WINGX�s weekly Business Aviation Bulletin.

Overall Comment

The industry is looking with trepidation at the repercussions for the global economy from the Ukraine invasion, but the effect is small in terms of immediate reduction in flight activity. The swift decline in outbound flights from the directly affected regions is more than offset by the ongoing strong demand for on-demand travel as the final constraints on travel restrictions are lifted in Europe and the US.

Ukraine Crisis

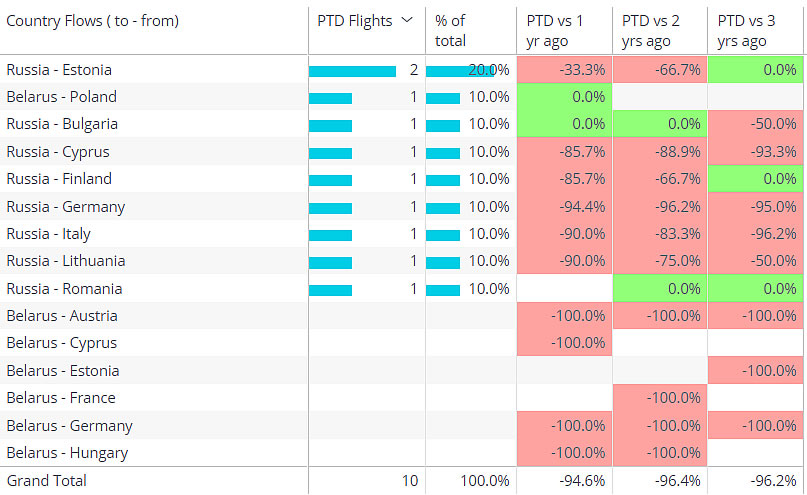

The declines in flight activity out of Russia, Belarus and Ukraine (RBU) accelerated sharply during the second week of the invasion. Compared to activity in the previous week, scheduled passenger airline sectors were down 54%, Cargo flights down 66%, Business jet departures down by 57%. Compared to the same first week of March in 2019, business jet departures from these three countries were down by 39%. To put this in context, up until the invasion, business jet departures from Russia were up by 25% compared to the January-February period of 2019. The biggest declines, unsurprisingly, have been to those countries which have implemented airspace bans on Russian-controlled aircraft.

Bizjet departures from RBU in last week to countries with ban on Russian aircraft

