WINGX�s weekly Business Aviation Bulletin.

Summary

We have seen the explosive charter demand relapse in the last month, compared to the high points in 2021, which may be a distraction as that spike was artificially boosted by the delayed loosening of lockdown restrictions. What is clear in the last month is that flight departments – both owners and corporate � are flying more than ever. It appears that the limited options on airlines are still out-weighing any downsides in terms of inflation and economic instability.

Global

In the first 18 days of September there were 279,105 business jet and prop sectors operated globally, 5% more than the same period 2021, up 17% compared to the same period in 2019. In week 37, 12th September through 18th September, business jet flights were up 4% compared to the previous week, 7% higher than week 37 last year. In the last four weeks bizjets are flying 4% more than comparable last year. Airline traffic remains sluggish compared to three years ago, however departures are up 13% compared to last year. Focussing on the top airlines, Southwest Airlines, American Airlines, Ryanair, Delta Airlines and United airlines, flights so far this month have rebounded above pre-pandemic levels by 1%, 16% above last year.

Global Fixed Wing activity 1st � 18th September 2022 compared to previous years

North America

Business jet and turboprop activity in North America across the first 18 days of September was 6% above last year, 13% above three years ago. Business jet demand so far this month is 7% above September last year, 19% above the same period three years ago. Week 37 saw a 5% rebound in activity compared to the previous week, that week a 12% rebound on week 35, indicating an acceleration in demand through September.

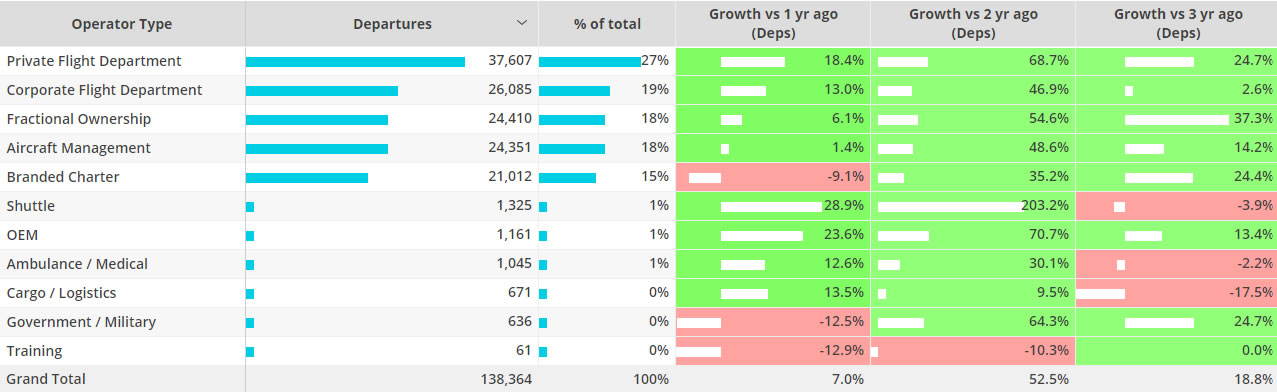

North America Bizjet Operator Types � 1st � 18th September compared to previous years

In the United States bizjet activity so far this September is 7% above last year, 23% above three years ago. In week 37 demand increased 5% over the previous week, 10% ahead of week 35 last year. In the last four weeks demand is 7% above the same period last year. Private flight departments flew 19% above last year, 36% above three years ago. Corporate flight departments are seeing modest gains compared to three years ago, 5% above, 13% growth compared to last year. Demand for branded charter flights is down 9% compared to last year, although up 25% compared to three years ago.

