WINGX�s weekly Business Aviation Bulletin.

Summary

So far this month, we have seen a modest correction in the downward trend in flights in 2022 compared to 2021, at least in the US. With charter operating still dipping from last year´s highs, the impetus appears to be coming from aircraft owners and flight departments. European flight activity is ailing, particularly in Central Europe.

Global

In the first 11 days of September there were 165,576 business jet and prop sectors operated globally, 2% more than for same period 2021, up 17% compared to the same period in 2019. In week 36, 5th September through 11th September, business jet flights were up 8% compared to the previous week, 7% higher than week 36 last year. In the last the four weeks bizjets are flying 2% more than comparable last year. Airline traffic this month is still sluggish compared to 3 years ago, even if departures are up 13% compared to last year. Focussing on the top airlines, Southwest Airlines, American Airlines, Ryanair, Delta Airlines and United airlines, flights so far this month are 10% above last September, down only 1% compared to three years ago.

Global Fixed Wing activity 1st – 11th September 2022 compared to previous years

North America

Business jet and turboprop activity in North America across the first 11 days of September was 3% above last year, 13% above three years ago. Business jet demand so far this month is 4% above September last year, 18% above same period three years ago. Week 36 specifically saw a rebound in activity compared to the previous week, departures up by 12%. Compared with the same week last year, activity was up by 10%. In the last four weeks departures are up by 3% compared to last year.

In the United States bizjet activity has started September 4% above last year, 22% above three years ago. Private flight departments are the busiest fleets, departures are up 15% compared to last year, 38% above three years ago. Demand for branded charter fleets continues to decline from last year´s highs, activity 11% below September last year, aircraft management fleets saw a 2% decrease in activity compared to last September.

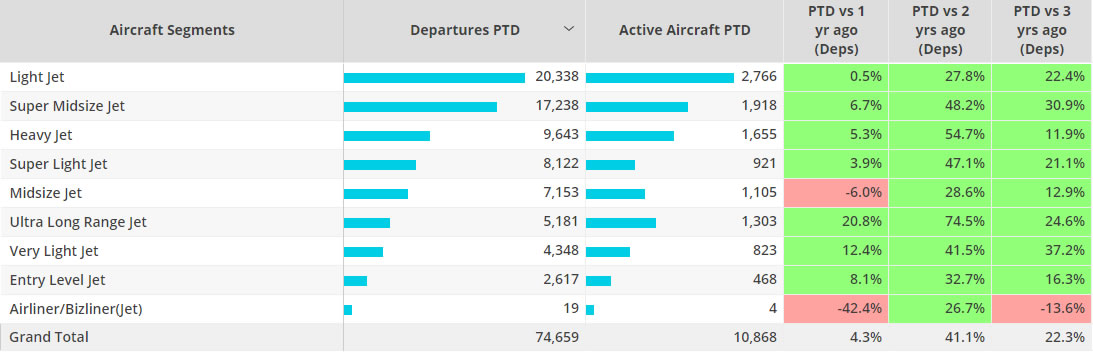

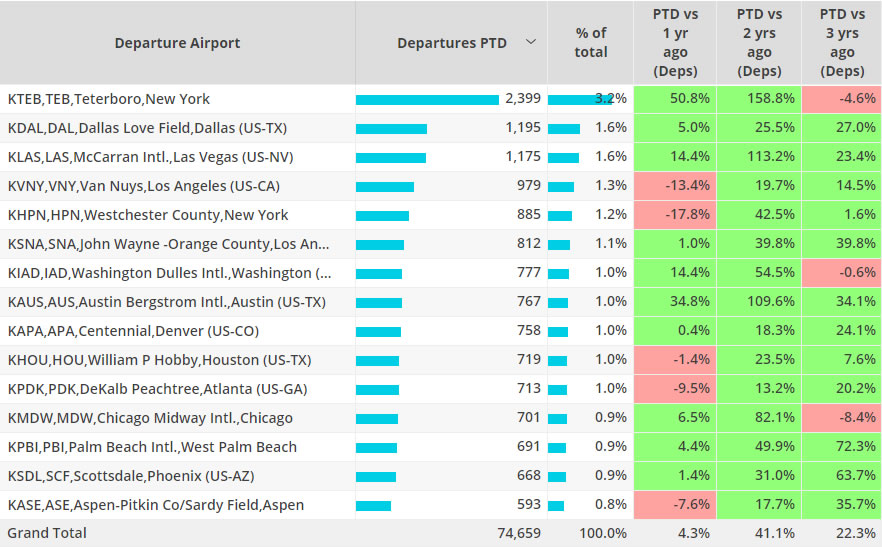

By airport, Teterboro is seeing a relatively belated recovery from the pandemic period, departures 50% above last September, although still 5% below three years ago. Neighbouring Westchester County is seeing departures 18% below September last year, only 2% above three years ago. By aircraft segment, the US is seeing a year-on year dip in Midsize and Bizliner activity. Light jets are contributing the most activity, with a big lead on September 2019, up 22%, but flat year on year. By contrast, Ultra Long Range jets are flying 21% more this year than last, and maintaining a 25% gain on September 2019. Very Light Jets have a the biggest gain on 2019, activity up almost 40% vs three years ago.