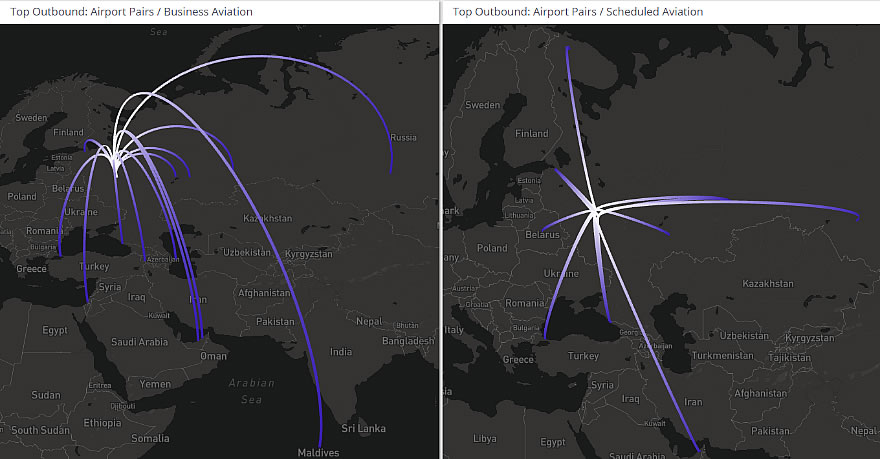

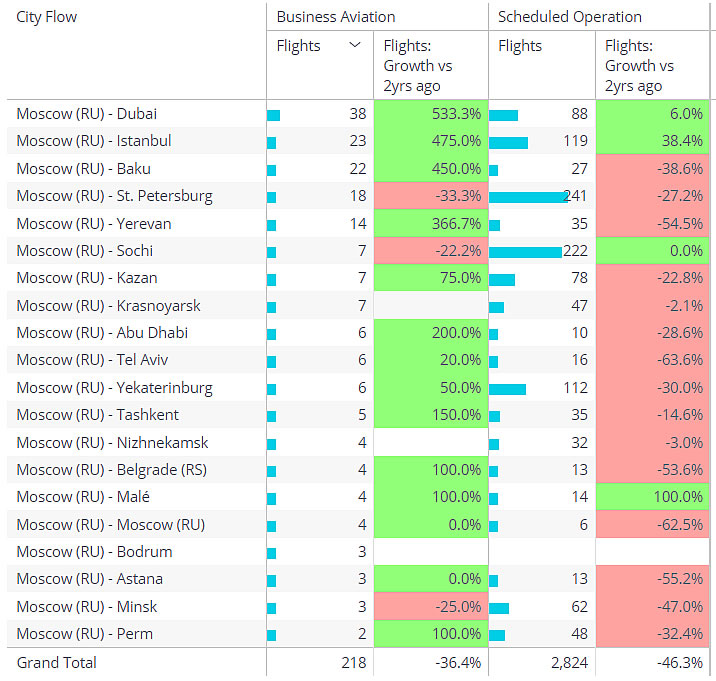

Relatively, Russia domestic activity is more resilient, representing almost half of all bizjet flights, and 10% higher than the same week back in 2019. The busiest bizjet city pairs include St Petersburg, Kazan and Moscow. For domestic trips, the Falcon 900 is the busiest business jet in the last week. Flying international, the most popular destination is UAE, and specifically Dubai. With 49 outbound flights in the first week of March, the Russia-UAE connection is three times busier than pre-pandemic, but just two thirds of the outbound activity during the last week of February. The Embraer Legacy 600 has accounted for more than 60% of these trips. Next most popular international destinations are Baku and Istanbul.

Business jets vs Scheduled airlines from Moscow, March 1-7 2022 (ref to 2Y ago = 2020)

Europe

It´s striking that, so far, business jet activity in Europe continues to exceed pre-pandemic levels despite the Ukraine crisis. In the first week of March, bizjet sectors were up 17% compared to March 2019, and as a mark of the recovery from Covid restrictions, fully 50% more activity than comparable March 2021. Strong bizjet demand in Europe also reflects the ailing scheduled network, trending 30% below pre-pandemic levels so far this year. Demand for fractional and charter flights has provided momentum for the last 6 months, although the most recent boost has come from recovering non-commercial flight departments, including corporate flight departments.

North America

The North American market is evidently insulated from the immediate effects of the Ukraine crisis, and is seeing the “tail end” of the recover from Covid, with most benefit for the largest cabin aircraft flying multiple-hour sectors. For example, ultra-long range jet activity is up by 28%. In the largest cabin aircraft, the bizliners, the Airbus ACJ is rapidly recovering on pre-2020 activity, although notable BBJ fleet activity is trailing, sectors 60% below where they were in March 2019. The lighter end of the fleet has been the biggest beneficiary of the recovery, with Cessna´s North American fleet flying 35% more sectors this March compared to 2019.

Rest of World

The regions outside of North America and Europe, including Russia, have seen the strongest of all rebounds in bizjet flights in 2022, with a 52% increase in this March compared to three years ago. Brazil, Argentina, Australia, India, Nigeria, have all seen much higher activity than pre-pandemic. There are a few countries which haven´t seen such a strong recovery and these are mainly in Asia. In this region, prolonged pandemic restrictions and turbulent geopolitics have constrained flight activity, particularly flight hours. China has seen the biggest slowdown, with outbound sectors down by 48% in the first week of this month compared to 2019.