WINGX�s weekly Business Aviation Bulletin.

Overall Comment

Business aviation flourished in 2021, with a very strong rebound in demand in from Q2 onwards, characterized by leisure demand, unleashed as travel restrictions loosened. The prolonged slump in scheduled airline capacity, and the persistent hygiene concerns around new virus variants, appear to have migrated business aviation services to many new customers. The resilience of the rebound in 2021 will be tested in early 2022 by the travel behaviour of business executives.

Global

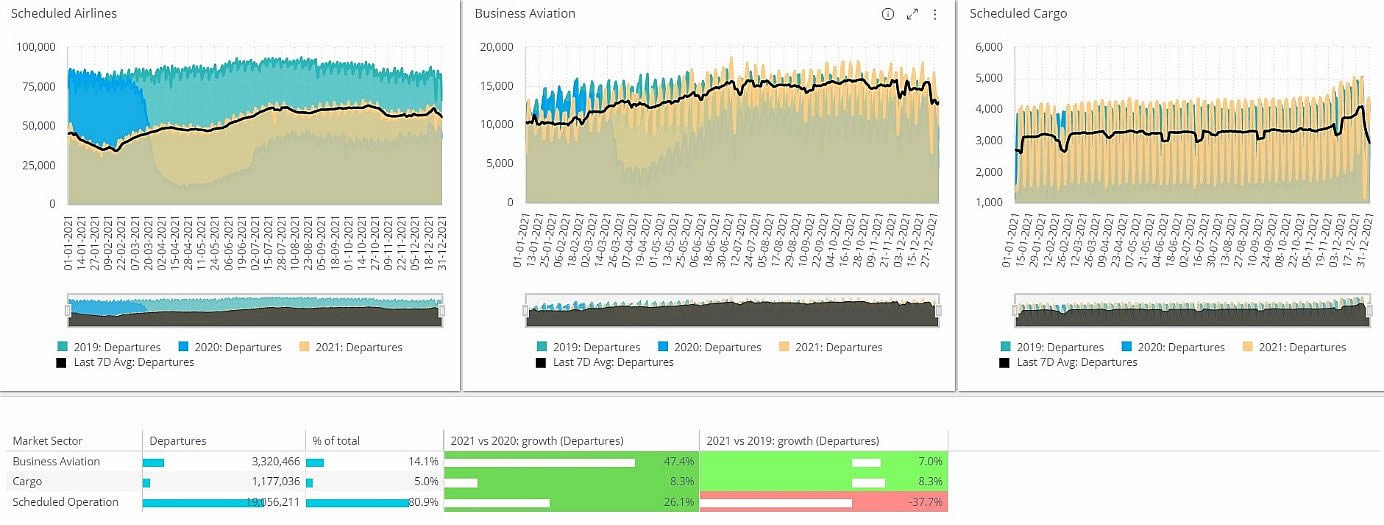

Business jets flew more sectors worldwide in 2021 than in any previous year on record. With 3.3 million flights from January through December, business jet traffic was 7% higher than in 2019, the previous high point for global business jet demand. Comparable growth was at its highest in the last month of the year, with the month of December seeing 23% more sectors flown than December two years ago. Over the holiday period (December 20th – Jan 2nd), business jets flew 127,000 sectors, 41% more than in the same period two years ago. In contrast, scheduled airline passenger traffic was down by 28% versus December 2019, in line with the full year trend. Cargo operations showed similar resilience to business jets during 2021, with dedicated cargo sectors up 8% compared to 2019.

Business Jet sectors flown vs Scheduled and Cargo activity 2019 � 2021

North America

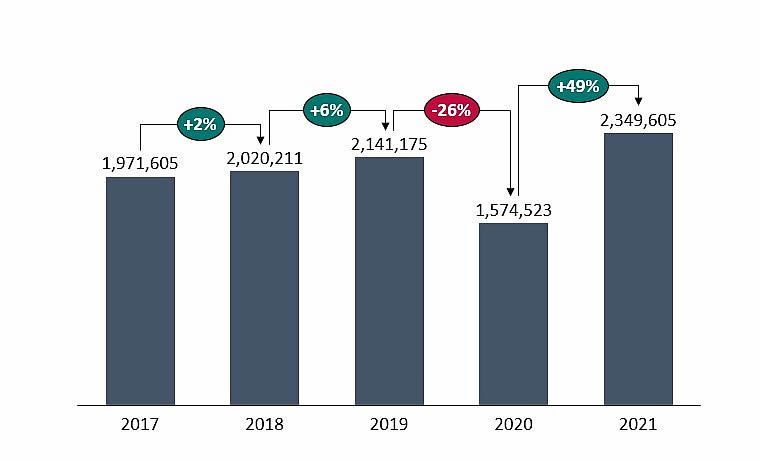

In North America, including Mexico and Canada, business jets flew 6% more sectors compared to 2019. The demand was fuelled by the United States market where business jet activity was 10% higher than 2019, contrast neighbouring Canada, which saw 24% fewer sectors than two years ago. The rebound in business jet demand in the US came from Fractional and Branded Charter operations, respectively up by 20% and 18% compared to full year 2019. Private and Corporate Flight Departments saw a more modest recovery in activity but nonetheless surpassed comparative 2019 activity by the end of 2021. The high points in business jet demand in the US showed up in holiday periods and were geographically concentrated around leisure destinations. Demand was exceptionally high during the Christmas and New Year period; between December 20th and Jan 2nd, business jets in the US flew 46% more sectors than in 2019. Relatively, scheduled airline traffic was still 16% adrift of the same holiday period in 2019.

