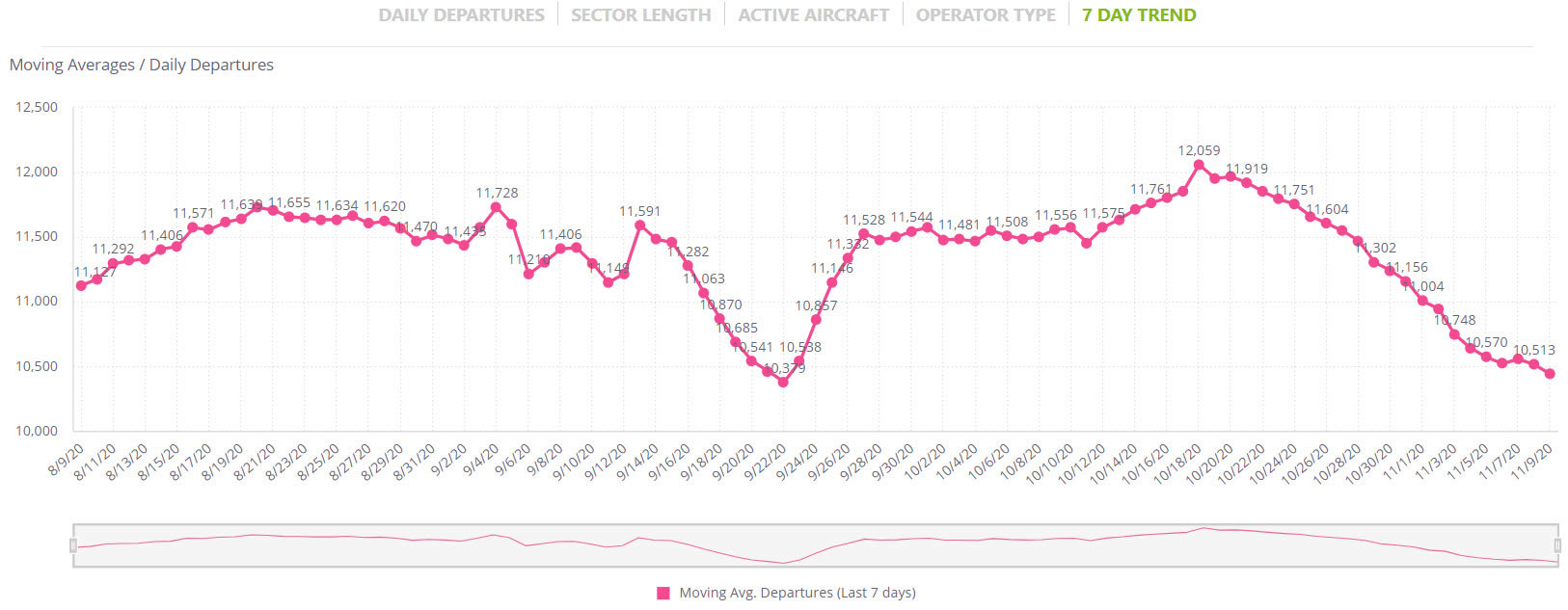

Global business aviation traffic is sliding in November, with moving 7-day average activity at just over 10,300 jet and prop sectors per day coming into 10th November, 10% off the post-March high point in mid-October

Global business aviation traffic is sliding in November, with moving 7-day average activity at just over 10,300 jet and prop sectors per day coming into 10th November, 10% off the post-March high point in mid-October.

According to WINGX`s weekly Global Market Tracker, published today, the YOY decline of 20% for November so far compares to 13% YOY trend in October and reflects the virus resurgence and subsequent travel restrictions in Europe and much of the US. Comparably, business aviation activity continues to be much more resilient than scheduled airlines, with passenger flights stuck at around 50% of normal, worse in Europe. Dedicated cargo operations continue to see more activity YOY, up 20% this month.

Europe

For business aviation, Europe is seeing the biggest relapse in the post-March recovery. Rolling activity trends have fallen each day since mid-October, with flights per day halved since the post-March high at the end of the summer. The formerly robust market in Germany has collapsed this month, flights down by 30% YOY.

The already weak UK market is bumping along at 34% below, with Italy also falling back to this level. Spain has seen some recovery in recent trends, flights at 12% below par. Norway, Sweden and Austria and Portugal are all quite resilient, within 10% of usual. There has been some YOY growth in bizav traffic in Russia this month, and flight activity to and from Greece, Turkey and Ukraine shows double digit YOY improvement for November.

Airports

At an airport level, the busiest hubs appear to be seeing the largest declines in November, with Paris Le Bourget activity collapsing by 53%, Luton down by 47%, and in Germany, Munich’s robust record since March has dissolved with 34% fewer flights. Nice is resilient at 10% below, likewise Biggin Hill, Vienna only 4% down. Vnukovo is the busiest airport in Europe, with 10% increase in YOY activity, whilst in Turkey, Ataturk airport activity is up 50% in November. Both Mallorca and Athens are also up. Across Europe, the charter market is more resilient than the owner fleet, with notably strong YOY growth in charter sectors for the Citation Mustang and Hawker Nextant.

North America

In the US, the solid recovery in flight traffic in October, reaching a post-March high of 8,465 flights a day in mid-month, saw an abrupt decline through the US election period and is 16% down since then, 23% down on November YOY. Charter activity has fallen back to 18% below, although government, ambulance and shuttle traffic is robust. Private and corporate flight departments are worst affected, 30% fewer sectors flown so far in November. The Phenom 300 continues to be the best performing jet, with sectors 8% off for November, and in the charter market, Phenom 300 flight hours are up this month, as also for Citation X, Lear 60 and the Nextant. Popular larger jets are seeing declines, with Challenger 300 down 18%, Legacy 600 sectors down by 30%.

All regions in the US have seen a relapse in recovery trends this month, with even Florida, which has had almost uninterrupted growth since July, seeing a drop-off, 9% fewer flights YOY. Likewise, business aviation flights into Colorado are wo falling, although Arizona and Oregon are still popular destinations. After Florida, Texas and California are next busiest, with 20% declines YOY, same for Georgia and North Carolina. The North East is back in decline, with New York down 23% and New Jersey well over 50% behind this month. At the airport level, the relapse is stark at former bizav hub Teterboro, where flight activity is trending more than 60% behind. Some airports continue to see resilient bizav activity, with double-digit growth this month at Naples and Scottsdale airports in the last 10 days.

Rest of the world

Business aviation flight trends are slightly stronger in regions outside the US and Europe, 14% lower than November 2019, although flight hours are almost 20% below, most severe in long-sectors, which are down by 40%. Turboprop activity is quite resilient especially in Canada and Australia. Business jet activity is up this month in China, India, Brazil, UAE, Nigeria, Indonesia. There are big ongoing declines in business jet activity in Canada, Mexico, Saudi Arabia, Bahamas.

Busiest business jets in these countries are large cabin in including Challenger 600 and Global Express, both within 20% of normal activity, and Legacy 600, flights up 30%. In contrast, Phenom 300 activity is down 30%.

Managing Director WINGX Richard Koe comments:�“Business aviation activity is on the slide as lockdown 2.0 suppresses the recovery in Q3. With corporate travel at a standstill and the leisure market out of season in the US and Europe, the month ahead looks bleak.�The vaccine news may help to brighten the longer-term outlook, and the bizav industry could find a big opportunity in providing ad hoc cargo for vaccine distribution.”