Ninety thousand business jet and turboprop flights have been operated in the first 8 days of September, 8% decline versus same period of September 2019

Ninety thousand business jet and turboprop flights have been operated in the first 8 days of September, 8% decline versus same period of September 2019, a deficit of around 7,000 flights.�Comparing the last 8 days with comparable 2019 days, the delta is twice as large, just under 16% YOY, according to WINGX`s weekly Global Market Tracker, published today.

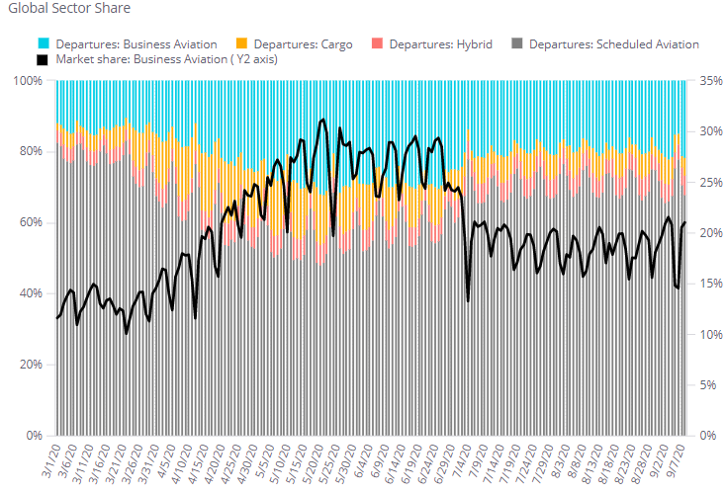

The most recent rolling 7-Day average is 11,273 daily flight departures, down from the post-March high point of 11,728 flights, but well above the April trough of 3,500 flights per day. Since March 1st, global business aviation flights are down 35% compared to last year. This trend is still far more resilient than scheduled aviation, 64% behind last year’s activity since March, and still 57% off so far this month.

The 7th of September marked Labor Day 2020, the TSA noting the largest number of scheduled passengers handled at US airports since March, even though less than half the usual volume. Business aviation activity, for the comparable Friday to Monday, was down by 16%, a drop of 5,000 flights. Flights within the US over the 4 days were down 19%, connections with Canada were down 65%, Mexico only 4% off, and there were big YOY increases in flights from the US to Bahamas, Turks and Caicos. A handful of US States saw some increase in flight activity during the holiday: Idaho, Oregon, and significant growth for Montana, and Virginia. At an airport level, biggest YOY increases were recorded at Salt Lake International, Dallas Love Field and Denver Centennial.

In Europe, where just under 20% of worldwide business aviation flights have operated this month, the August surge has given way to a decline as the summer ends. Comparing 1st through 8th of September, jet and prop flights are down by 3.5%, 9% down on a comparable day basis. In contrast, scheduled aviation activity is down 56% in Europe so far this September. For business aviation, this month is seeing a relapse in activity from top market France, and a slump in flight activity from the UK and Spain, respectively 18% and 24% adrift of September 2019. Flights from Germany are down just 1% so far this month, but in contrast to double-digit growth in August. Austria has so far sustained its summer YOY growth, and Croatia still benefits from late summer leisure travel, but arrivals into Greece are down by 13%. The biggest YOY growth trends are apparent in Turkey and Russia.

The busiest airport in Europe is, as usual, Le Bourget, but activity is trending down 22% for September. Likewise, there are now steep declines for Nice, with Geneva also seeing the end of its late summer surge. Farnborough and Luton are still trailing by 20%, in contrast to Biggin Hill, which has carried its record August activity through into September, flights up by 15% in the first 8 days of the month. Vnukovo, Olbia, Munich, Ataturk and Vienna are other airports with large gains compared to September 2019. In terms of connections, international flights have seen the biggest slowdown, with Italy-UK one of the few exceptions. Domestic travel is still showing some buoyancy, with growth in bizav flying within Germany, France, Sweden and Italy. Flights within the UK are down by 13% YOY.

North America, with declines in both Canada and Mexico steeper than in the US, and Europe, are easily the worst-performing global regions for bizav activity in September. Other regions, which capture less than 10% of total business jet sectors, are stable or above 2019 activity levels.

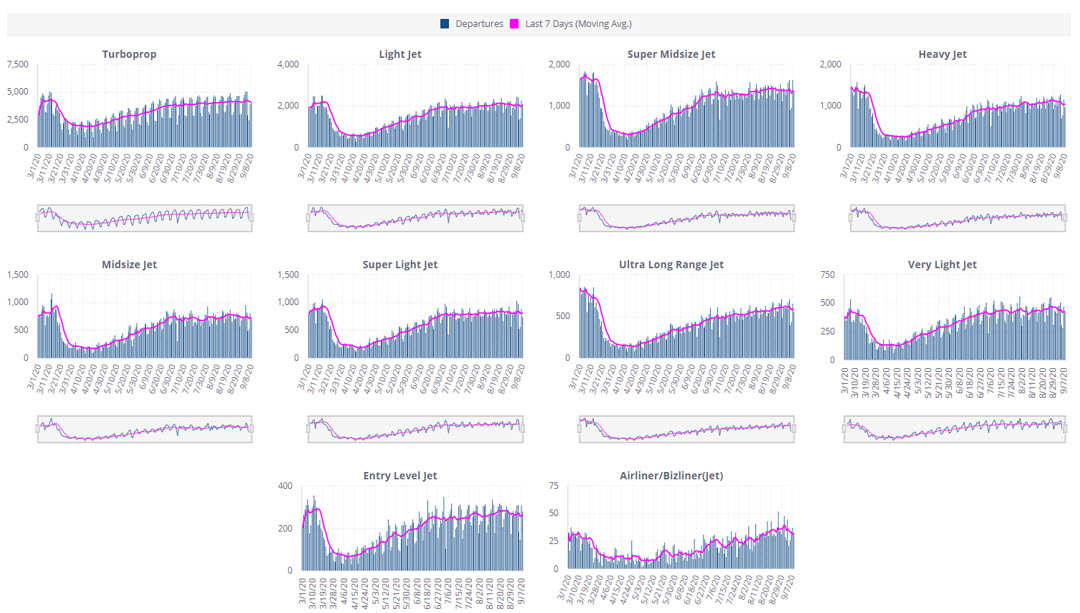

In terms of fleet application, 91% of last year�s globally active fleet has flown so far this month. Light jets are the motor for the recovery, 28% of all sectors flown and at 98% of September 2019 activity. Very Light jets are also in demand, 3% under par. In Europe, Citation Mustang flights are up by 9% so far this month. It�s still a very different story for the large cabin jets, with Heavy and Ultra Long-Range Jet sectors down by over 20%. Gulfstream 600/650 activity is down 18%, Falcon 900 sectors down by 30%.

Managing Director WINGX Richard Koe comments:“Predictably, the end of the summer holidays saw a drop-off in leisure flying and, with scant corporate travel to make up the difference, overall business aviation flight activity has already started to soften in September. The resurgent virus has pushed governments into slowing, and in some cases reversing the opening of the economy, and the result is likely to be a deterioration in further demand as the month goes on.�It´s still an open question how much of the corporate travel demand which remains is able and willing to switch from scheduled to business aviation.”