WINGX�s weekly Business Aviation Bulletin.

Overall Comment

As the Ukraine crisis deepens, record business jet demand in Europe is slowing, with demand in Germany falling back from recent highs, now back below pre-pandemic levels. Small and midsize jets are doing an increasing share of activity, with larger jets more exposed to fading demand from Russian customers. Across the Atlantic, the US market is still very strong, especially in large cabin aircraft. Elsewhere, business jet activity in China is all but grounded by the lockdown.

Ukraine Crisis

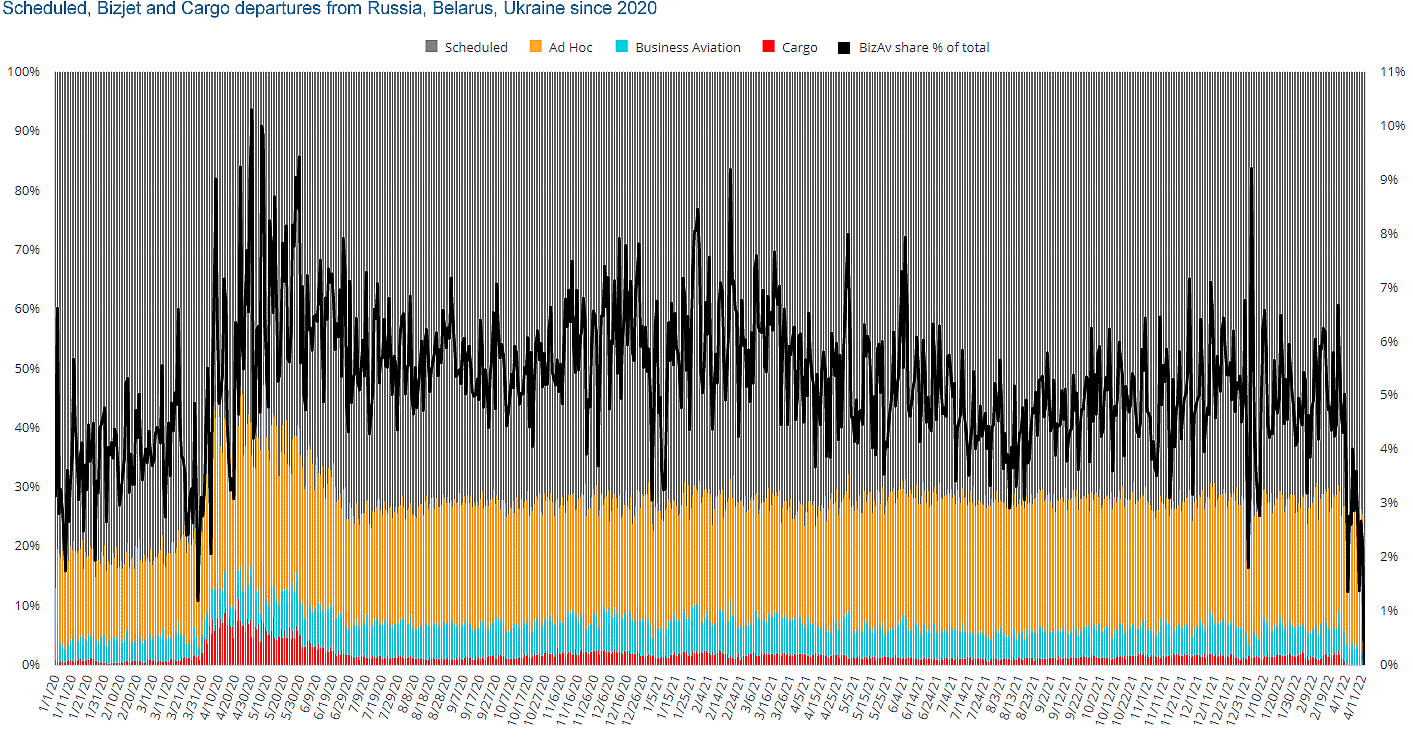

Through April 11th 2022, just 311 business jet departures have been recorded out of Russia, Belarus and Ukraine. As the crisis deepens, scheduled airline and cargo operations are also swiftly declining. Total fixed wing activity from this region has dropped 43% in the first part of April 2022, and although that volume was still double what it was in April 2020, it’s down by 50% compared to pre-pandemic April 2019. The last few days have seen a more precipitous fall in activity. Just 59 business jet flights have been operated internationally in the last 7 days, a drop of almost 90% vs 3 years ago. The charter market as almost disappeared, with just private owners active. The bulk of business jet departures are flying domestically within Russia. Of the international sectors, most are going to Turkey and UAE.