Business jet departures in the United States, 2017-2021

Within the US market, the busiest jet segment in 2021 was Light Jets; 662,000 sectors flown, almost one million flying hours operated, traffic up by 15% compared to 2019. The Super Midsize segment saw the largest growth in sectors compared to 2019, up 18%. The Challenger 300 was the busiest business jet type, with 179,000 sectors operated, up 12% on the active fleet in 2019. Ultra-Long Range jet activity was well behind pre-pandemic levels during 2020 and the first half of 2021, but by the end of the year, sectors flown had nosed ahead of 2019, even if hours operated were still 7% down on two years ago. Heavy jets have not yet seen a robust recovery, and at the top end of the cabin size, bizliners flew 43% fewer sectors in 2021 compared to 2019.

Europe

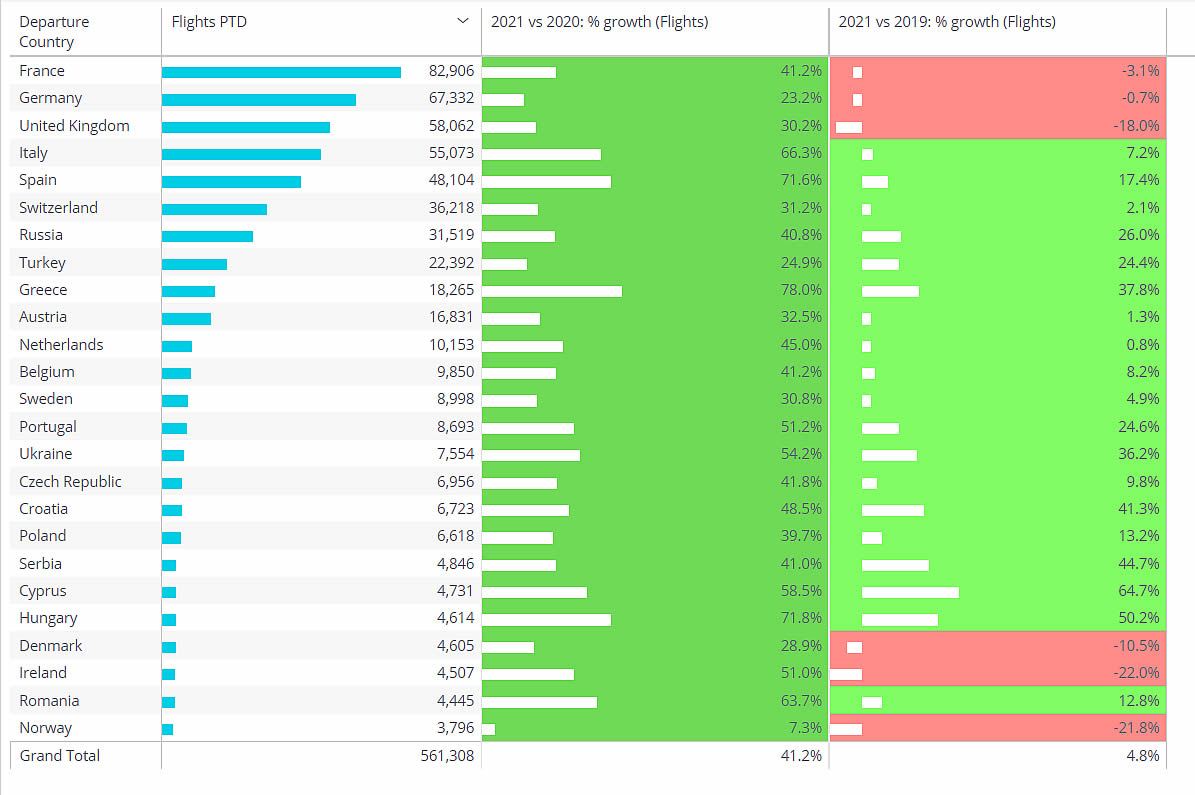

Despite the hesitate recovery of European economies from lockdown, business jet activity in the region clearly surpassed 2019 levels, with 5% more sectors flown by year-end. As in the US, business jet demand peaked during the Christmas and New Year holiday period, with 30% more sectors flown than during the same period two years ago. Demand was variable geographically, with the three largest markets, France, Germany and the UK, ending the year still some way short of 2019 in terms of sectors flown. In contrast, Italy and Spain saw the strongest rebound in the EU in 2021, reflecting robust leisure demand. Russia and Turkey, with large domestic markets and looser travel restrictions, both saw consistently very strong increases in business jet sectors, up by a quarter compared to two years ago. Across the European region, the standout growth came in the lightest cabins; Very Light Jet sectors were up 22% in 2021 vs 2019.

Business jet departures by country in Europe in 2021 vs 2020 and 2019

Rest of the World

Business jet activity outside North American and European regions constituted a small minority of the global total, with around 200,000 sectors representing around 6% of worldwide activity in 2021. There was substantial growth compared to pre-pandemic trends, with 28% more business jet flights operated than in 2019. The trends were diverse regionally, with Asia getting modest growth in business jet traffic, buoyed up in India and Australia, but stunted in China, especially in the latter half of the year. The Middle East saw some of the strongest growth in business jet demand in 2021, notably in the United Arab Emirates, sectors up by 73% compared to 2019, contrasting with very modest growth in Saudi Arabia. Elsewhere, Brazil, Nigeria and Egypt saw much more activity in 2021 than in 2019.