, Spain´s early month recovery was reversed as virus-related travel restrictions were reintroduced, flights now trending 3% below normal, arrivals faltering by 10% in the last 7 days. Italy, UK and Greece are seeing gradual recoveries, with activity around a third below par. Much more robust recoveries are coming through in Turkey and Russia, also Netherlands, all within 5% of activity for last July and August.

In contrast, the recovery in business aviation activity in the US has lost some ground recently. A month ago, trends were coming within 15% of usual, now they´re more than 20% behind. For the first time since the pandemic struck, Florida is no longer the busiest US State, and its YOY growth trend, resilient through June and July, is now close to flat. That will undoubtedly worsen as the tropical storms hit. California and Texas are the bellwethers, and both are around 80% of normal in terms of sectors flown since start of July. Colorado and Arizona appear to be thriving as getaway destinations, with flight hours operated in and out trending at least 5% above July-August 2019. At the other end of the spectrum, East Coast States like New York, New Jersey and Illinois are still around 30% behind normal activity.

Outside the US and Europe, there are mixed trends in other regions, with flight activity in Africa still in the doldrums, Asia stabilised around 20% below par, Oceania maintaining a 5% delta, South America keeping head above water. There is a lot more variation within these regions: Middle East flight activity is well behind par, but UAE is bucking the trend with strong growth; within South America, Brazil and Colombia have strong growth; across Asia and Oceania, activity out of Chinas is hovering at just under 85% of usual, and whilst Australia and New Zealand have been solid recoveries the last few months, their flight activity is now starting to erode.

No sign yet of the 4-month trend in preference for lighter aircraft over heavier jets; global Very Light Jet traffic is at 95% of last summer´s flight activity, with the larger Light Jet segment operating 12% below normal since start of July. The Super Midsize segment is competitive at 19% under, with Midsize aligned to the overall market delta of 21%. Heavy Jet activity is trailing by 30% this summer, Ultra-Long Range jet flights down by 35%. The PC-12 continues to be strongest performer, flying 37K sectors since July 1st, activity trailing 11% YOY. The Challenger 300/350 and Phenom 300 are the go-to business jets, activity some 15% off normal. Busiest heavy jet is Challenger 600, sectors down by more than a quarter.

Richard Koe comments: “The mid-summer comeback in business jet activity has been weaker than anticipated due to the stop-start lockdowns in the US. In particular, the East Coast is still in a slump, and Florida, the recovery engine so far, is now spluttering. Europe is doing much better, but with similarities, with rapid recovery in Spain now offset by renewed restrictions, the UK still in a mire, and only Central Europe showing strong pent-up demand. August usually sees a lull in the US market so we don´t expect a turnaround there in the next few weeks, but leisure demand in Europe should continue to boost the charter market over here. The missing piece is the corporate market, and we will probably need to wait until the Autumn to see how the business traveller adapts.”