WINGX�s weekly Business Aviation Bulletin.

Overall Comment

During the pandemic, lifestyle and occasionally necessity sustained business jet demand, in the last few months we have seen leisure boost the recovery, and this will accelerate through the summer, with the return of at least some business travel taking utilisation to new highs in 2021 compared to 2019. The surge should reliably follow the lifting of restrictions, with international trips waiting longer but almost certainly at the planning stage.

Global

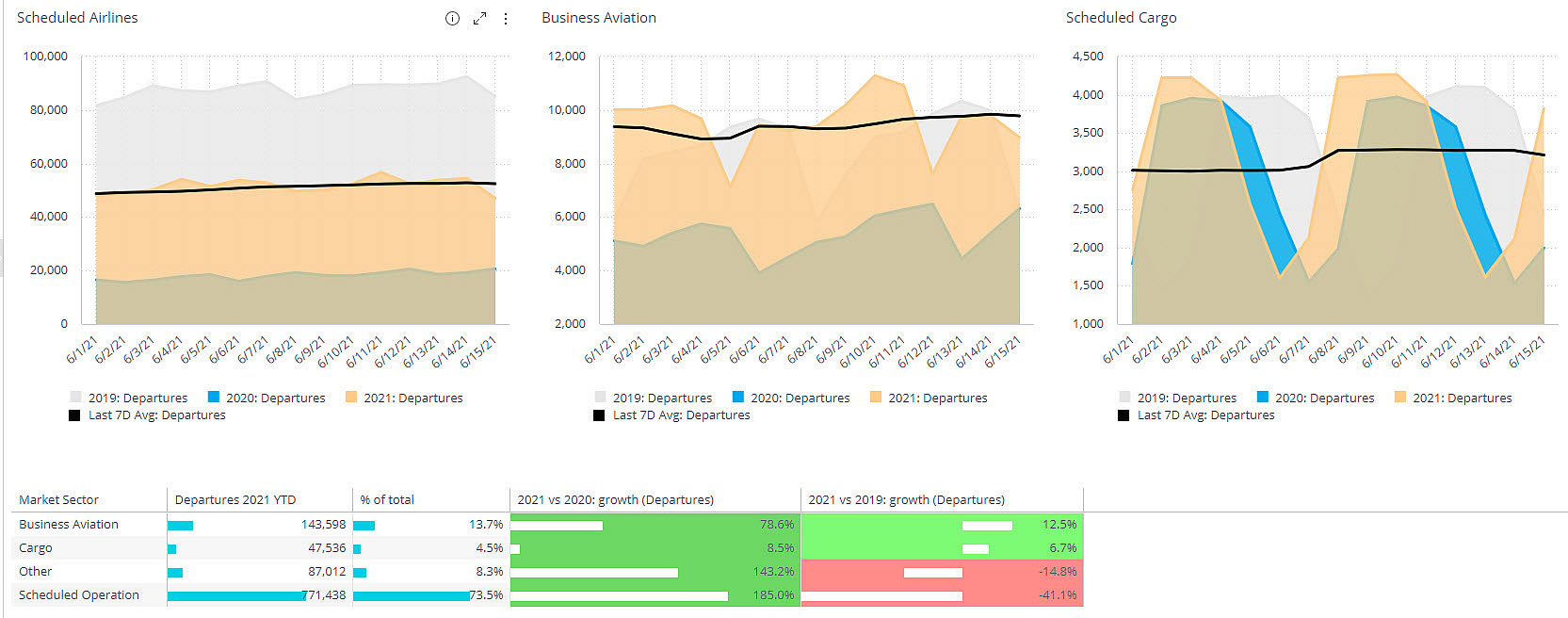

The first half of June 2021 is seeing a surge in business jet activity, rebounding well beyond the recovery threshold with relation to flight trends in 2019. With just over 100,000 business jet sectors flown this month, the sector represents 15% of all fixed wing movements, activity 12% higher than in the first half of June 2019, the first time bizav growth is outstripping Cargo growth. Scheduled airline activity globally is still languishing more than 40% below pre-pandemic normal for this time of year. So far this year global business jet and prop activity is within 6% of 2019, rebounding 41% above YTD 2020. Comparably, passenger airlines are just 1% ahead of the first half of 2020, still just under 50% shy of 2019.

Global Scheduled Airline, Cargo and Business Aviation activity Jan through June 15th, 2021

Geographical differences abound, with European business aviation activity trailing 2019 by 15%, flight activity in Asia 10% ahead of 2019, 45% ahead in Africa, 80% ahead in South America, 23% ahead in the Middle East, 7% behind across North America. There is also considerable variation in activity by aircraft type, with Turboprop activity aligned with overall trends, 7% fewer sectors, but Light and Very Light jets flying more than in 2019, same with Super Midsize Jets. Super Light and Midsize Jet activity is also close to normal, with much more substantial deficits for large cabin aircraft, Heavy Jet hours down by 13% this year, Ultra-Long-Range Jets 27% down on comparable 2019. The link between range and travel restrictions is clear; globally, domestic sectors are back to where they were in 2019, whereas international business jet sectors are still down by 20% vs 2019.

