WINGX�s weekly Business Aviation Bulletin.

Summary

The downwards slide in business jet activity is apparent in the US as well as Europe, notably in the charter market. On the anniversary of the start of the Ukraine war, the loss of the Russian business jet market is apparent, with biggest impact on the heavy jet charter market. There are growth areas outside Europe and the US, notably in the Middle East and Asia.

Global

Worldwide business jet sectors in Week 7 of 2023, 13th February through 19th February, amounted to 71,097 sectors, a 6% increase compared to Week 6 2023, and a 4% decrease compared to the same dates in 2022. The global trend for the last 4 weeks is 2% below comparable last year. Global Part135 and Part 91K bizjet activity in week 7 was 12% below the same dates last year. Combined business jet and turboprop activity between February 1st and 20th was 1% below last year, 12% ahead of February 2019. Scheduled airline sectors are 25% ahead of February last year, still 16% behind pre-pandemic 2019. Focussing on the top 5 busiest airlines (Southwest Airlines, American Airlines, Delta Airlines, United, Ryanair), sectors so far this month are up 15% compared to last year, 6% ahead of 2019.

Global fixed wing flights, 1st – 20th February 2023 compared to previous years.�(Note business aviation includes turboprops)

North America

In week 7, 55,678 bizjet sectors were flown, a 7% increase compared to week 6, a 6% decrease compared to the same dates in 2022. In the last four weeks activity is 3% down compared to the same dates last year.

150,000 bizjet sectors have flown out of airports in North America in February 2023 so far, 3% behind the same 20-day period in February 2022, 11% ahead of 2019. Year to date 370,000 bizjet sectors have been flown, 1% behind comparable 2022, 13% ahead of 2019. So far this month 89% of bizjet activity has been domestic flights, although sectors are down 4% compared to February last year, up 13% compared to 2019. International sectors are up by 4% compared to last year, 3% ahead of 2019.

So far this month bizjet activity in the United States is trailing last year by 4%, although 15% ahead of pre-pandemic February 2019. Major bizjet hotspots are down compared to last year, departures from Teterboro are down 3%, Palm Beach down 6% and Van Nuys down 5%, McCarran bucks the trend, departures are up 2% compared to last year. Florida is the busiest state so far this month, although departures are down 9% compared to last February, California 10% behind last year, Texas 8% behind.

This Presidents’ Day holiday weekend (Friday 17th � Monday 20th) saw just over 29,000 business jet departures from United States airports, 10% fewer than the Friday � Monday holiday period last year, although 23% more than in 2019. Palm Beach was the busiest departure point this year, followed by Teterboro. Private flight departments were the busiest operator types this holiday, Friday the busiest departure day.

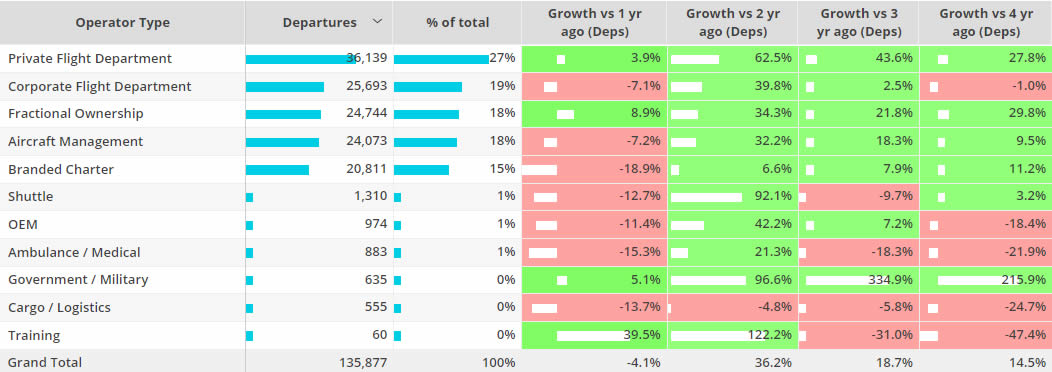

United States bizjet operator types, February 1st � 20th 2023, compared to previous years.

