WINGX�s weekly Business Aviation Bulletin.

Overall Comment:

We are now getting to the point where traffic levels in 2021 need to be interpreted versus 2019, gauging return to normality rather than rebound from locked-down 2020. The evidence so far suggests that charter demand in domestic markets, especially the US, may exceed pre-pandemic levels this year. Fractional operators are also starting to do better than ever before in the US. Europe is running behind, but making up ground, especially in leisure demand.

Global:

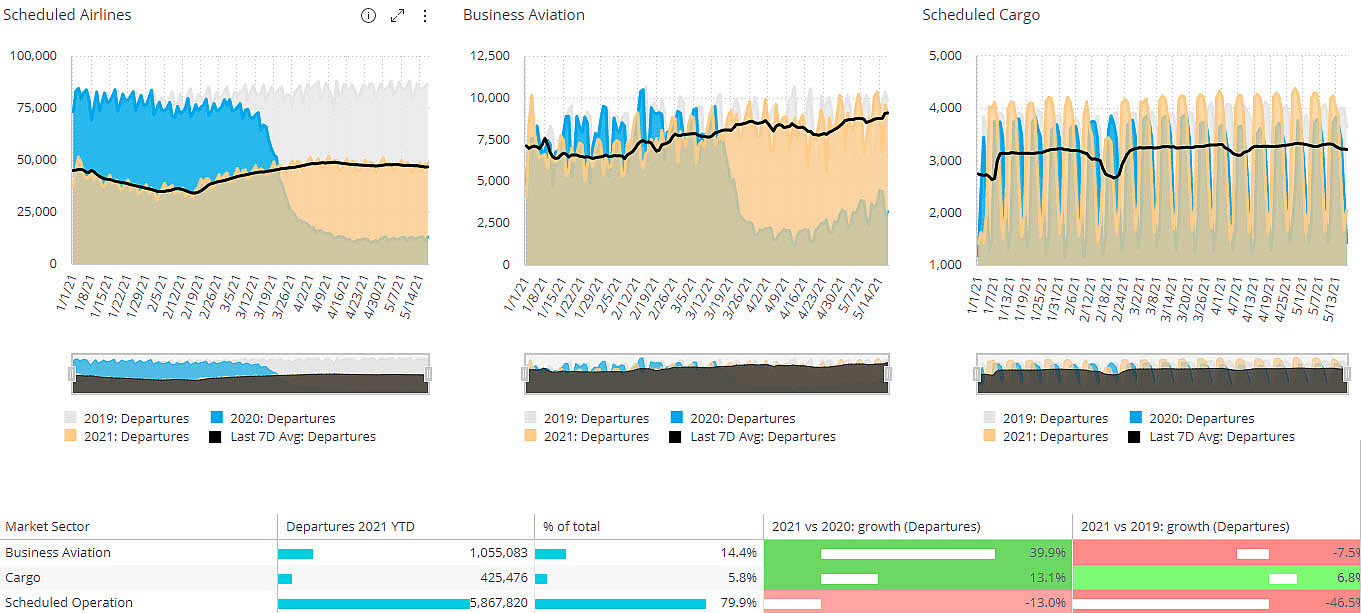

Through the first three weeks of May 2021, global fixed wing activity amounts to just over 1 million sectors flown, with 21% of these operated by business aviation operators, almost double their pre-pandemic share. Business jet and prop flights so far this month are up by 123% compared to May 2020, 5.7% fewer sectors than in May 2019. Cargo traffic is up 9% this month, down 4% versus May 2019. Commercial airline traffic has rebounded almost three times this month year-on-year but is still 45% below May 2019. Year-to-date, business aviation traffic is up by 34% this year compared to last, in stark contrast to the 13% deficit in scheduled traffic this year versus last. Compared to the January through May period 2019, business aviation activity is down by 8.7%.

Global business aviation versus other fixed wing sectors, May YTD vs 2020 and 2019.

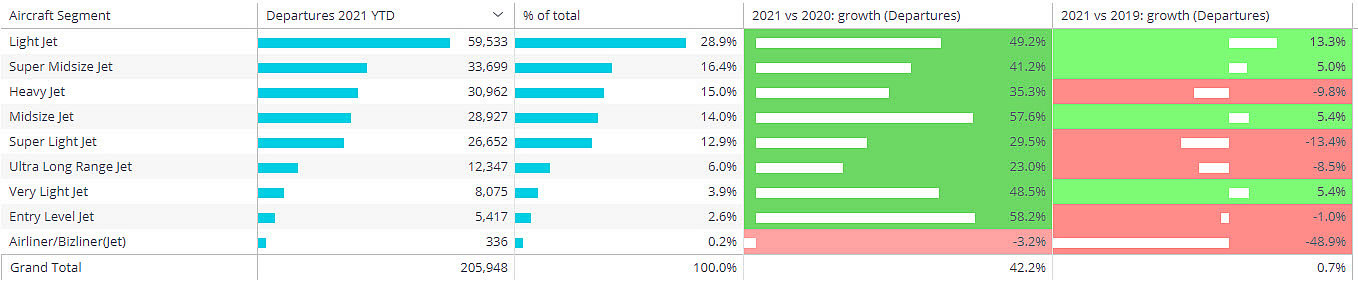

Two business jet types stand out: Very Light and Super Midsize Jets, these segments seeing more activity so far this year than in 2019, respectively 3% and 1% growth in sectors. This growth is accelerating; for just the first three weeks of May, VLJ and SMJ segments are 5% and 7% versus 2019. This month, the combined light jet segments, with 40,000 sectors, is also busier than in May 2019. Large cabin aircraft are still making up historical deficits, sectors down by 10% this month compared to May 2019. The recovery is much stronger for branded charter operators; Light Jet charter sectors are up 23% on May 2019, and Heavy Jets are only 2% below 2019 levels. There is also a lot of regional variation: arrivals of ultra-long-range jets into the Caribbean are up 8% this year versus 2019.

