WINGX�s weekly Business Aviation Bulletin.

Summary

This month we have seen pronounced slowdown in European bizjet activity compared to September 2021, although flights are still up 17% compared to September 2019. The softening market is partly due to last year´s late summer seasonal peak, but it´s clear that macro concerns are also eating into demand. The US bizjet market is still hitting new peaks, with corporate and owner traffic driving momentum.

Global

Just over 400,000 business jet and prop sectors were operated globally in the first 26 days of September 2022, 4% more than the same period in 2021, up 14% compared to three years ago. Focusing on business jets, activity so far in September is 3% above last year, 19% above three years ago. In the last four weeks activity has been 4% above last year. So far in September, overall passenger airline traffic is 21% behind three years ago, though 13% above the same period in September last year. Focusing on the top global airlines Southwest Airlines, American Airlines, Ryanair, Delta Airlines and United airlines, flights so far this month are 16% above last year, rebounding to less than 1% below comparable 2019.

Global Fixed Wing activity 1st – 26th September 2022 compared to previous years

North America

Business jet activity in North America across the first 26 days of September was 5% above last year, 17% above three years ago. Activity in the last four weeks is 7% above last year, with week 38 up 1% increase compared to week 37 and 5% up on same week last year.

North America Bizjet Operator Types � 1st � 26th September compared to previous years.

