WINGX�s weekly Business Aviation Bulletin.

Summary

There was a big post-Easter pick-up in business jet demand, with a strong emphasis on leisure destinations. Demand has drained out of Russia and Ukraine, with negative spill over to Germany, but this is more than offset by big gains in Mediterranean markets. In the US, the Florida market is booming, supporting more modest growth on the West and East coasts.

Global

Business aviation activity was particularly strong in the last week compared to same week in 2019, which partly reflect Easter dates in this year compared to three years ago. Global business jet and turboprop activity is up 17% compared to 2019, above the 14% growth trend for the month and year so far. Slower turboprop activity is undercutting a surge in business jet demand, up 20% this year versus 2019, up 25% for week 17. Business aviation activity is racing ahead of the recovery in scheduled airlines, where passenger sectors are up 29% year-on-year but still trailing 27% versus comparable 2019. Cargo traffic has fallen back compared to pre-pandemic, 4% below trend in same week 2019.

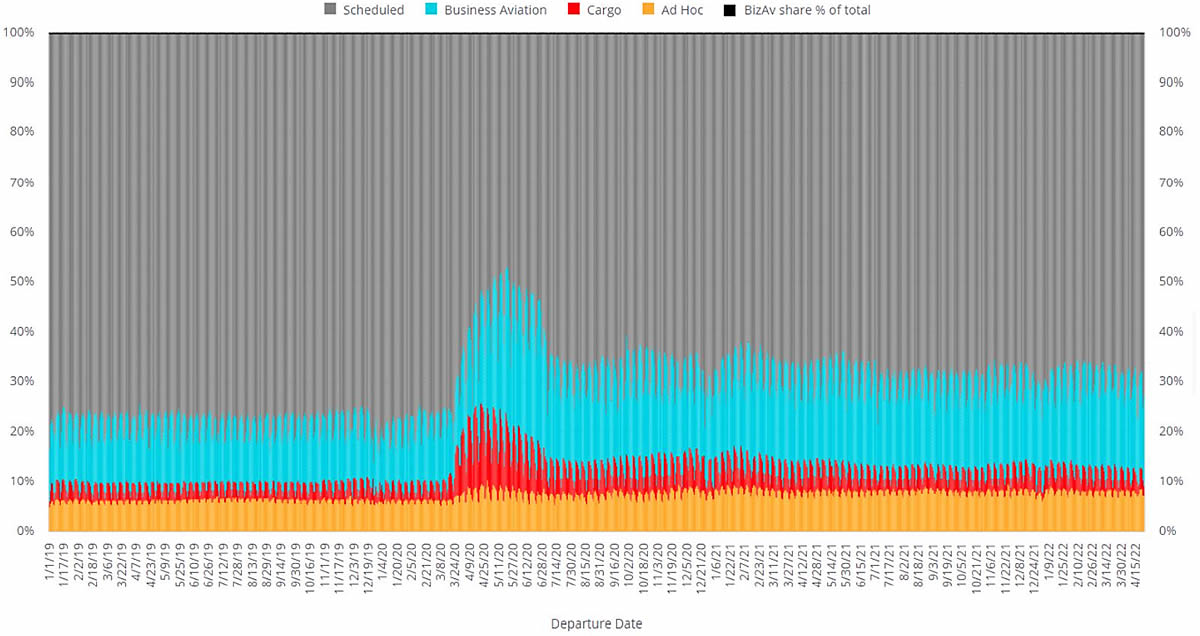

Business aviation flights share of total fixed wing activity since 2019

Russia and Ukraine

As the war in Ukraine moves towards a 3rd month, regional business aviation activity is crumbling away, with just 225 flights out of Russia, Belarus and Ukraine in the last week, 71% less than three years ago. This compares to 31% decline so far this year. Business jet activity comprises 2.6% of all flight activity out of the region in the last week. Most of this activity is within Russia – Vnukovo connections to Pulkovo, Sochi, Kazan and Surgut. Of the international destinations, the most popular are Istanbul, Dubai, Baku, Antalya, Tel Aviv, Tashkent. To put the decline of the Russia business jet market in context, last year, the 4th week of April saw 727 departures from the country, up 32% on the same week pre-pandemic. Back then, the UK, Latvia and Switzerland numbered in the top 5 country destinations.