Global business aviation activity May YTD, comparing segments, vs 2020 and 2019

United States

The US market continues to make gains, with business aviation activity this year up by 37% compared to the first four and a half months of 2020. The charter market is hot, with almost 50% more sectors this year than last, and 4% more charters flown than in the same period of 2019. Light jets, including the older entry-level Citation jets, are flying 20% more charters than in 2019. Even Ultra-Long Range Jets are flying more charters than in 2019, up by 8% this year. Compared to the January to May period in 2019, 2021 has seen more than 15% increase in charter flights between the US and Mexico, Bahamas and Turks and Caicos, and 77% increase in charters to Antigua and Barbados. Canada is the outlier, with this year’s charter connections with the US still 59% down on last year, over 70% below comparable 2019.

Europe

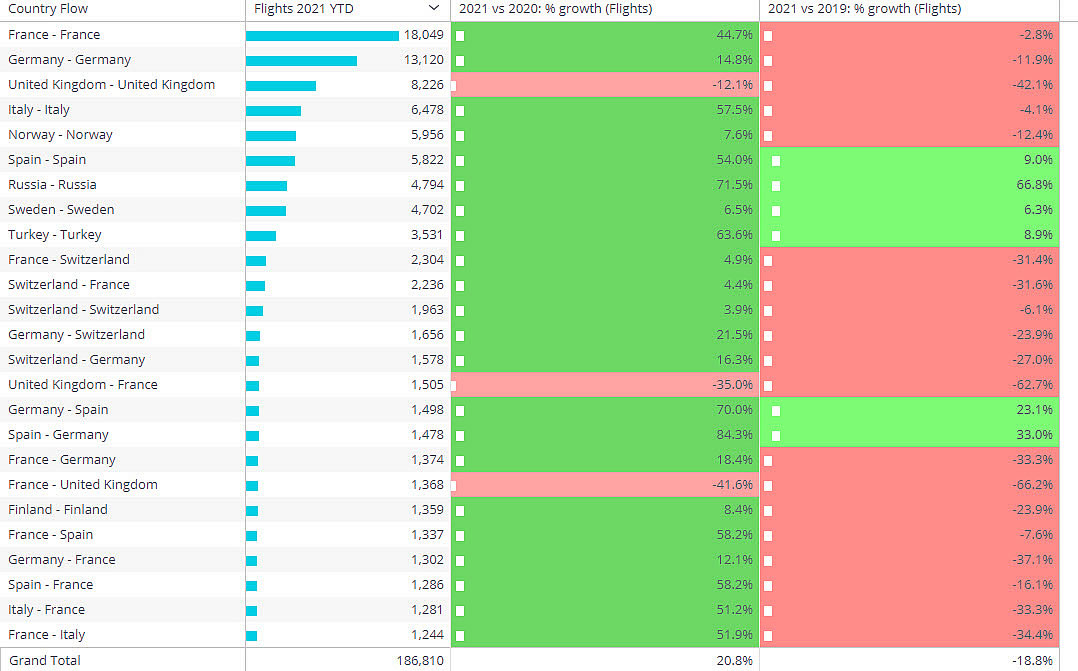

In Europe, branded charter operators are still a way from closing the gap on 2019, 14% below for the YTD, -12% for May 2021. Very Light Jet charters are up 43% this year compared to last year, and even 9% ahead of the same few months in 2019. Overall, the busiest ten countries in Europe are now well ahead of 2020, the exception being the UK, traffic still 20% behind 2020 trends, 40% below 2019 levels. In Western Europe, Spain has seen the biggest bounce this year, business aviation departures up by 60%, and trending 12% up on 2019. The Balearic Islands are the hottest destination, with flights up by 58% compared to same period 2019. Andalucia and Galicia have also seen more business aviation arrivals this year than pre-pandemic. The growth momentum is coming from Germany; business aviation visitors are up more than 25% this year compared to 2019.

Country connections in Europe by business aviation, 2021 May YTD vs 2020, 2019.

Rest of World

Outside Europe and the US, Canada is the biggest domestic market for business aviation, with internal flights up 17% this year so far compared to 2020, but 3% behind 2019. Mexico is the next busiest market for business jet movements, 1% more flights this year than last year but still 50% behind 2019. Brazil and Australia have seen substantial gains this year compared to 2019, and China�s domestic business jet travel have more than doubled compared to 2019. Business jet sectors flown within Nigeria and South Africa are also much higher than pre-pandemic. Other important business jet markets, including Saudi Arabia, Morocco, Indonesia, are still catching up with 2019 trends. Overall, business jet traffic is up 33% outside the US and Europe so far this year versus last, but still 14% below 2019 levels.