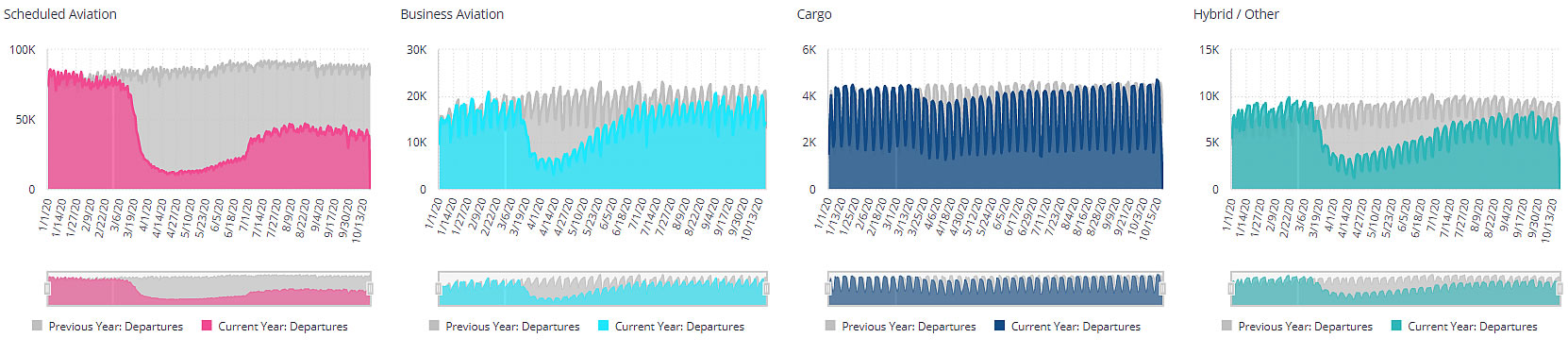

Global business aviation activity is down by 16% in the first three weeks of October 2020 compared to same period in 2019

Global business aviation activity is down by 16% in the first three weeks of October 2020 compared to same period in 2019, according to WINGX`s weekly Global Market Tracker published today.

