WINGX�s weekly Business Aviation Bulletin.

Overall Comment

The European recovery is picking up rather than tapering and the US domestic market is still breaking pre-pandemic records.

Given that the holiday season is ending, this sustained growth may hint at a return of the corporate customer, especially as airline recovery is slow and tenuous. International connections are also starting to recover faster. As NetJets limits its fleet access, smaller operators are likely getting record demand for lift.

Global

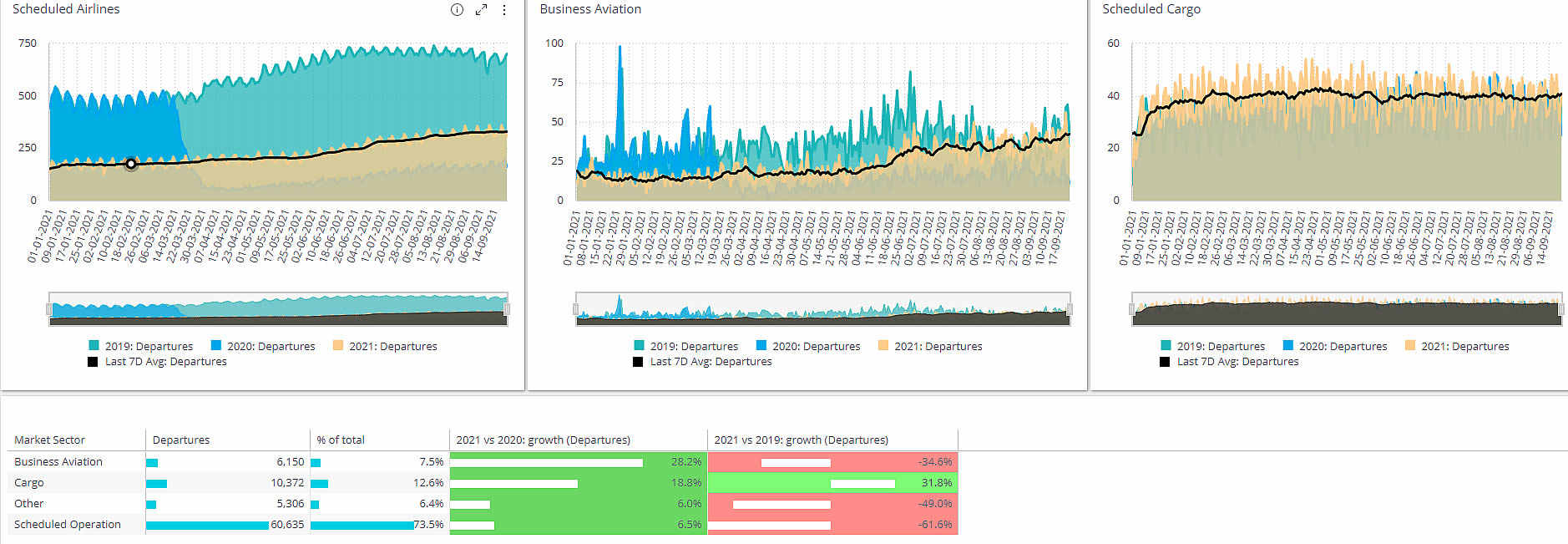

Since May 2021, pre-pandemic comparable month traffic levels have been eclipsed. So far in September 2021, business jet sectors are up 15% compared to the first 3 weeks of September 2019.

Passenger airline traffic is only 20% up on 2020 so far this year, although it has bounced 47% this month. Compared to 2019, the airlines’ recovery is painfully slow, sectors still trailing by 41% versus last 2019 year to date. Cargo operators continue to see more activity than before, up by 9% this month, up 7% this year.

From November, transatlantic flights are expected to restart as the US announced a softening of restrictions on inbound passengers from Europe including the UK. So far this year, the transatlantic connection has shown little sign of recovery; though improved on 2020, arrivals into North America are still down 25% through the first 9 months of 2021 versus 2019.

Passenger airlines are further behind, with 61% fewer transatlantic sectors. Transatlantic cargo traffic has surged ahead, up 31% on pre-pandemic. Other inter-regonal connections have been slower to recover, although business aviation flights from Europe to Asia region are down only 2% this year versus 2019.

Specifically to South East and East Asia, business jet flights from Europe are down 75%. There are exceptions to long-haul traffic declines: flights from Europe to the Caribbean are up 13% this year versus 2019, and from the US, jet sectors to the Caribbean are up 1%.

