Following a surge in business jet demand over the Christmas holiday period, the year-on-year trend in global flight activity came in around 11% below December 2019

Following a surge in business jet demand over the Christmas holiday period, the year-on-year trend in global flight activity came in around 11% below December 2019, the best comparative performance since the Pandemic broke out, according to WINGX`s weekly Global Market Tracker. At its peak of just over 12,000 flights on December 23rd, the rolling 7-day average daily activity surpassed the previous post-March high point. By contrast, scheduled airline traffic was down by 48% this December. Since the pandemic, scheduled passenger movements are down by 63%, whereas business aviation – jets and props � flew 29% less than in 2019 over the same period. Global cargo operations are up by 6% since March and trended up by 16% in December YOY.

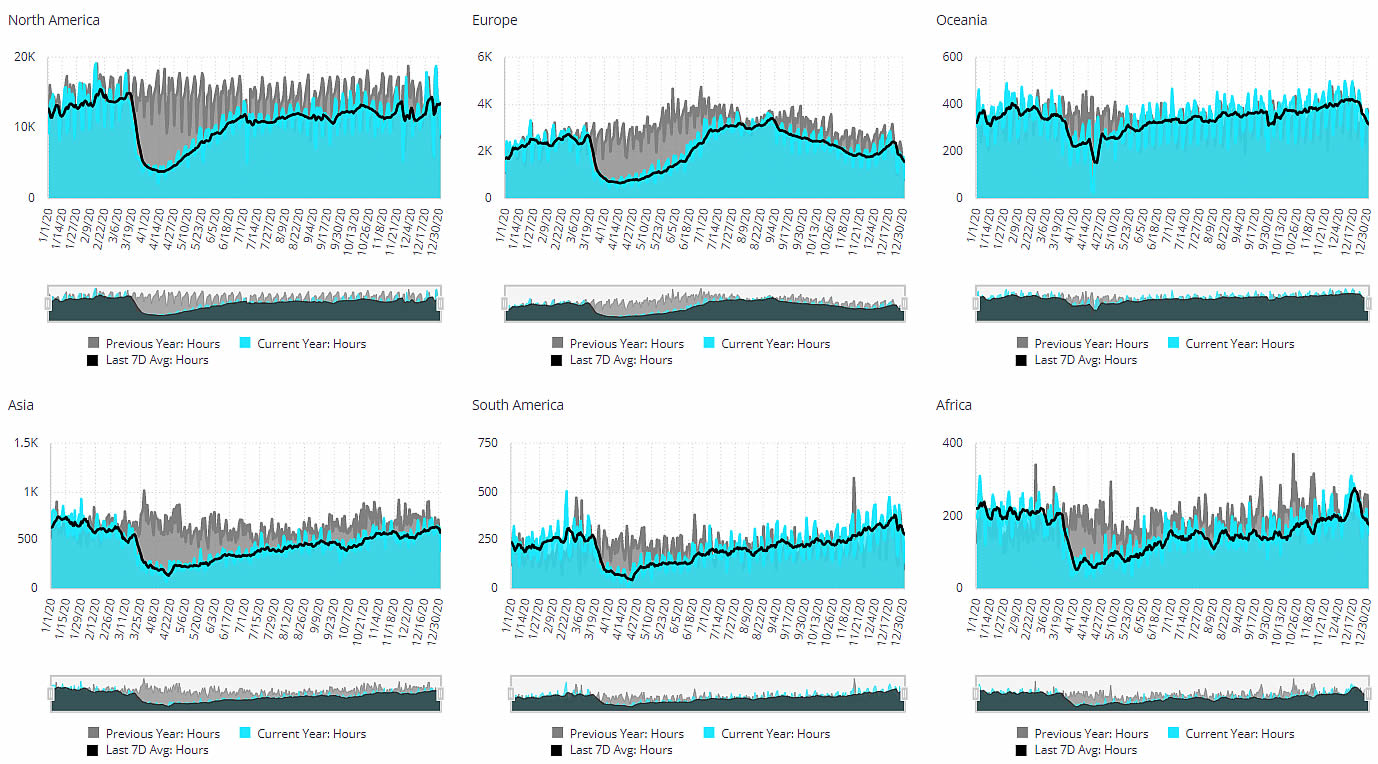

Two thirds of worldwide business aviation activity in December originated in the US, these flights down by 10% YOY, an improvement on the 16% YOY decline in November. Charter activity continued to be robust, sectors down by 7% YOY, branded charter flight hours up by 2% YOY. Aircraft Management operations were also robust, just 6% off, inflated by 3rd party charters. Private operations are lagging, 17% below normal, largely due to still-idle corporate flight departments. On a geographic basis, Florida shone as the busiest State, with 12% more flights than in December 2019. Flights into Arizona were up by 10% YOY. California is the laggard, where continued lockdown measures have suppressed recovery at 80% of normal. Texas got a lot closer to recovery in December, departures down by 6% YOY.

The driver for the Christmas holiday surge from the US was clearly demand for getaway locations. Flights from the US to Mexico were up by 17%, and other Caribbean destinations saw a major rebound in US tourists: arrivals into Turks and Caicos were up 41%; 15% up to Sint Maarten; 32% growth to Costa Rica; almost 70% growth in