Scheduled, Bizjet and Cargo departures from Russia, Belarus, Ukraine since 2020

Europe

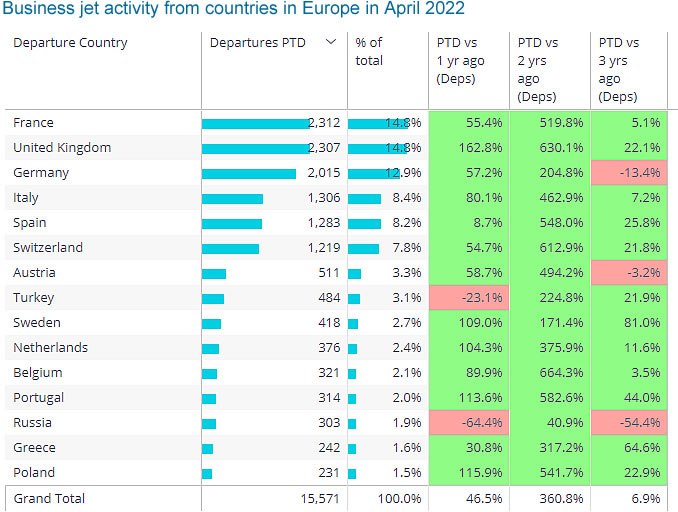

The deepening economic impact of the Ukraine crisis is apparently slowing the record growth of business jet activity in Europe. It�s still at all-time highs, up by 7% in April 2022 compared to April 2019, but that�s falling behind the 14% trend for Jan-April year-to-date compared to 2019. The drop in demand in Russia is the big factor; with Russia excluded, the growth trend in April is still almost 10% above pre-pandemic levels. Some countries are seeing much stronger rebounds in business jet activity, with UK, Spain, Switzerland business jet sectors up by over 20% compared to April 2019. Germany is clearly taking the major impact of the crisis, with bizjet activity falling 13% this month compared to April 2019.

Business jet activity from countries in Europe in April 2022

Excluding the Russian market, the record growth in business jet demand is coming in Super Midsize and Super Light Jet sectors, up respectively 30% and 22%. For example, Challenger 300 activity is up by 58% compared to 2019, and the Embraer Phenom 300 fleet is 48% busier this month. Heavy Jet activity has dropped back, still up by 51% compared to last year, but down 6% compared to April 2019. This reflects an exposure to fast-fading demand from Russian customers; 16% of all business jet flights in Europe in 2021 connected with Russia and Ukraine. Ultra-Long Range jet activity has a very modest 1% edge on April three years ago. Global 6500 activity is 2% down on April 2019, and Challenger 600 demand has fallen off by 20%.

North America

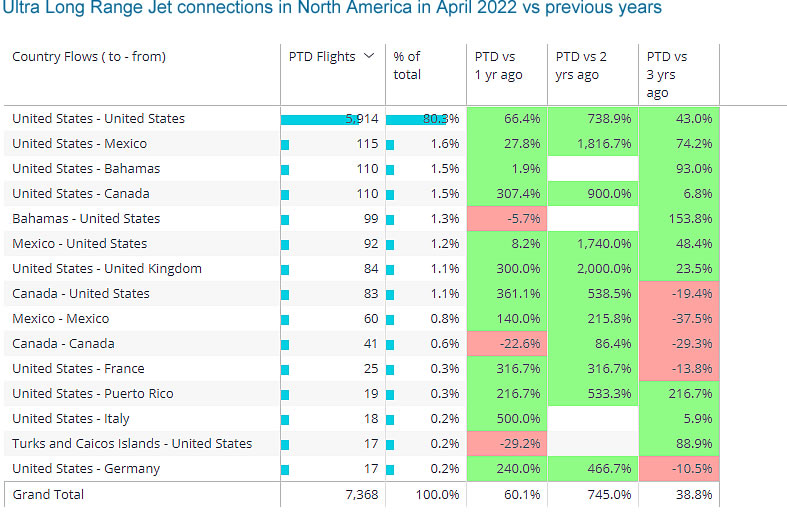

Business jet activity in Russia is at record levels, 26% higher than April last year, five times the activity of April 2020, up by 25% compared to pre-pandemic April 2019. The Ultra Long Range jet segment has is now seeing the strongest rebound compared to last year, sectors up by 60%, and up by 39% compared to April 2019. 80% of that ULR Jet activity is US domestic, with the next busiest country flows between the US and Mexico, Bahamas, and Canada. Whilst ULR jet activity in Government and Ambulance missions has fallen off this month, Private and Corporate flight departments are flying 46% more than in April 2019, Branded charter ops are up by 43%, Fractional flight activity up by 27%. For ULR jet branded charter operations, the busiest airport this month is Teterboro, 78 flights in the last 10 days, 20% more ULR jet departures than back in April 2019.

Ultra Long Range Jet connections in North America in April 2022 vs previous years

Rest of World

Charter operations in Ultra Long Range jets outside North America and Europe have still not recovered to pre-pandemic levels, 2% fewer flights operated worldwide this month compared to April 2019. Including all business jet platforms operating across the rest of world, sectors are well up on pre-pandemic, 47% more flights operated, although only 20% up in terms of hours flown. The busiest airports for flight departures this month are Congonhas Sao Paolo, Al Maktoum Dubai, Ben Gurion Tel Aviv and Seletar Singapore. Almost all the activity is in domestic sectors, and longer connections are still behind pre-pandemic volumes, with flights over 6 hours down by 8%. The most obvious example of the ongoing effect of covid restrictions is China where business jet flights have declined by 70% compared to April 2021, down by 50% versus April 2019.