Transatlantic flights from Europe to North America in 2021, 2020 and 2019

North America

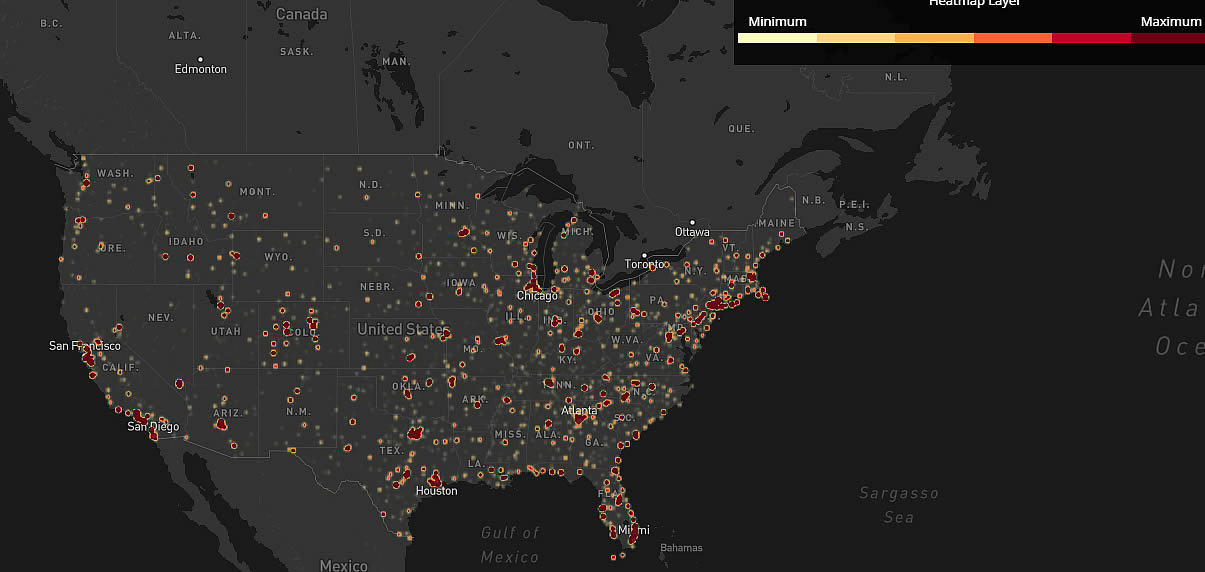

The domestic US market continues to move ahead of comparable 2019 activity. Over 20,000 business business jets and props have been active this month, an average of 44 hours utilisation in the first 3 weeks of September, with an aggregate activity almost 10% above that of September 2019.

The Part 135 and Part 91K operators are doing best, with branded charter operations up almost 30% so far in September, versus 2 years ago. Overall domestic business jet hours are up by more than 15% versus September 2019. There is stand-out growth this month at metro hubs including Denver, Dallas, Miami, Fort Lauderdale, Orlando, West Palm Beach. Chicago airports, long in the doldrums in terms of activity, has seen a 23% increase in flights this September. Van Nuys has 15% more departures this month, 25% increase in outbound flight hours, versus same period 2019.

Heat map of domestic business jet activity in the US in September 2021

Europe

Europe is seeing the stronger end-of-summer recovery, with September�s business aviation activity surging more than 25% beyond September 2019. The UK has seen an 11% increase in activity versus pre-pandemic September, and lags most other countries in Western Europe, with demand in France up more than 20%, flights in Italy, Germany, Austria, up more than 30%, arrivals into Spain up by 40%, arrivals into Greece up more than 60%.

Business jet flights to and from Croatia have more than doubled compared to September 2019. The busiest country connection from Croatia is Italy, 94 flights so far this month, with Germany, France, Austria and UK also featuring highly. Overall in Europe, most of the busy connections are still domestic, although there is now strong recovery in flights between UK and France, Switzerland, and Spain. Flights within Russia are up 80% versus September 2019.

Top 20 outbound business jet pairs from Croatia, September 2021

Rest of World

Outside the US and Europe, the September trend is notably weaker overall, trending 4% below September 2019.

The same geographical pattern persists, with relatively large business jet markets including Canada, Mexico, Saudi Arabia, Japan, Morocco, all continuing to see big deltas utilisation versus 2019, whilst Brazil, Nigeria, South Africa, United Arab Emirates, have more activity this month than two years ago. China and Australia are seeing more flights, but fewer flight hours.

The Phenom 300 is the most popular business jet, with 15% growth in activity compared to 2019. The ageing Hawker 700-900 fleet is flying more hours than ever. The Global 6000 has flown 25% fewer sectors this month versus two years ago, and Gulfstream 600 flight hours are comparably trending down 30%.