Top US bizjet aircraft segments September 2022 compared to previous years.

Busiest US airports for business jet activity September 2022 compared to previous years.

Europe

As September gets underway business jet activity is down 7% compared to September last year, although still 20% above three years ago. In the last four weeks activity has dropped 7% compared to last year, activity in week 36 fell a further 2% compared to the previous week. The UK saw the largest drop-in activity in the most recent week, flights down 10%, although 3% above week 35 in 2021. Despite increases in activity in the most recent week, flights in Germany and France saw double digit declines compared to the same September period in 2021.

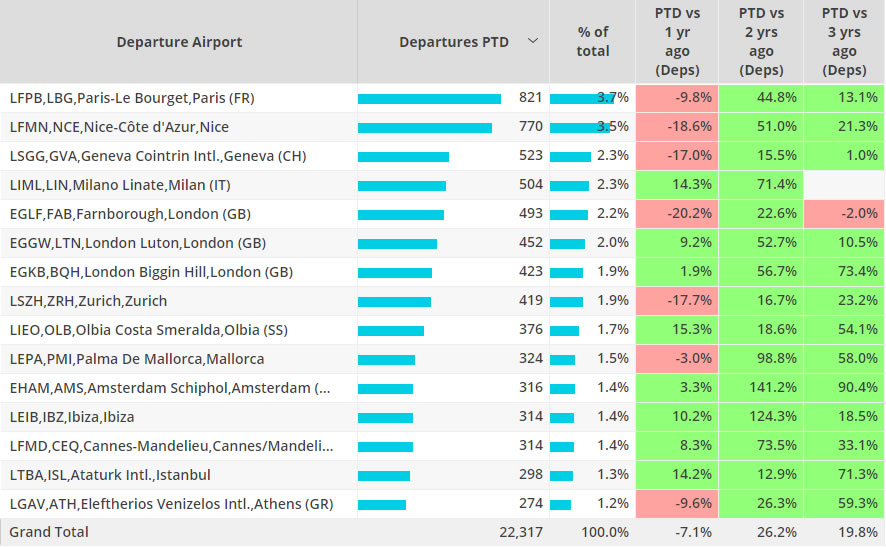

The top 3 busiest airports so far this month have seen a decline in activity compared to last year. Le Bourget seeing 10% fewer departures, Nice 19% fewer and Geneva 17% fewer. All three are up on three years ago, although Geneva edges over pre-pandemic 2019 by just 1%. Leisure spots Milan Linate and Olbia are seeing 14% and 15% growth compared to last year, Ibiza 10% busier than last September. Farnborough is experiencing a dip in activity this September, flights are down 20% compared to last year, 2% down on pre-pandemic September.