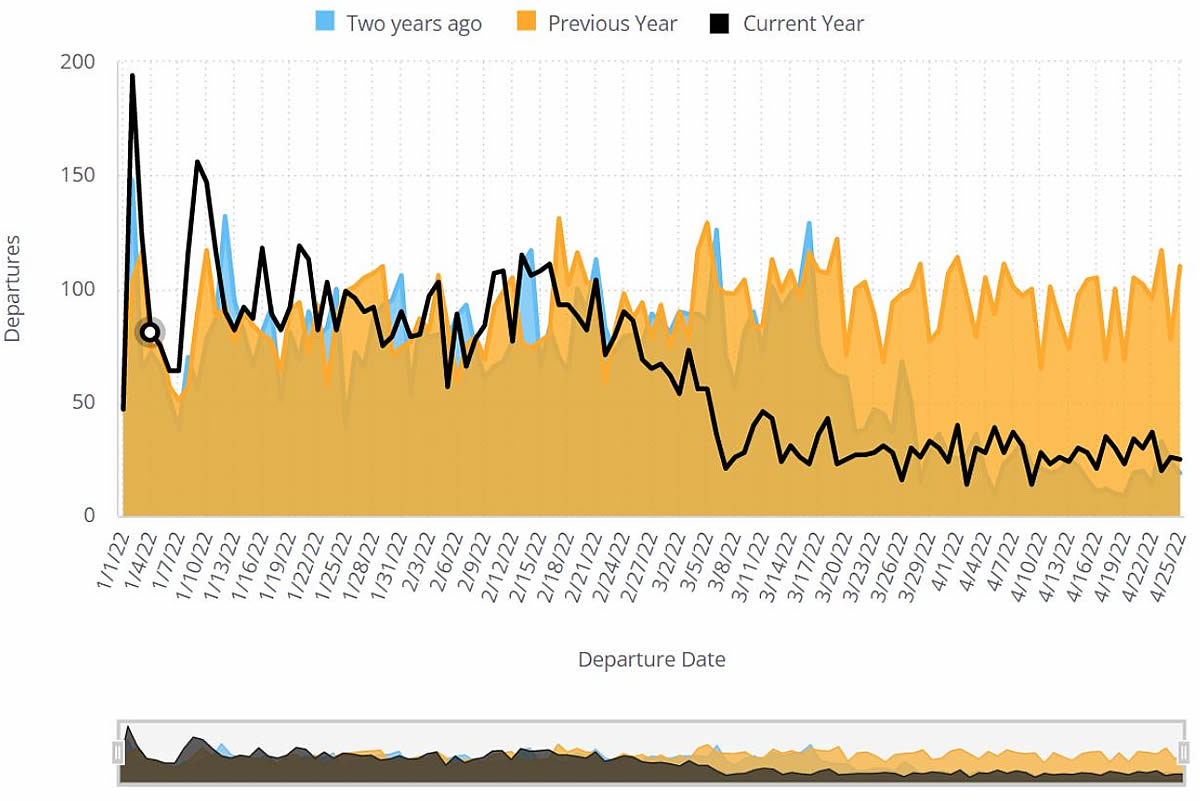

Business jet departures from Russia and Ukraine since 2019

Europe

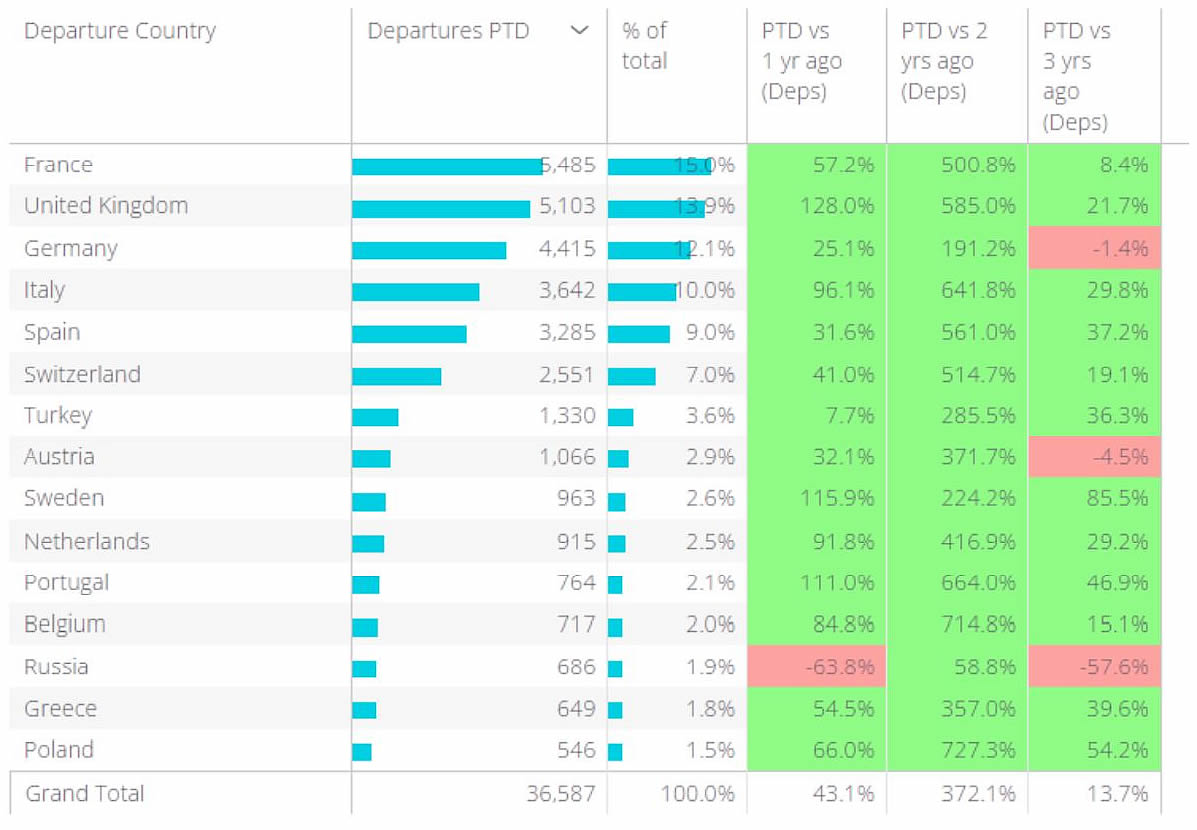

European business aviation demand was particularly strong in the last week, with just under 13,000 sectors operated in the last 7 days, up 17% on the previous week. Compared to week 17 last year, European bizjet traffic was up 25%. The UK and Italy are seeing the biggest upticks in activity. Compared to three years ago, Farnborough’s outbound traffic is up 37%, Biggin Hill up 59%, Oxford up 73%. Nice is their most popular destination. Out of Italy, Venice, Milan Linate and Ciampino are the busiest airports. Besides Vnukovo, there are some airports seeing declines, notably Vienna, Belgrade, Luxembourg, Innsbruck. Other airports are seeing vertiginous growth this Spring, typically “leisure” resorts such as Alicante, Bordeaux, Cascais, Faro, Ibiza.

