WINGX�s weekly Business Aviation Bulletin.

Overall Comment

The recovery in flight activity is entering an uncertain phase as the global backdrop for business aviation gets more complicated. The pace of the economic recovery is slowing, with inflationary risks increasing as post-pandemic supply line disruption becomes more apparent. Ongoing virus concerns are keeping a lid on international travel, although the softening restrictions in Europe have prompted a big rebound.

Global

Global business jet activity in September is finishing up against September 2019, a gain of 9% more flights over the most recent comparable week, 14% for the full month. North American activity is up by 6% this month versus two years ago, the US domestic market up by 5%, 50% up on September last year. Europe has had a consistently strong month, with 2019-benchmarked business jet sectors up 26% in the last week, up 27% for the month. The bigger picture shows that Scheduled Passenger Airline traffic is trending 30% below September 2019, a modest improvement on the 40% year to date deficit, but overall, still only 20% up on last year. Cargo operations continue to operate above pre-pandemic levels although the last week has seen a slow down which may reflect growing concerns over the disruption of global supply chains.

Busiest airports for business jet activity in 2021 (green = growth vs 2019)

.jpg)

The worldwide business jet market remains on track to post a record year in terms of utilisation, with the strong summer rebound taking full year trend 2% above 2019. Turboprop activity has been weaker, but is still within 1% of where it was pre-pandemic.

North America

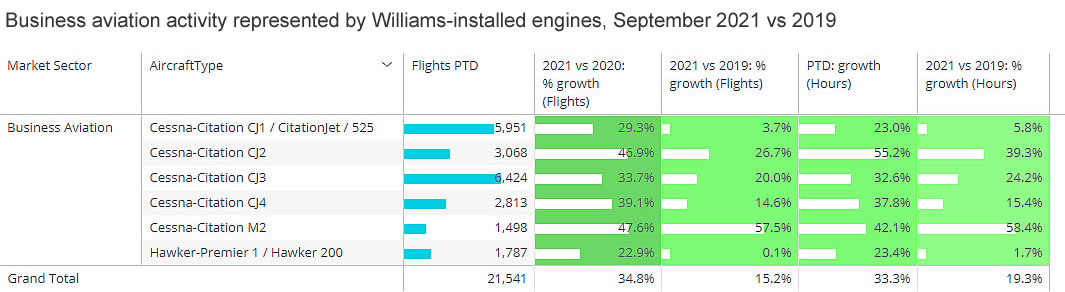

The core business aviation market, in North America, had a very strong September in Part 135 and Part 91K operations, the latter seeing 25% increase in sectors compared to September 2019. The US market has also seen a tentative recovery in Private operations, including both individual and corporate flight departments, flights up 1% compared to September 2019. Shuttle operations, including corporate shuttles, are still down by 6% versus pre pandemic. Overall, aircraft with Pratt & Whitney and Rolls Royce engines are flying up 4%, whereas aircraft installed with Williams, mostly Citation light jets, are flying 15% above the norm.

Business aviation activity represented by Williams-installed engines, September 2021 vs 2019

The busiest business jet in the US market is the Citation Excel, flights up 14% versus September 2019, but the jets with the biggest rebound late-summer are Phenom 300 and Citation Latitude, over 20,000 sectors flown this month and trending up 50% on the smaller fleet back two years ago. Florida, California and Colorado are the hub spots for these two aircraft types, all seeing well over 60% increase in pre-pandemic flights in this fleet. At the other end of the spectrum, ultra long-range business jets are recovering much more modestly, flights back in line with 2019 although hours some way behind.

Within the largest cabin sector, Gulfstream GV/500-550 operations are lagging pre-pandemic by 5%, Gulfstream 600/650 sectors are up 5% this month, and whilst Bombardier Global 6000/6500 platform is flying 4% less, the 5000/5500 fleet has seen more than 30% gains compared to September 2019. The Falcon 7X has the largest deficit, flight hours off the norm by 31%.

The busiest pairs for US operations of ultra long range jets have been connections between Van Nuys, Los Angeles, and Teterboro, with municipal airports like Hawthorne also seeing a big increase in flights from the norm, particularly connections to Brownsville in Texas. Typically busy 2019 connections such as Teterboro to Toronto or to Boston are still 30% off. Overall, ULR jet flights within the US were up 2% this month, with international flights still way behind, 21% off vs September 2019. But this is variable; notably, ULR flights from the US to Italy are up 28% this month.

Europe

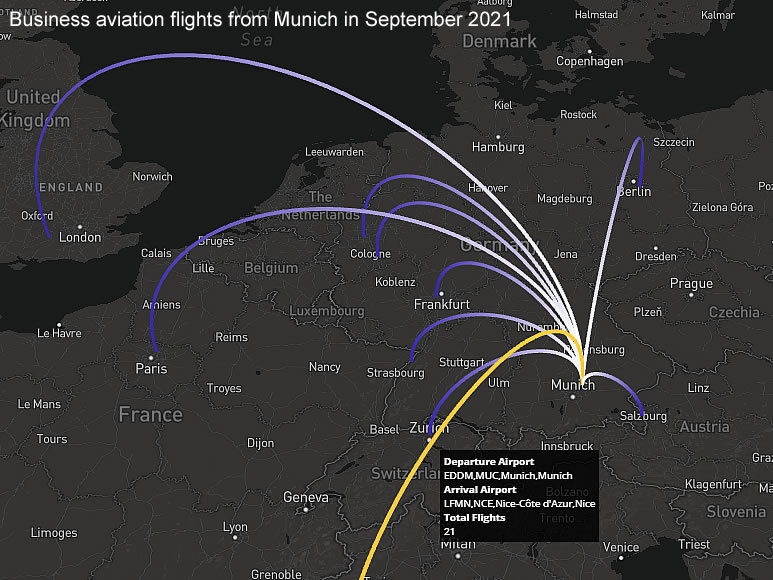

The European market is continuing to post it’s strongest ever business aviation utilisation, well beyond the end of the typical summer season. Across the European Union, flight activity has rocketed 24% above levels in September 2019, with the biggest spike in international flights. This is surely connected to the pervasive deficit in scheduled capacity, with these sectors running 38% below September 2019. For example, during September so far, business aviation flights from Munich are up by 24% compared to two years ago, whilst passenger schedules are down 55% for the same period. The Scandinavian market has seen the smallest recovery, around 5% up on September 2019, with France, Germany, Netherland, Poland seeing at least 20% pick-up in sectors versus two years ago. Italy, Spain, Greece, Portugal are seeing much larger gains compared to pre-pandemic.

Business aviation flights from Munich in September 2021

Rest of World

Outside Europe and the United States, it continues to be a mixed bag of record activity, modest rebound, and enduring declines. The aggregate trend has been much weaker than for Europe and the US this month, with 4% fewer flights, 8% fewer hours, versus September 2019. Both Canada and Mexico have had very weak recoveries throughout the recovery, and September does not show any big change. China�s activity has significantly fallen off in the last two months, with sectors down 6% on 2020. Australia is in the top 5 markets, activity still shading 2019 levels, despite the ongoing lockdowns. the fastet growing business jet markets are Brazil, Colombia, UAE, India, South Africa. The UAE has seen tremendous growth in activity this year, up 70% on 2019. Ultra Long Range departures from the UAE are up 24% this year, Heavy Jet sectors up over 150%, Legacy 600/650 the most prolific.