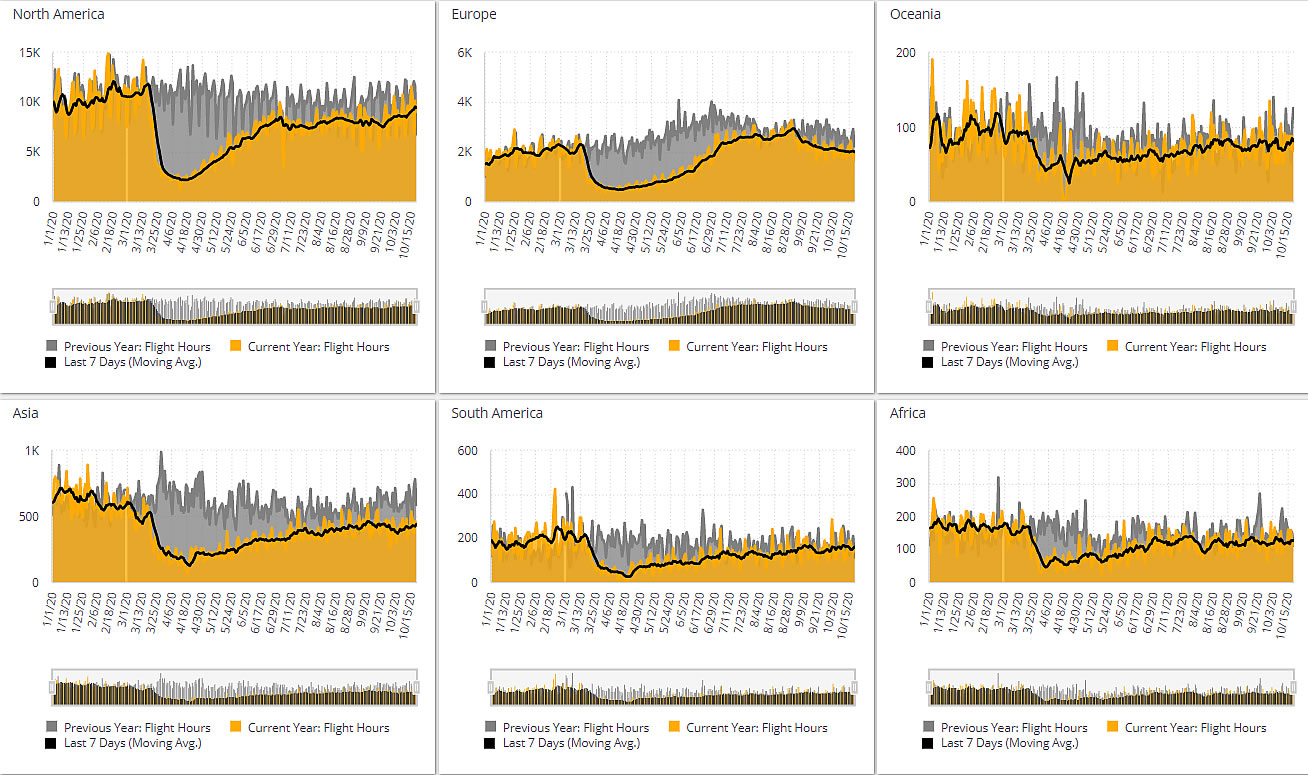

The trend remains far more resilient than for commercial airlines, which have seen a drop of 57% in October YOY, a deficit of 933,000 sectors vs October 2019. Year to date, the respective bizav and airline trends are 24% and 52% deficits vs 2019. Regionally, Europe has stronger trends in business aviation than the US, but this month they are converging as Europe weakens and the US modestly improves. Asia is relatively stable at 10 points below normal, whilst flights out of Latin America and Africa are trailing some 20% below normal.

Europe

As virus concerns mount, European business jet activity has slipped back as October progresses. As predicted, leisure demand is dimming, and corporate travel is not yet coming back to the market. Rolling average trends in sectors flown have declined 5% during the first 3 weeks of October. Flight hours are down by 17%, and for sectors over 3 hours, activity is down by 33%. For these longer sectors the decline has been most severe from Spain, United Kingdom and France, over 40% in October 2020 compared to October 2019. There are some exceptions, with October YOY growth in long sectors flown to and from Turkey, Cyprus, Greece, Portugal.

Shorter sectors, less than 3h, are most robust, less than 10% decline in the first 3 weeks of October. Some countries have seen an increase YOY in these sectors, notably Italy, Turkey, Austria, Russia, Sweden. Whereas from France and Spain, even short sectors are trailing by over 20%, and from UK and Netherlands, more than 40% drops. The UK is now the European backmarker, flights trending down by 32% in October YOY, and by 41% for the period since March this year. So far in October, the London area has the biggest decline in bizav, with Luton activity down by 50%, Farnborough by 37%, Stansted by 33%. Biggin Hill and Oxford are the outliers, both airports seeing growth in YOY activity this month.

North America

North America, including Canada, Mexico, and the Caribbean, is maintaining trends over the last couple of months, flights down by 16%. There is considerable divergence, with Mexico still 50% below normal, similarly severe declines for Bermuda, Bahamas, and other parts of the Caribbean. The US, with an 88% share of regional flight activity, has an October activity trend of -14%, with a small but consistent improvement coming since September. Charter demand is buoying the market, with branded charter sectors down by only 7%, and charter hours up YOY vs October 2019. Fractional operations are also improving, activity down 5% this month. The big decline is in Private operations, which also includes corporate flight departments. This points to well-known weakness in business travel.

Regionally in the US, the varying pattern of activity favours a few States, with flights out of Florida up by 9%, Colorado getting 20% more visitors this month vs last year. Arizona, South Carolina and Oregon are also seeing more bizav activity YOY. California is inching back to normality, with flight sectors down by 10%, half the deficit we saw in September. The North East US is also finally improving, with flights out of New York down by 13%, flight hours down just 4%. New Jersey remains a backmarker, flights down more than 40%.

At an airport level, regional trends are reflected at Teterboro, still the busiest airport, but flights trending down 54%, Dulles trailing by 37%, McCarran likewise, This contrasts with strong growth in YOY business jet and prop departures from Florida’s leading airports Palm Springs, Miami-Opa Locka, Naples. Scottsdale and Salt Lake City continue their growth and this month Van Nuys is also up.

Rest of the world

Outside Europe and North America, there continues to be a mixed picture, big declines in India, Saudi Arabia, gains for Qatar, Nigeria. China has an increase of 22% in sectors flown this month, although flight hours are still down close to 20%. Across all these countries, the best performing aircraft segments are turboprops and very light jets, activity 10% off. Light Jet activity is down 18% this October, with Midsize activity down 20%. Super Midsize activity has slipped back this month, flights down 34%, but Heavy Jet activity is holding up at 26% below. Ultra-long range jets are flying 34% fewer sectors this month, although flight hours are down by over 40%.

Managing Director WINGX Richard Koe comments:�“Increasing efforts to suppress a winter virus wave are blunting flight recovery in Europe, with some notable country and airport exceptions. In the US, trends are improving modestly, and Florida continues to be the ballast, with charter demand pretty robust throughout the country. Outside the core markets, activity trends are 20% below, with exceptions like China, but even there, flight hours are trending well below last year.”