Europe

In Europe, 10,126 bizjet sectors were flown in week 7, 4% higher than week 6, a 1% decrease compared to the same dates in 2022. In the last four weeks activity is 5% below the same dates last year. So far this month bizjet activity has dropped by 7% compared to last year, although 10% ahead of pre-pandemic 2019. Excluding Russia and the trends look more favourable, sectors down just 4% compared to last February, 14% ahead of 2019. The year-to-date trend for Europe (including Russia) is down 7% compared to last year, 7% ahead of 2019.

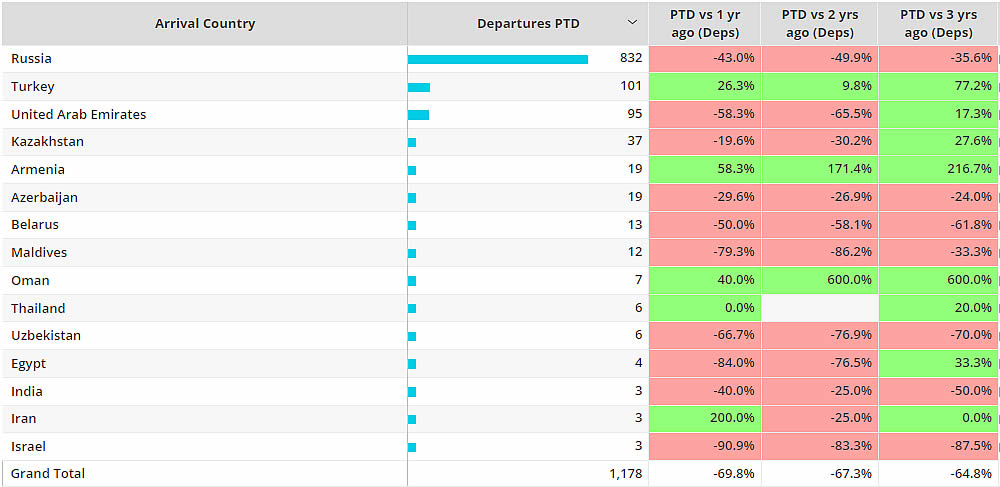

Year to date bizjet departures from Russia are down 70% compared to the same period last year, 62% below comparable 2019. International bizjet flights are down by 86% compared to last year, 82% compared to 2019.

Business jet arrival countries from Russia, January 1st � February 20th 2023 compared to previous years.

Bizjet and “other” aircraft activity in Turkey remains high due to humanitarian efforts following the Turkey-Syria earthquake. Business jet activity is 81% higher than February last year, 127% higher than 2019. Ataturk International is the busiest bizjet departure point this month, activity up 28% compared to last year, triple digit growth compared to 2019. Elsewhere there is triple digit growth compared to last year at Istanbul, Esenboğa International, Adana, and Gaziantep International airports.

Business jet and �other� sectors from Turkey, 1st � 20th February 2023 compared to previous years.

Business jet flights trends, Turkey, 1st � 20th February 2023 vs previous years.

Rest of World

In Week 7, 13th February through 19th February, activity in Africa was 19% ahead of the same dates last year, Asia 20%, Middle East was 32% and South America was 19%. The top 3 ROW countries so far this month are Brazil, India and Australia. Al Maktoum is the busiest airport the ROW region, although sectors are down 5% compared to last year, triple digit growth compared 2019, Congonhas down 1% compared last year, up 94% compared to 2019.

Bizjet sectors in China this month are 7% above last year, although 6% below 2019. Year to date bizjet sectors from China are up 22% compared to last year, 4% above 2019. Year to date almost half of bizjet flights from China are between 1.5 � 3hours in length, flights of this duration are up 14% compared to last year, 6% more than 2019. Long Haul and Ultra Long Bizjet flights are still way behind 2019 levels, year to date flights between 6-12 hours in duration are down 54% compared to 2019, 12+ hour flights are down 71% compared to 2019.