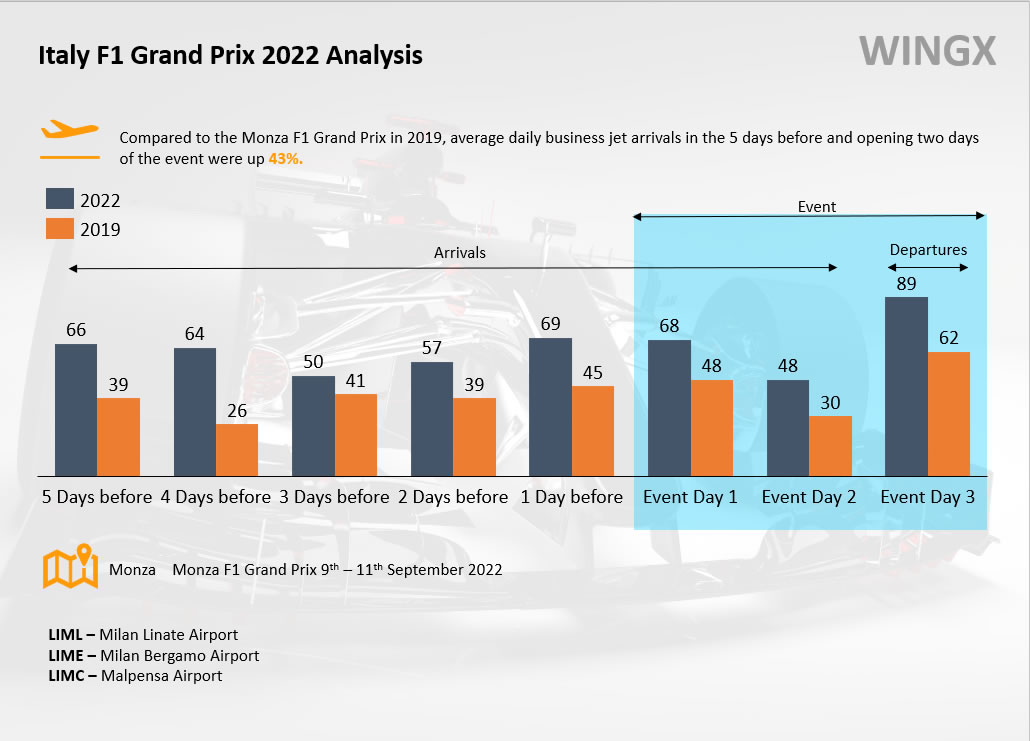

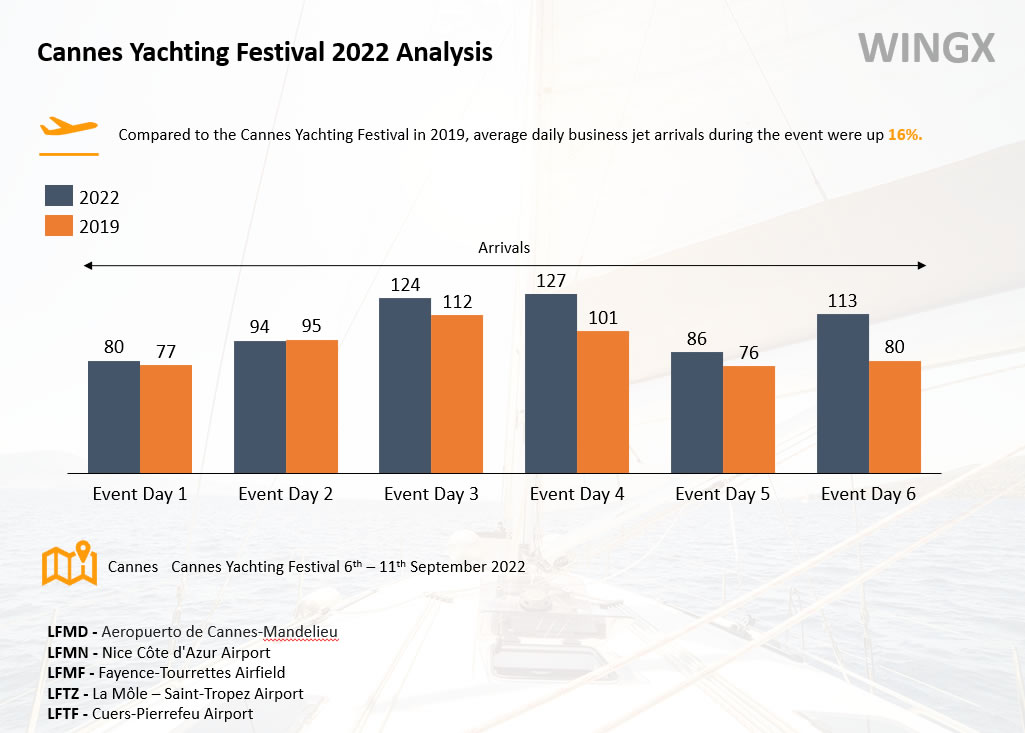

The Italian Grand Prix at Monza last week saw a 43% increase in average daily bizjet arrivals during the 5 days prior and first 2 days of the event compared to the 2019 Grand Prix. The Cannes yachting festival saw the average daily business jet arrivals at nearby airports increase by 16% compared to the 2019 event.

Business jet activity around Italy F1 Grand Prix 2022

Business Jet arrivals during Cannes Yachting Festival

European Business Jet airports, September 2022 compared to previous years

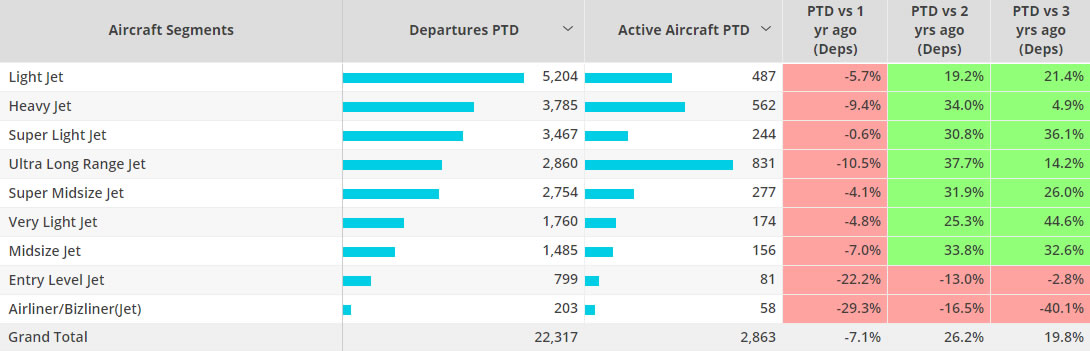

Business jet segments, Europe, September 2022 compared to previous years

Rest of World

Business jet activity outside of North America and Europe continues to trend upwards. Departures from 1st September through 11th are 14% above last year, 62% above three years ago. Sao Paulo remains the busiest airport, traffic trending 6% above last year. Brazil is the busiest ROW market, departures are almost double compared to the second busiest market, Australia. China and Morocco continue to see the largest slow down this month, departures from China are half of September last year, Morocco seeing a 30% drop-in activity. Japan and Columbia seeing a 6% drop-in activity compared to last year.

At the regional level the Middle East is seeing 15% growth in the last four weeks compared to last year, South America 11% and Asia 22%. In week 36 the Middle East saw a 1% drop compared to the previous week, although 19% higher than the same week last year.