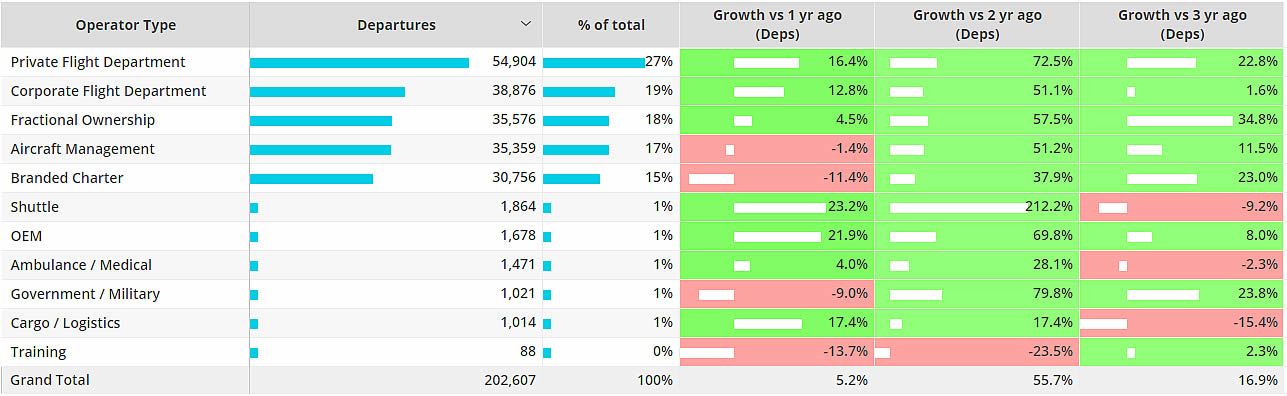

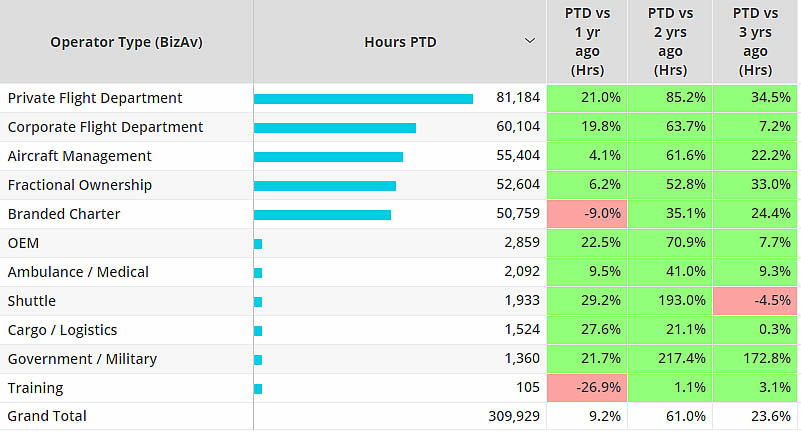

In the United States bizjet activity so far this month is 5% above last year, 21% above three years ago. In the last four weeks activity is 7% above last year, with week 38 activity 1% higher than the previous week, 5% above week 38 last year. In the last four-week period bizjet demand in the US has been driven by private flight departments, these fleets flying 19% more than last year, 34% above three years ago. Corporate flight departments are flying 16% more than last year, 6% more than three years ago. Aircraft management programs are flying 1% more than last year, 15% more than three years ago. Branded charter fleets are seeing declines compared to last year, 11% fewer flights in the four weeks compared to last year, although flight hours are down 9% compared to last year.

US Business jet hours by operator type, last four weeks (29th August � 25th September) compared to previous years.

Europe

Business jet activity has stalled to 9% below September last year, so far this month, though still 17% above three years ago. In the last four weeks activity is 9% lower than last year, activity in week 38 fell a further 3% compared to the previous week. In the last four weeks private flight departments are flying 28% more than last year, fractional programmes 5% more than last year. Aircraft management and branded charter are seeing big declines compared last year, activity in the last four weeks down 18% and 13% respectively.

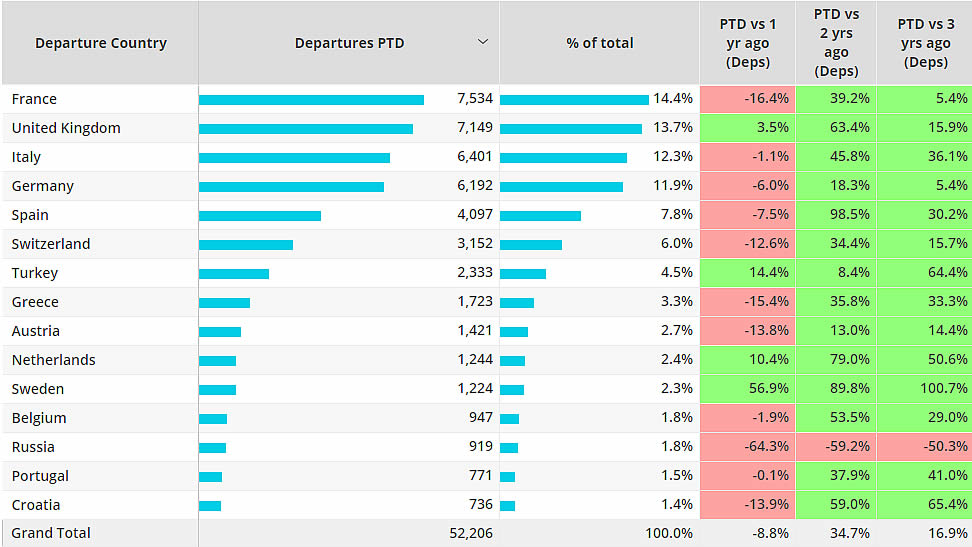

Top European Bizjet markets 1st � 26th September 2022 vs previous years

Bucking the regional trend in Europe, business jet activity in the UK, Turkey, Netherlands and Sweden is well ahead of last year. The largest contributor this month in the UK is coming from Aircraft Management operators, although this activity is 4% below where it was in September last year. Whereas branded charter in the UK is down 10%, Fractional and Private flight departments are seeing double digit growth compared to last year, up 20% and 33% respectively.

Rest of World

Business jet activity outside of North America and Europe continues to trend upwards. In the last four weeks activity in the Middle East is up 18% compared to September last year, Africa 3%, Asia up 24% and South America 9%. Departures through September 2022 are 19% above last year, 55% above three years ago across all ROW regions. Sao Paulo is the busiest airport through September, departures 3% above last year. Seletar continues to see triple digit growth compared to last year, Ben Gurion seeing 50% growth and Al Maktoum 29% compared last year. Columbia and Morocco are experiencing a dip, departures are down 8% and 19% retrospectively. Departures from China are half of what they were of last year, down 45% from three years ago.