WINGX�s weekly Business Aviation Bulletin.

Overall Comment

Geopolitical issues are now front-stage in terms of outlook for continued growth in business aviation in 2022. For European business jet operators, Russia and Ukraine connections comprise almost 10% of all flights, with Central and Eastern Europe, and heavy jets in general, having a much larger exposure. Downstream consequences from the current crisis could have severe economic consequences which will threaten flight demand as the year unfolds.

Global

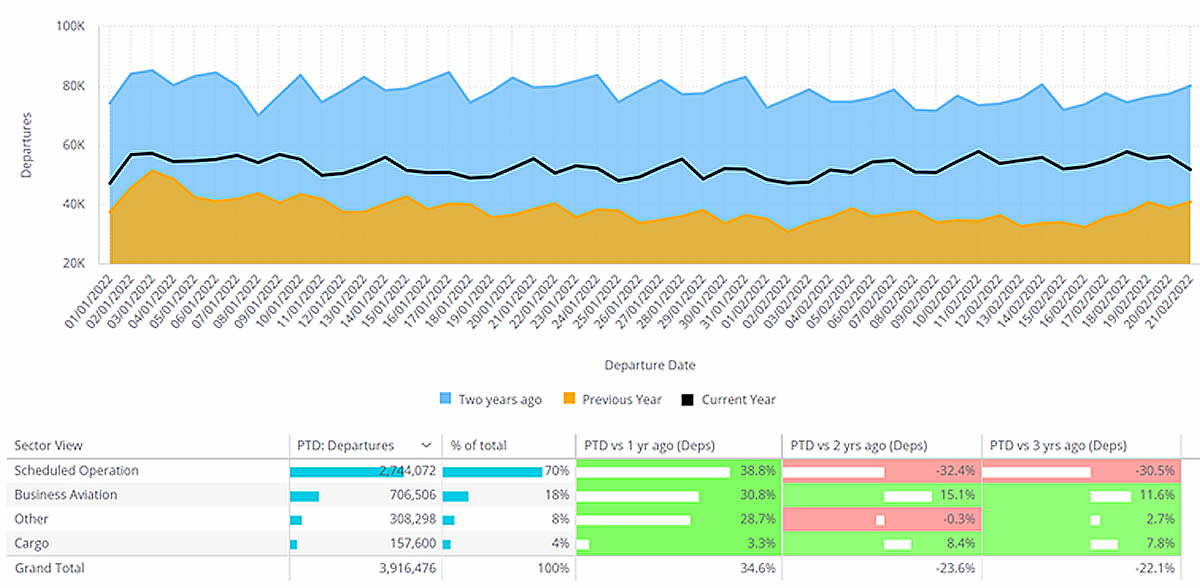

There has been a significant increase in geopolitical tensions in the last week, which is likely to exacerbate financial instability, but at least for the time being, business aviation activity has continued to flourish. So far in 2022, through the second half of February, bizjet flight sectors are up by 12% compared to pre-pandemic January and February 2019. Compared to winter 2021, this year´s activity is up 31%. Global scheduled airline activity is also up more than 30% compared to last year, but still down by 31% compared to same period 2020, just as the pandemic was breaking. Cargo activity has stayed ahead of the pre-pandemic trend ever since March 2020, although growth is moderating, with 2022 so far seeing 3% growth compared to January and February 2021.

Global business jet activity in Jan-Feb 2022 vs 2021, 2020, 2019.

Europe

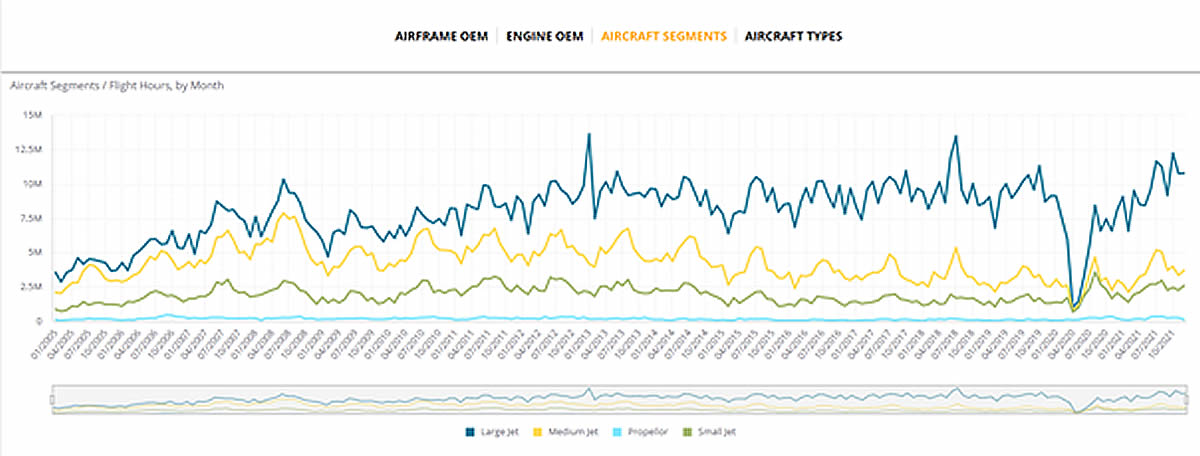

The Ukraine crisis has rapidly displaced the pandemic as the most significant destabilizing factor in the European region. Based on just the last seven days, the only country to see an obvious slowdown is Germany, where business jet sectors are down by 16% compared to same period pre pandemic 2019. Bizjet activity in Spain, Italy, Netherlands is up by over 20% compared to February 2019. As with France, Switzerland and Turkey, Russia has seen more than 10% growth on 2019 activity. The much longer-term view of flight activity out of Russia, since 2005, illustrates that recent flight activity has recently come close to previous peaks in 2018 and 2013, and until now, appeared to be on an upward trajectory in the last 18 months, especially in Large Jet activity. Russia registered jets (RA) had a particularly strong 2021, activity up by 80% compared to 2019.