flights to Antigua and Barbuda versus December 2019. Departure points were strongest from airports in Florida, with Naples, Miami-Opa Locka and West Palm beach all seeing more than 20% increased activity YOY, Scottsdale business aviation departures up by 30%, Salt Lake getting 19% more arrivals than in December 2019. Teterboro still managed to be the busiest airport for business aviation in December, but departures are tracking 45% less than normal.

In Europe there were 40,000 business aviation sectors operated in December, some 6,000 fewer flights than in December 2019, a drop of 13%. As with the US, this marks a rebound on 20% declines in November, regaining the recovery path in October. The resilient sector is Charter, with branded charter operators flying 7% below normal, but up 1% in hours. Private operations, mainly aircraft owners, were also resilient, more than 90% of normal. Cargo-specific business aviation aircraft were 18% busier than last year. The growth didn´t come from the leading markets; Departures from France and Germany fell close to 20%, Italy down 25%, UK down 30%. The market was buoyed by Spain, Russia and Turkey, respectively up in terms of flights by 1%, 5% and 20% YOY. Flights within Turkey were up 25%, and there was also strong growth in connections from Turkey to Russia, UK, Albania, Greece.

At the airport level, across Europe, the busiest airport in December was Le Bourget, but activity was down 29% YOY, with Linate, Ciampino, Munich equally weak, and Luton standing out at 40% fewer departures YOY. Farnborough and Geneva continued to stagnate 20% below normal, but Zurich and Biggin Hill were both within 10% of last year. The growth came out of Nice, flights up 7%, Vnukovo, departures up 12%, and Ataturk, flight activity up by 40%. The biggest increases came on flights from Moscow to Dubai, St Petersburg, and into Western Europe via Nice and Riga. Flights from Spain to Belgium and Germany were up 50% in December. Further flung connections with growth during the Christmas period included UK to UAE and Russia-Maldives.

