Global business aviation activity this April is 221% up versus April 2020, and 5% down on April 2019, according to WINGX`s weekly Global Market Tracker. Since the start of the year, business jet and prop activity is now 10% up on same period for 2020, 9% behind same period in 2019.

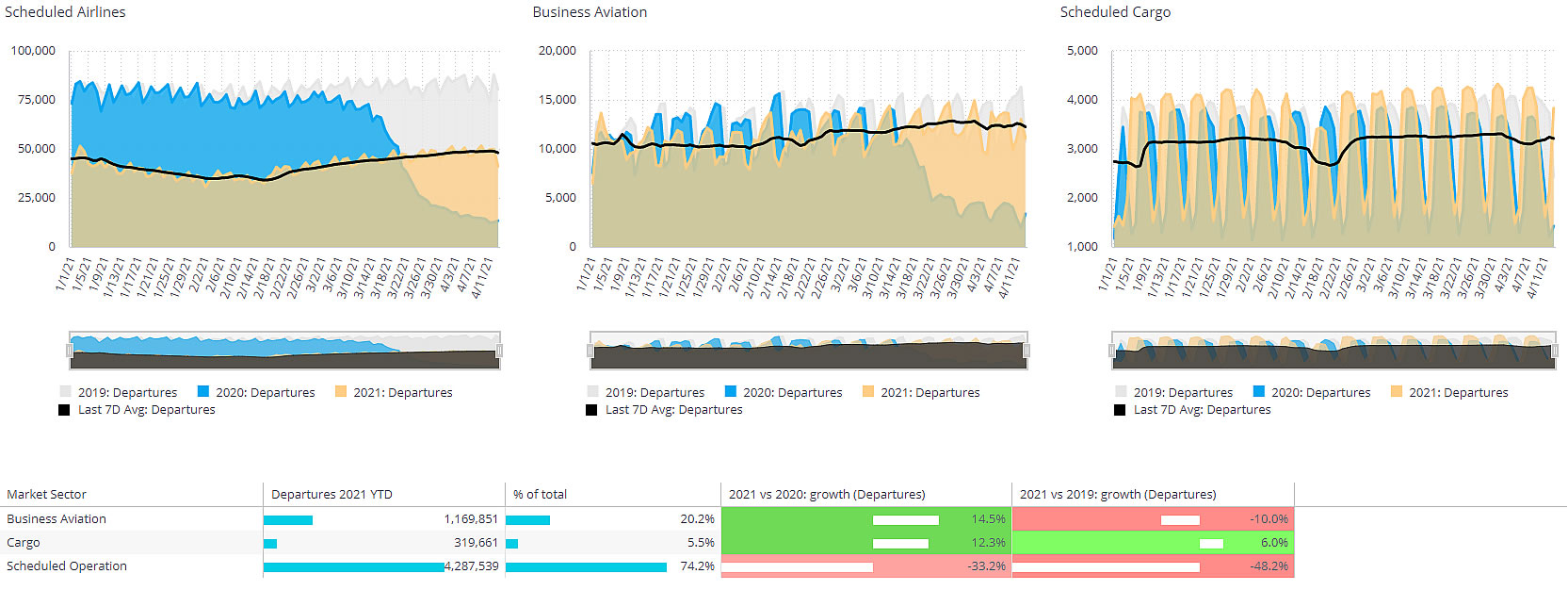

Scheduled airline activity is down by 33% compared to last year, and Cargo operations are 11% up on last year. The airline trends diverge, with Europe 62% down YTD, North America 32% below, Asia 2% up.

Business Aviation: Global 2021 YTD

For business aviation, the US has seen a 13% increase in flights this year to date, contrast Europe which is still 5% down, whilst other regions combined are now 10% up. Compared to the same period in 2019, these trends are respectively -9%, -22% and -4%.

All Market Sectors – Global 2021 YTD

Europe

Europe’s gradual easing of mobility restrictions is showing up in a large bounce in April activity, flights up by 189% in the first two weeks of April 2021 vs April 2020. For the year so far, sectors-flown in the European region, including Turkey and Russia, are down 2%, hours down by 5%.

Non-commercial business aviation traffic has recovered most, Private flights now up 12% this year vs last. Branded charter activity has fallen back severely in 2021, still down 2% on year-to-date 2020. France is the largest market for business aviation activity this year, with 21.8K sectors flown, up by 2% compared to 2020. Flight activity in Germany is still slightly lagging 2020 trends, Switzerland is further behind, 16% fewer flights, and the UK continues to be the backmarker, with 44% fewer flights this year vs 2020.

Other countries in Europe are seeing a stronger recovery this year. Business jet and prop activity is up 13% in Spain, 22% in Italy, 29% in Russia, compared to Jan-April 2020. Flights from Poland are up 12%, from Greece, up 40%, from Turkey, up 63%. Business jet activity out of Turkey is trending 10% higher than same period 2019. This year, Turkey�s domestic activity is up 57%, and international connections have more than doubled with Russia, Albania, Iraq, UAE and Israel, although in contrast, flights from Turkey to Germany are still down almost 20%.