Business jet departures from Russia between 2005 and 2021

The fall-out from the Ukraine crisis is indeterminate at this stage but is bound to cause significant short term turbulence in international relations, trade and financial markets, although the more specific impact for business aviation will likely come through targeted sanctions imposed by the West. In the European region, in 2021, 11% of all country connections involved Russia or Ukraine, as an arrival or destination, and that translated into 7% of all flights. The exposure is much higher for some countries than others, with respectively 22% and 16% of flights from Estonia and Cyprus heading to Russia, but only 1% of outbound UK flights, 6% from Turkey. There is variable exposure across OEM fleets, with 25% of European BBJ flights connecting with Russia and Ukraine during 2021, 12% of Gulfstream activity, 3% of Cessna. As well as Bizliners, Heavy Jets have a high exposure, 16% during 2021.

North America

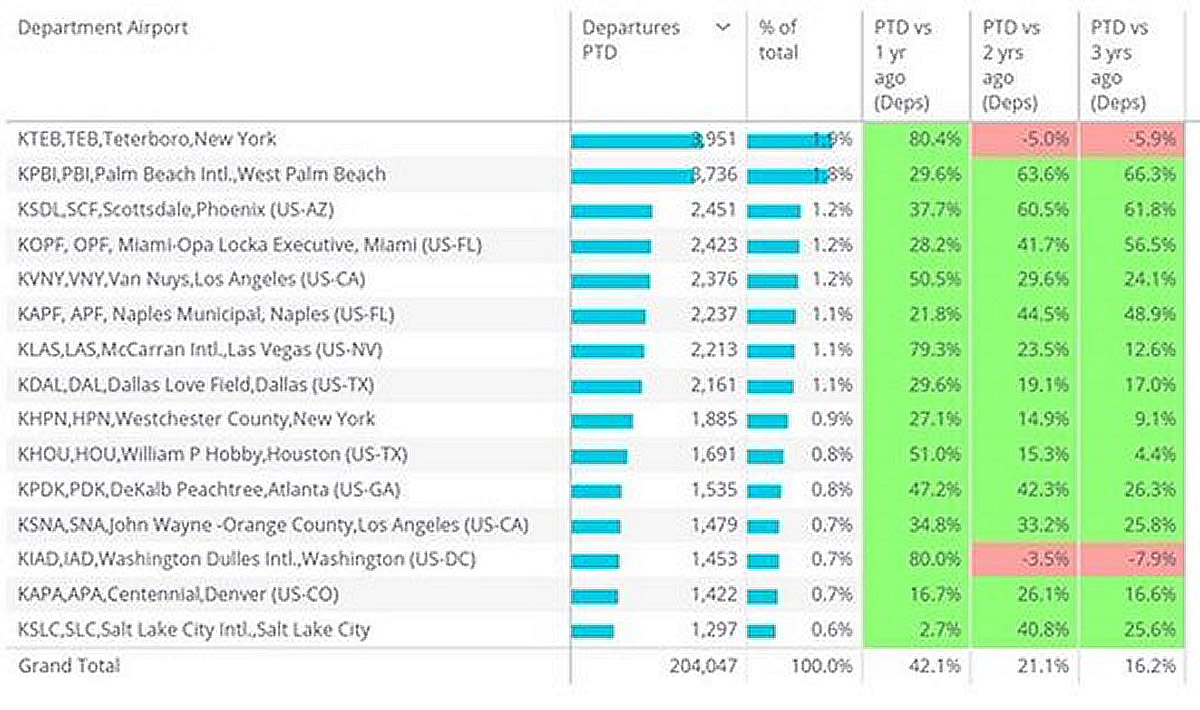

In North America, the scheduled airline recovery is gaining pace, with narrow body passenger traffic within 10% of 2019 trends. There may be a lagged effect on business aviation demand, but at least in the last week there is little sign of a slowdown, with business jet sectors 16% ahead of 2019, 24% ahead of 2020, and rebounding 54% above last year. Bahamas, Puerto Rico, Sint Maarten, Turks, and especially Costa Rica, all are well ahead of 2019 levels in terms of business jet arrivals in the last week. Ultra Long Range jets are seeing the strongest recovery this year, with ULR jets flying 38% more than same week 2020. For the month-to-date, two airports with significant international exposure, Teterboro and Dulles, are still behind activity in February 2019 and 2020.

Top airports in the US for business jet activity in February 2022 vs 21, 20, 19

Rest of the World

Outside the North American and European area, business jet traffic has surged well above 2019 levels over the last 6 months. Taking the region as a whole, business jet activity this year is up 16% on January and February 2021, up 21% compared to early 2020 and up 44% compared to three years ago. Much of this growth is coming from a few countries where business aviation aircraft have significantly amplified their role, including Brazil, Nigeria, Colombia, Argentina. Other countries continue to see a strong trend in touristic business jet demand, notably in the Middle East, with UAE, Saudi Arabia and Israel well above 2019 trends. The relatively weaker region is Asia, where for example China and Singapore are respectively 14% and 48% below December 2019.