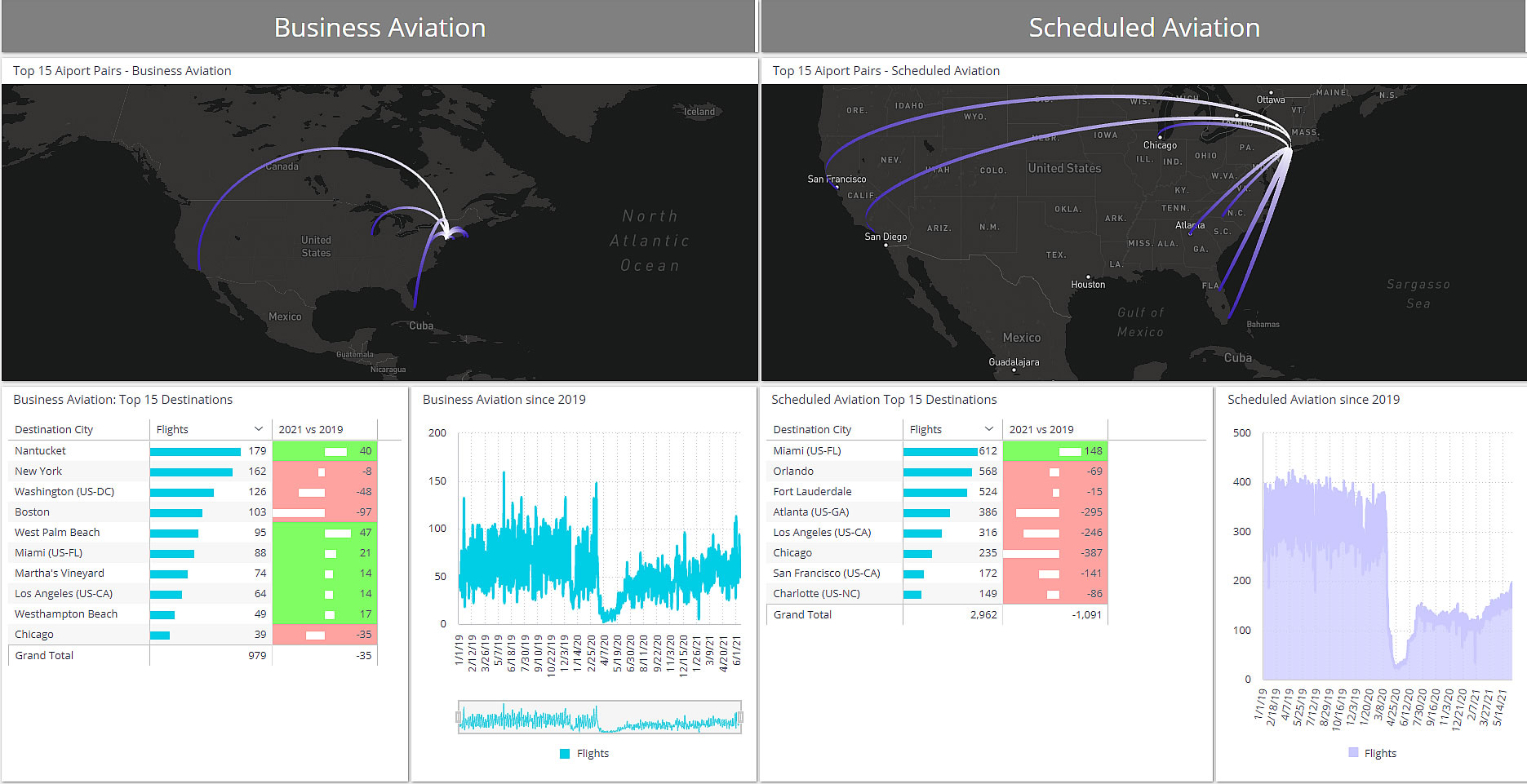

The US market is going form strength to strength as lockdown measures dwindle and the economic rebound gathers steam. Business jet activity so far this year is now 1% above the same period in 2019, and the resurgence is gathering pace, with the first half of June seeing 20% more business jet movements than June 2019, business jet flights comprising almost 25% of all sectors operated by fixed wing aircraft this month. Business jet departures in Florida are now a staggering 30% higher in 2021 than in 2019, recording 160,000 departures which is more than ten times the number of business jet movements in the UK for the same period. Most of Florida’s flights are intra-State, these 34% up on pre-pandemic. Flights between Florida and New York are up almost 70% on 2019.�

Business aviation vs Scheduled aviation from New York, 2021 vs 2019

Business jet demand in Texas and latterly, New York, has stormed ahead of 2019 trends in recent weeks. Within Texas, flight activity is still shy of 2020 let alone 2019, but connections between Texas and Colorado, Florida, and California are higher than ever. Across the country, Charter and Fractional Share operators are seeing the quickest rebound, their combined activity 60% up on last year and 10% ahead of 2019. The busiest aircraft segments in these sectors are Super Midsize and Light Jets, activity up 20% on normal. The stand-out jet types are the Challenger 300, Citation Latitude, Phenom 300, all clocking up record fleet activity. The Nextant is very busy as is the older Hawker 700-900 fleet. The Gulfstream GV/550 is flying 13% less this year than in 2019, but the Global 5500 fleet activity is up by 24% compared to the same period.