Business aviation activity out of top European countries in Q1 2022

North America

Across the US, Mexico, Canada and the Caribbean, business jet activity is trending up by 23% for the period 18-25 April, compared to three years ago. Flight departures from the United States account for more than 90% of the activity, trended up by 28%, with 7% growth on flights flown in the previous 7 days. Puerto Rico, US Virgin Island and Costa Rica are seeing very strong growth, as they have done throughout the pandemic. Teterboro has retaken top spot in terms of busiest airport in the region, though strikingly still short of 2019 volumes. In contrast, departures from West Palm Beach airports are trending up by 93%. There have been 65 business jet flights between West Palm and Westchester in the last week, up by five times compared to pre-pandemic.

Business jet departures out of North America region in Jan-April 2022

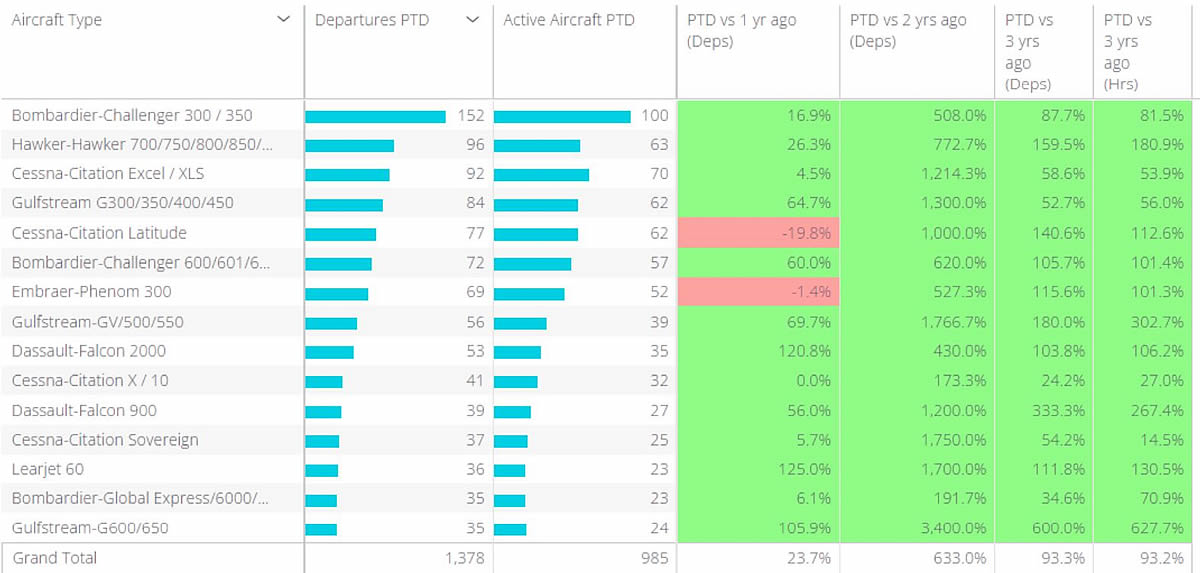

Zeroing in on the US market, the business jet types with largest active fleets are Challenger 300/350 and Citation Excel/XLS, a combined total of 1,150 active tails, with just under 9,000 sectors flown in the last 7 days. The Phenom 300 continues to be a highly demanded business jet, with activity compared to same week 3 years ago up by 53%. Fractional and Charter operations of the Phenom 300 is well above normal, close to 30% growth, but the biggest boost has come from private users, activity doubling compared to 2019. Besides NetJets and Flexjet, the busiest operators are Air Share, Summit Aviation, Maxair Charter.

Rest of World

Phenom 300 fleets are also flying more outside North American and European markets: 255 flights in the last week, up by 44% compared to 3 years ago. The busiest connections for this aircraft type are in Brazil, Nigeria and Australia. At the other end of the cabin-size spectrum, Ultra Long Range jets have flown just over 1,000 missions in the last 7 days, 11% less activity than the same week 3 years ago. Ultra Long Range jets with Pratt & Whitney engines installed flew 23% more sectors than 3 years ago, whereas the Rolls Royce installed ULR fleet few 24% less. The Dassault Falcon fleet had record demand, with Male, Abuja and Al Maktoum the most popular airports for 7X and 8X.