WINGX�s weekly Business Aviation Bulletin.

Overall Comment

The continuation of record-breaking demand for business jets in Europe and United States, beyond the normal end of the summer season and despite ongoing virus concerns, suggests the surge in demand is going to sustain well into Q4 2021. It may be that business executives are now adding to the strong leisure and lifestyle demand to fly private, with little sign yet that the airlines schedules are close to recovery. The immediate question is when we hit the ceiling in terms of available aircraft to charter.

Global

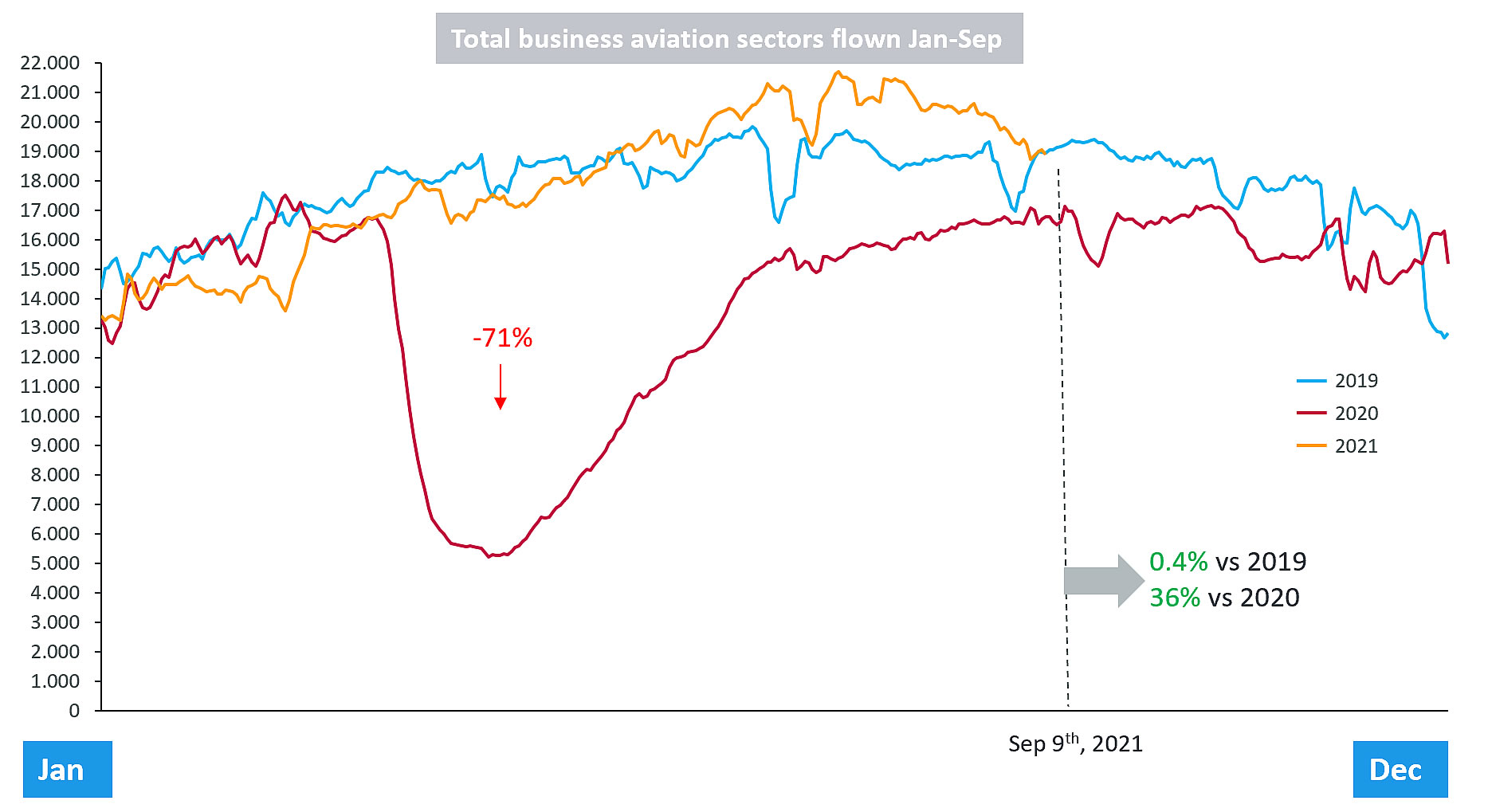

Business aviation traffic in the first two weeks of September is trending up 25% up versus September 2020, and 7% up on September 2019. Almost half of the 183,000 business jet and prop sectors operated so far in September have been generated by non-commercial flight departments, private and corporate, these still slightly less busy than two years ago. Aircraft Management companies, mixing owner and charter operations, are flying 9% above pre-pandemic levels, whilst fractional and branded charter sectors are up almost 20% on the same period two years ago. Scheduled commercial airlines are 46% less active than two years ago this month, scant improvement on the year-to-date decline versus 2019. Contrast business aviation, traffic so far this year now on a level with 2019, up by 3% for just the business jet fleet.