The UK�s business aviation demand is at the other end of the spectrum so far this year, with 53% fewer flights to France, 70% fewer flights to the US. AOC flights from the UK are up 175% this month, but down 43% this year compared to last year.

United States

The US market continues to thrive, with April seeing two and a half times the activity of the first fortnight of locked-down April 2020.

Fractional activity has been particularly strong on the rebound, with more than 5 times� last April�s activity. Year to date, most US States have seen more traffic than comparable 2020, with New Jersey the exception, business aviation departures still off by 9%.

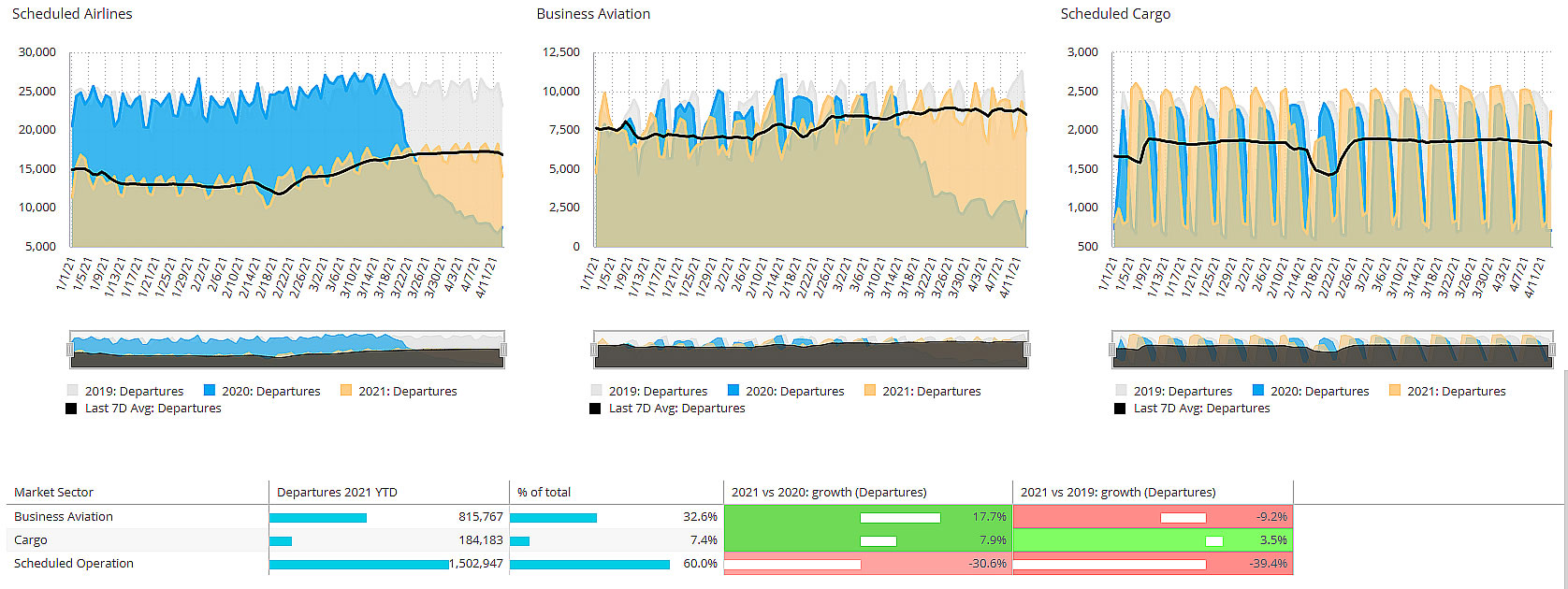

All Market Sectors � USA 2021 YTD

Florida has more than 50% of the traffic of next busiest State, Texas, with flights departing airports in Florida up by 40% compared to 2020. A recent peak of 1,388 flights per day this month compared to high points of 1,185 in 2020, and 1,257 back in 2019. Charter activity in Florida is fully 20% higher than peaks in Spring 2019.

For charter activity, top airports West Palm, Miami-Opa and Naples are up more than 50% this year compared to same period last year.

