WINGX�s weekly Business Aviation Bulletin.

Summary

Geopolitical instability, currency market turbulence and runaway inflation has undermined business and consumer confidence and in Europe this is feeding through to lower demand for business jet travel, well down on last year´s early Autumn peaks. In the US, the charter market continues to taper, but still holds at a higher level than in any period pre-pandemic.

Global

Twenty-four days into October global business jet and prop activity is 1% behind the same October period last year, 11% above pre-pandemic October 2019. For business jets only, activity is 3% below October last year, 16% above three years ago. Global passenger airlines are 23% behind pre-pandemic October, although 8% above last year. The top global airlines – Southwest Airlines, American Airlines, Ryanair, Delta Airlines and United airlines, are flying 15% above last year so far this month, 1% below three years ago. Dedicated freight activity is 8% behind last year, 5% behind three years ago.

Global Fixed Wing activity October 2022 compared to previous years

North America

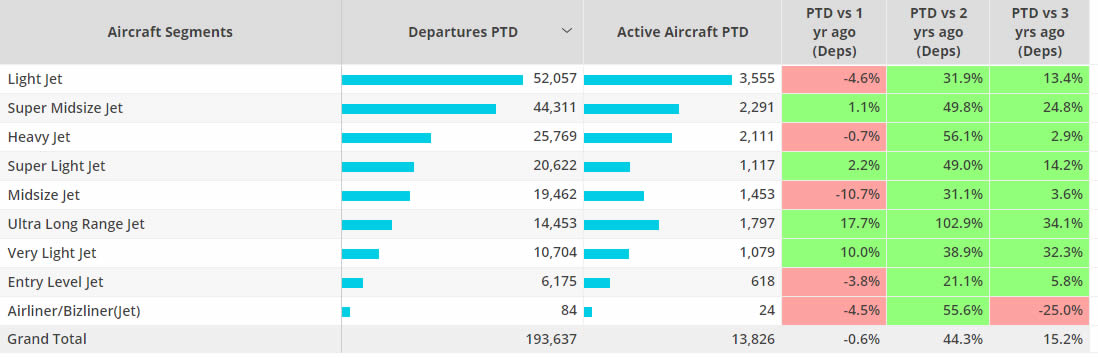

So far this month business jets are flying 1% less than last year, 15% above three years ago. In week 42 ending 23rd October, activity across the region was on par with same week last year, also level with week 41 this year. In the last four weeks business jet sectors are trending at 1% below the same period last year. Light jet is the busiest segment across the region this October, although this activity is down 5% compared to last year. Super Midsize, Super Light, Ultra Long Range and Very Light Jets are flying more than last year, whilst Light, Heavy, Midsize, Entry Level and Bizliners are flying less.