Business jet and prop sectors flown through September 2021 vs 2020 and 2019

North America

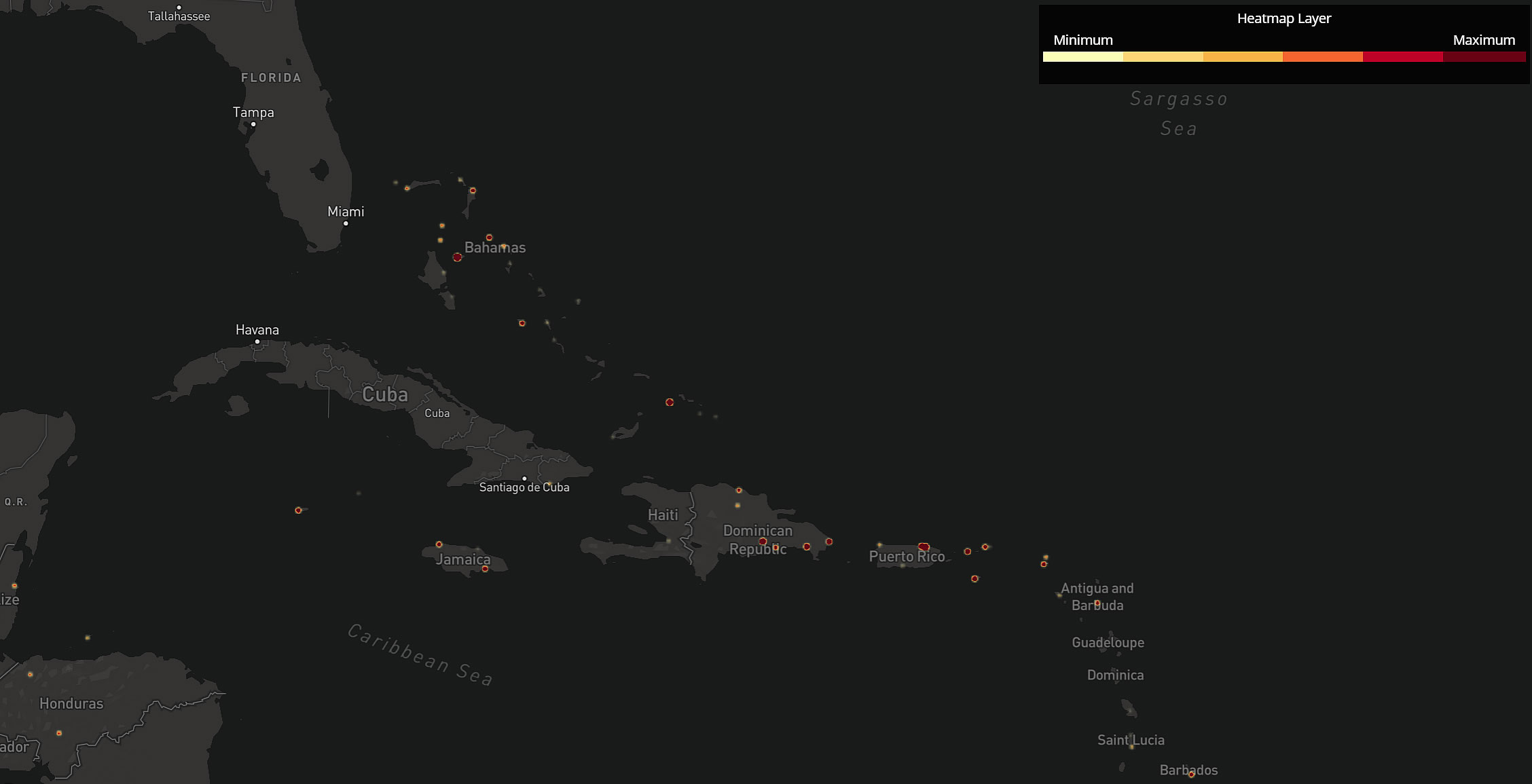

The North American market continues to see highest business jet activity on record, with September trending 7% up in terms of sectors flown. The program providers, with market leaders such as Netjets, VistaJet, Wheels Up, Flexjet, are setting the pace with at least 20% more activity than comparable 2019. Ninety two percent of the flight hours in the region are coming from the US market, which is up 12% on September 2019. Flight hours are down 22% in Canada this month compared to 2019, Mexico down by 44%. Turks and Caicos is maintaining its remarkable growth in visitors, arrivals up by 76% this month. Other North and Central American hotspots, easily beating any previous record for business jet activity, include Belize, Honduras, British Virgin Islands, Barbados.

Heat map of business jet departures in September 2021 in Caribbean

The continued restrictions on overseas visitors to the United States, and the more recent concerns over Delta variants, have not curbed strong rebound in business jet activity across the US States. Demand for business jet travel in California is surging back, sectors up by 11%, hours up by 14%, same with Jet A1 uplift, showing the rebound in larger aircraft and longer sectors. Florida, where business jet demand has held up all year, is now seeing an even stronger lift, departures this month up more than 50% on two years ago. Colorado is the 4th busiest State, flights bouncing 19% above the norm this month. New York has fewer flights, but demand is up 24% on September 2019. Other States with big September growth include Arizona, South Carolina and Georgia.