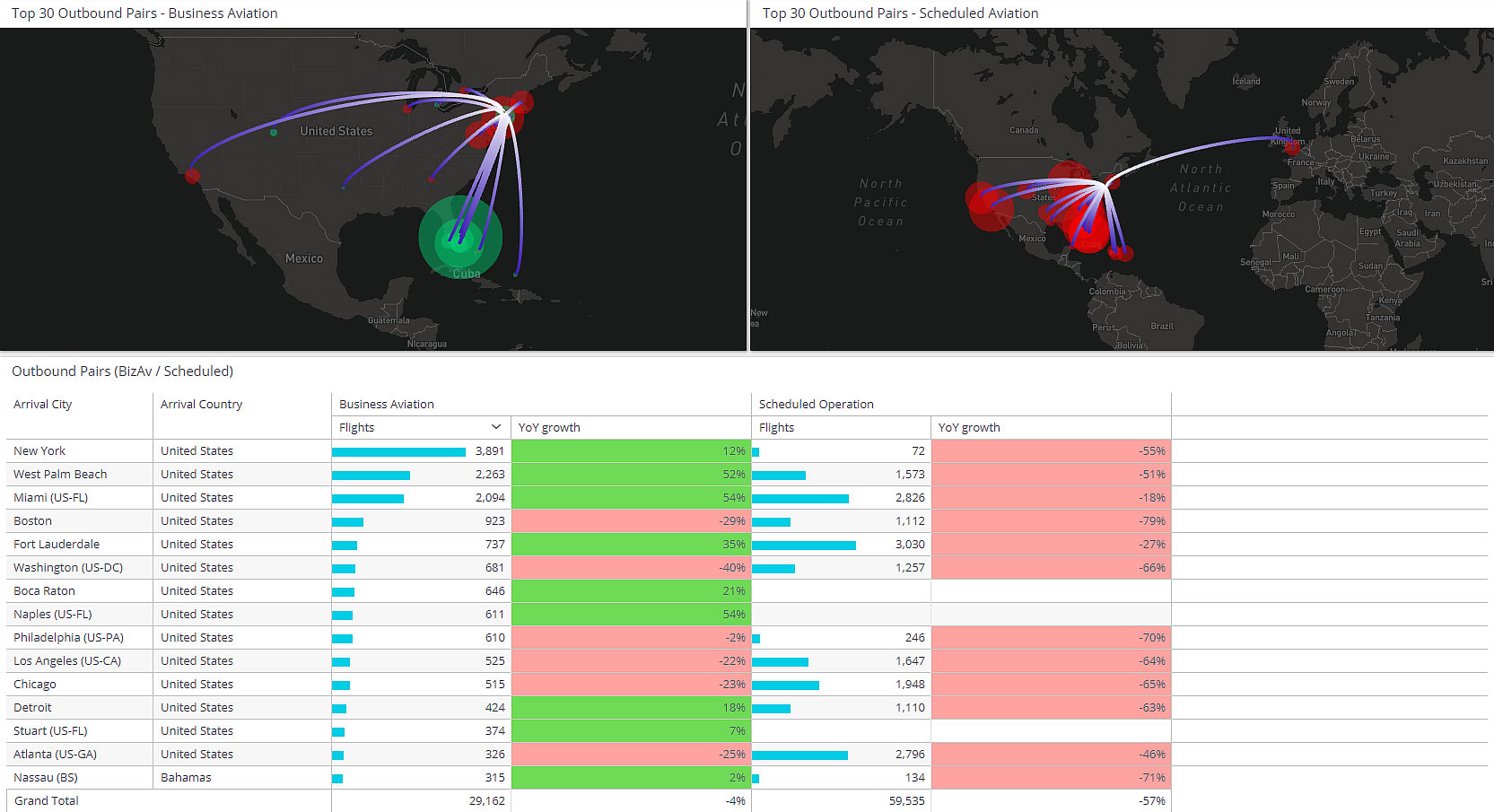

Top Bizav Connections Scheduled from New York State (Jan � April 2021)

Only Nevada has seen less business aviation charter this year compared to 2020. Charters out of California are up 16% and from New York State, up 40%. Country-wide, charter rebound of 25% in 2021 is well above the recovery in non-commercial flights, although these are also up 13% compared to 2020. Teterboro and McCarran are two of the only major business aviation airports still trailing 2020 trends this year.

Larger business jet cabins are seeing the slowest recovery, with Ultra-Long Range jet sectors up 3%, Heavy Jets flying 6% more, contrast Light through Midsize cabins, flying at least 25% more this year. The Challenger 300/350 is the busiest jet platform, hours up 21%. The Phenom 300 has seen a substantial rebound, flight hours up 40% so far this year compared to 2020.

Rest of the World

Outside Europe and the US, business jet and prop activity is now ahead of 2020 trends. Including turboprops, Canada is the busiest country, but still lagging 2020 trends through mid-April. Contrast Australia, where prop activity is some 30% ahead of last year.

For business jet traffic, Mexico is the leading market, 7% up on 2020 through mid-April. Business jet departures in Brazil are now 36% up this year compared to 2020, Bahamas activity up 50%, UAE movements up 95%. Nigeria is the busiest country in Africa, business jet flights doubled year on year, although next busiest Morocco is still behind 2020 trends. Leisure destinations such as Turks and Caicos are popular this year, arrivals up 59%.

Managing Director WINGX Richard Koe comments “Unsurprisingly, the first half of April 2020 is several multiples busier than locked-down April 2020. The longer-term view shows that in Europe, gradual easing of travel restrictions are slowly restoring flight demand, whereas the rapid opening up in various US States has already seen pent-up activity surpass the total for 2020, with all-time record demand coming through in Florida and Texas, particularly in Charters.”