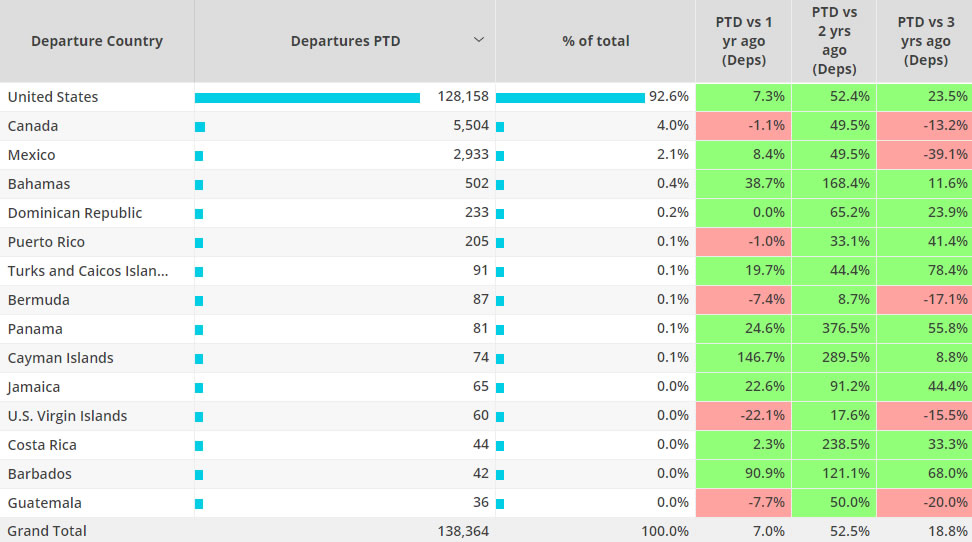

Busiest North American markets 1st � 18th September 2022 compared to previous years

Europe

Business jet activity is 8% below September last year, although 19% above three years ago. In the last four weeks activity has dropped 8% compared to last year, activity in week 37 fell a further 1% compared to the previous week. Despite this region-wide dip, activity in the UK was on par with the previous week, Germany saw a 10% rebound. France and Switzerland saw a 5% and 3% decline in week-on-week activity, both double digit decline compared to the same period in 2021.

During the week of HM Queen Elizabeth’s death, week 36, arrivals into RAF Northolt were up 13% compared to the previous week. Arrivals into Aberdeen airport were up 145% in week 36 compared to the previous week. Other London bizjet hotspots were down week to week, London City down 31%, Biggin Hill down 25%, Luton down 16%, Stansted down 12%. Looking at the Friday � Monday period of the state funeral, arrivals into RAF Northolt were up 13% compared to the previous Friday � Monday period, 29% below the last August bank holiday Friday � Monday weekend. Arrivals into Stansted were 11% above the previous weekend, 15% above the previous Bank Holiday Friday � Monday.

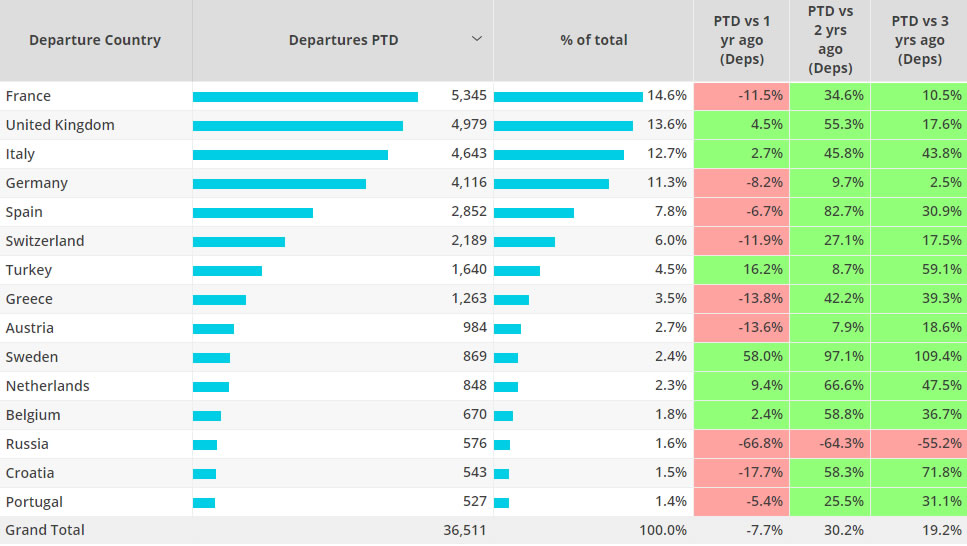

Top European Business Jet Markets 1st � 18th September 2022

Rest of World

Business jet activity outside of North America and Europe continues to trend upwards. For example, business jet flights from the Middle East are up 18% in the last four weeks compared to last year, Africa up 4%, Asia up 21% and South America up 9%. Departures through September 2022 are 16% above last year across all ROW regions, 59% above three years ago. Sao Paulo is the busiest airport, although activity is dipping below last year. Seletar is seeing triple digit growth compared to last year, Ben Gurion and Al Maktoum both seeing 51% growth compared to last year. Columbia and Morocco are seeing a 9% and 27% respective slowdown in flights compared to last year. Flights from China are half of last September, down 41% compared to three years ago.