North American Business jet segments, October 2022 compared to previous years

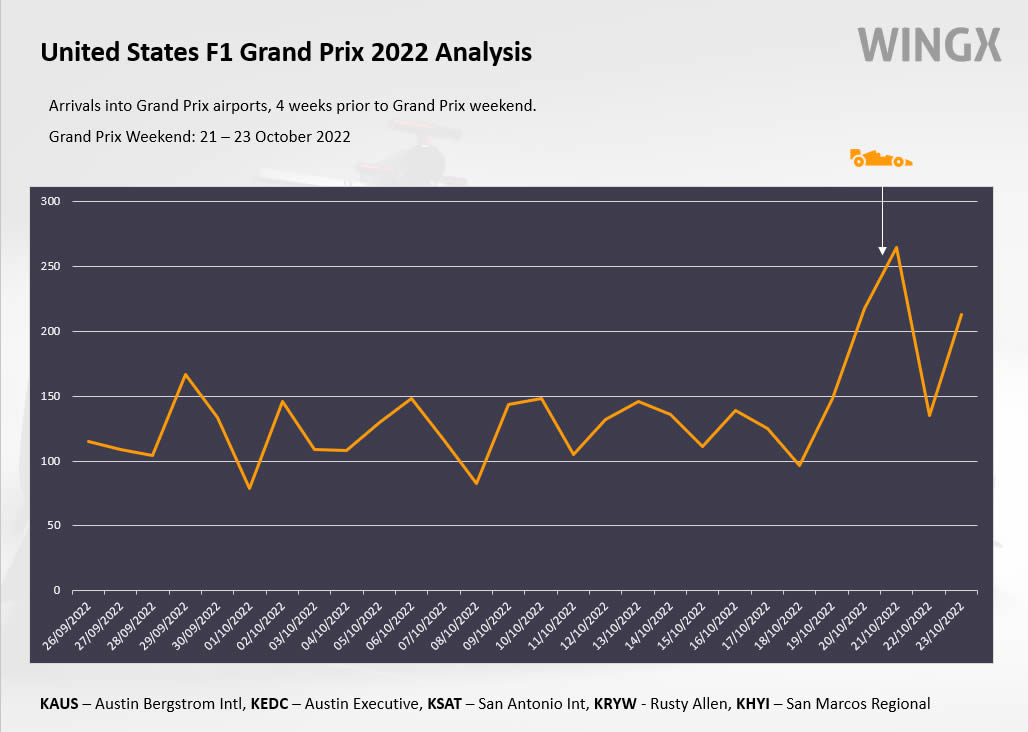

The US Grand Prix at the Circuit of The Americas on 20-21 October reportedly drew the biggest ever F1 spectator crowd. For those arriving by business jet, there was notable activity at nearby airports (KAUS, KEDC, KSAT, KRYW, KHYI). Compared to the 2019 US Grand Prix, average bizjet arrivals during the 5 days prior to the event was up 37%. During this year’s Grand Prix event there were 538 active aircraft, 74% more than at the 2019 event. In Orlando NBAA-BACE caused a spike in business jet arrivals at Orlando airports compared to normal activity levels. During the conference there were 406 active business jets at nearby airports, 4% more than the 2019 event in Las Vegas.

Arrivals into US Grand Prix airports, last four weeks

Europe

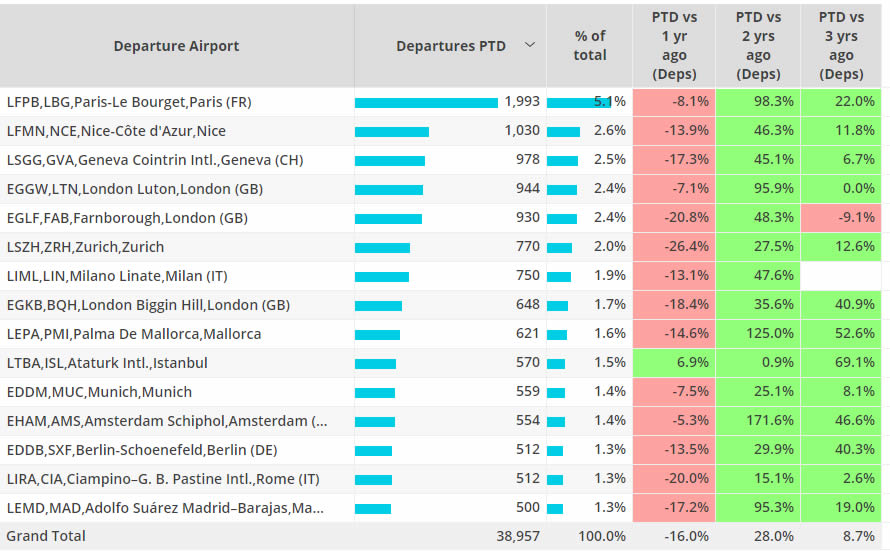

So far this month business jet activity in Europe is 16% below October last year, despite this drop, activity is 9% above pre-pandemic October. In the last four weeks activity has dropped 14% compared to last year, 16% in the last week. Activity out of France, the busiest European market is down 15% compared to last year, although 4% above three years ago. Flights out of Germany are 12% below last year, less than 1% below three years ago. Austria is also experiencing a drop in demand compared to three years ago, flights are down 7%. Out of the 10 busiest bizjet airports, Ataturk is the only to see activity above last year. Luton is on par with three years ago, while Farnborough 9% below three years ago.

Business jet activity trends by European airport in October 2022

Rest of World

Outside of North America and Europe, business jet activity is 16% above last year, 50% above three years ago. Just under 16,000 flights were operated in the first 24 days of October, Brazil is the busiest market. Business jet flights in China have halved compared to three years ago, a 64% decrease compared to last year. In the last four weeks, bizjet activity in the Middle East is 5% above last year, Africa 10% above last year and Asia 23% above last year. Demand in the ROW region is coming from private flight departments, activity is 27% above last year, 96% above three years ago.