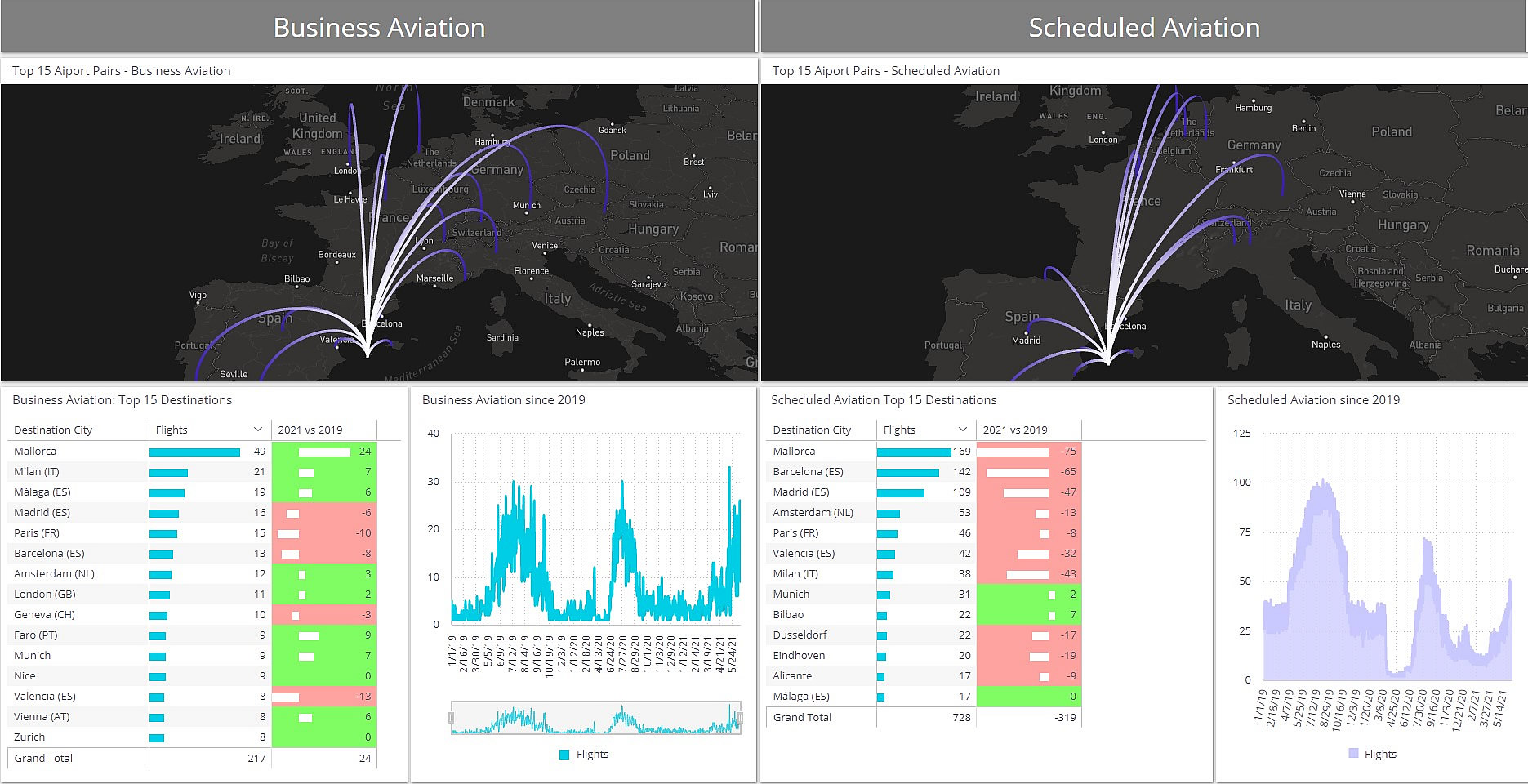

The recovery in business aviation activity is picking up pace in Europe, with first two weeks of June only 6% behind 2019, and more than double the movements we saw in June 2020. The analysis is flattered by continued very strong growth in business jet flights in Russia, Greece, across the Balkans and much of Eastern Europe, although business jet demand in Turkey has dried up on a year-on-year basis. In Western Europe, the outlier is Portugal, with flights far above normal for this season. Flights from Germany and Switzerland are within 10% of normal this month. But France is well behind, 30% fewer flights than in June 2019, little improvement on the YTD trend. That said the summer hotspots are regaining their customers, with jet and prop flights into Ibiza, Mallorca and Mykonos respectively up, versus 2019, 5%, 25% and 55%.

Business aviation vs Scheduled aviation from Ibiza, 2021 vs 2019