Europe

Europe shows no sign of slowing down this September, despite the end of the summer holidays, which would normally see a fall-off on peak activity. Business jet sectors are up by over 25% compared to first half of September 2019. All business jet segments, with the sole exception of corporate bizliners, are seeing stronger activity than two years ago, with even ultra-long range jets, idle for much of the pandemic, seeing 25% increase in sectors, 15% in flight hours. Very Light Jets represent almost 10% of all jet sectors flown this month and are trending up 46% on September two years ago. The average sector length of business jet sectors this month in Europe is 535 nautical miles. Croatia appears to be the outstanding European hotspot for business jet arrivals, 107% above levels in September 2019.

Asia

In Asia, a strong rebound in business jet activity this year has extended into September, sectors up by 11% versus two years ago. In contrast, there is a long-standing deficit in terms of hours flown, which are down 5% this month, little improved on 7% decline this year versus 2019. The shorter sectors, with very few international trips, have also tilted towards smaller jets; Jet A1 fuel uplift is down by 20% in Asia this year compared to 2019. The regional differences are acute, with growth in flight sectors and hours in South and Central Asia. East Asia and particularly South East Asia have seen the weakest recoveries, respectively trailing by 5% and 15% in sectors. Business jet departures from China and Hong Kong are up by 6% this year versus 2019, but flight hours are down by 19%.

Business jet activity in South-East Asia in September 2021