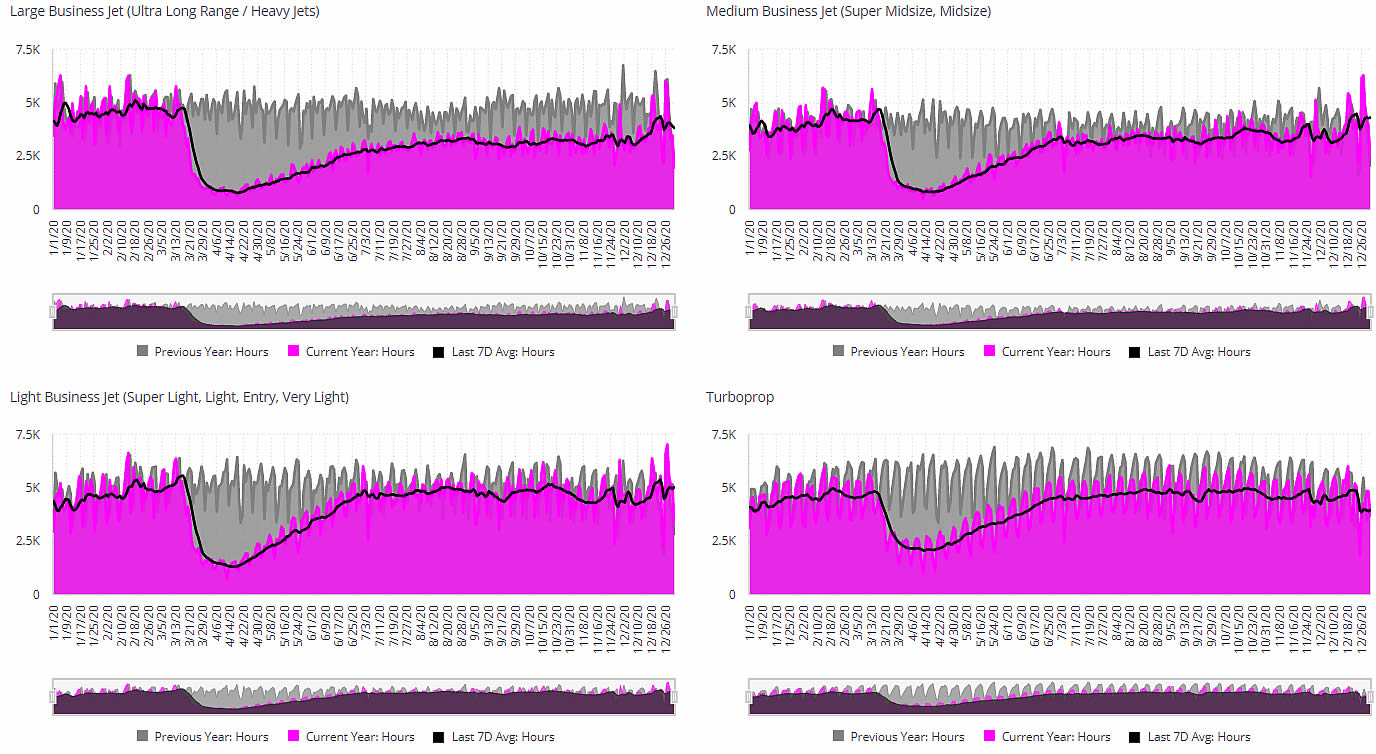

Worldwide, four business jet segments flew more in December 2020 than in December 2019: Very Light Jet; Entry Level; Light Jet; Midsize Jet. Heavy Jets flew 19% fewer sectors YOY, Ultra-Long range jets flew almost 30% fewer hours and Bizliner traffic was down 46%. The Phenom 300 was the busiest light jet, sectors down by 3%, hours up by 7%. Hawker 700-900 aircraft also few more hours, as did CJ1 and Nextant. Demand for Caravan, King Air and PC-12 was pretty close to normal. The Challenger 300/350 flew at 88% of usual, and the Challenger 600 was busiest large jet, activity 16% down. The Gulfstream GV/500 flew 5,400 missions in December, 23% fewer YOY.

Managing Director WINGX Richard Koe comments “The first half of December was stagnant but the holiday period demonstrated the enduring demand for business aviation to reach leisure getaway destinations. This is obvious in the Caribbean for the US market. In Europe, the lockdowns have suppressed this pent-up demand to a large extent, with the ski season postponed at best. In Russia and Turkey, stronger flight activity suggests that business aviation is filling in gaps left by erosions in schedule services.”