WINGX�s weekly Business Aviation Bulletin.

Summary

Bizjet flight activity in Germany has slipped back an eye-watering 27% in April 2023 compared to April 2019. Other countries in Europe are also seeing big declines, with the overall region now below the 2019 waterline. The US is now trending 10% below the record peaks last year but still double figures above 2019.

Global

Global bizjet sectors in Week 15, April 10th through 16th, amounted to 70,657 sectors, 8% more than the previous week, 4% fewer than the same dates last year. In the last 4 weeks the global trend for business jet activity has been at 9% below the same dates in 2022, 11% ahead of 2019. In the last four weeks worldwide Part 135 & 91K activity is trending 14% behind the same dates in 2022, but still up 24% vs comparable 2019. Scheduled airline activity continues to recover, so far this month 16% ahead of last year, but still trends 16% below April 2019.

Chart 1: Global fixed wing flights, April 1st – 17th 2023 compared to previous years. (Note business aviation includes turboprops)

North America

In Week 15, North American bizjet sectors amounted to 55,798 sectors, 8% more than Week 14, 5% fewer than the same dates in 2022. In the last four weeks the trend has been 11% below the same dates in 2022. In Week 15 Part 135 and 91K sectors were 3% ahead of the previous week, 9% below the same dates last year.

91% of bizjet departures in the North America region are from the United States, sectors are down 11% compared to last April, 12% ahead of 2019. Second ranked Mexico is seeing activity 1% below last year, still 37% behind 2019. Third ranked Canada is well behind April last year, sectors down 23%, 37% behind 2019.

Teterboro is the busiest bizjet airport in the region so far this month. Departures are down 11% compared to last year, 8% below April 2019. Palm Beach is seeing activity 6% below last year, Dallas Love Field 8% below, Opa-Locka 12% below.

The Bombardier Challenger 300/350 has flown the most flights so far this month, although departures are down 7% compared to last year, 12% ahead of last year. The Embraer Phenom 300 is the only aircraft in the top 3 to have flown more sectors compared to April 2022.

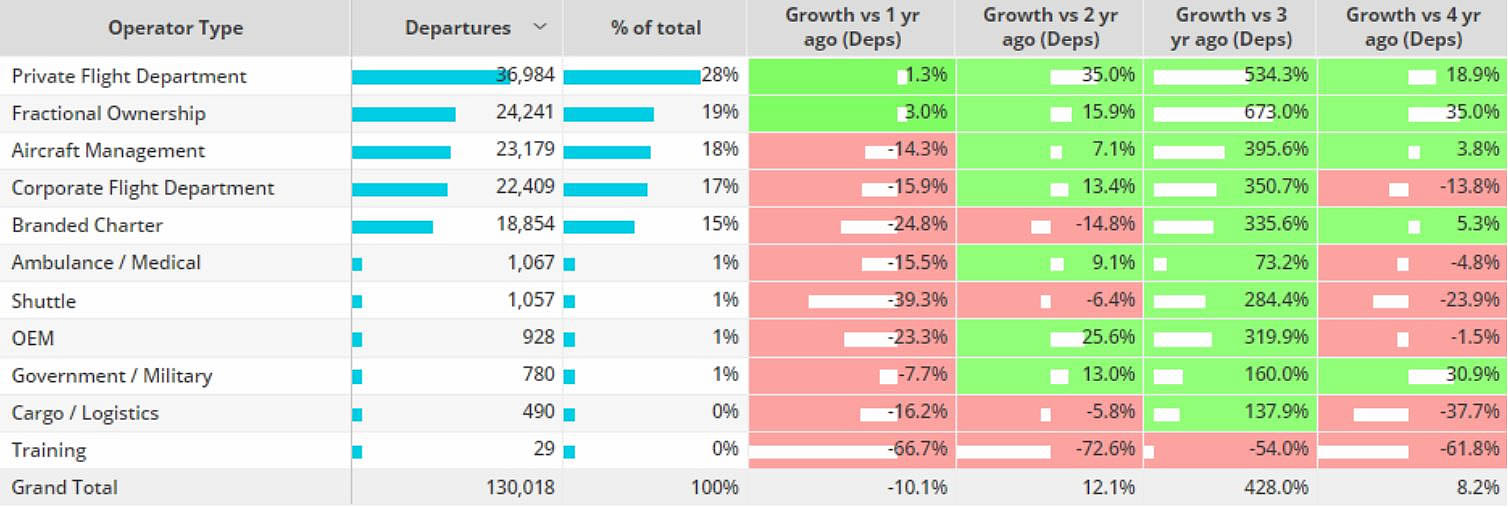

Branded Charter bizjet sectors have fallen 25% compared to April last year, although 5% more than 2019. So far this month only private flight departments and fractional fleets are flying more than last year, both seeing double digit growth compared to 2019.

Chart 2: North America Business Jet Operator Types, 1st � 17th April 2023 compared to previous years.

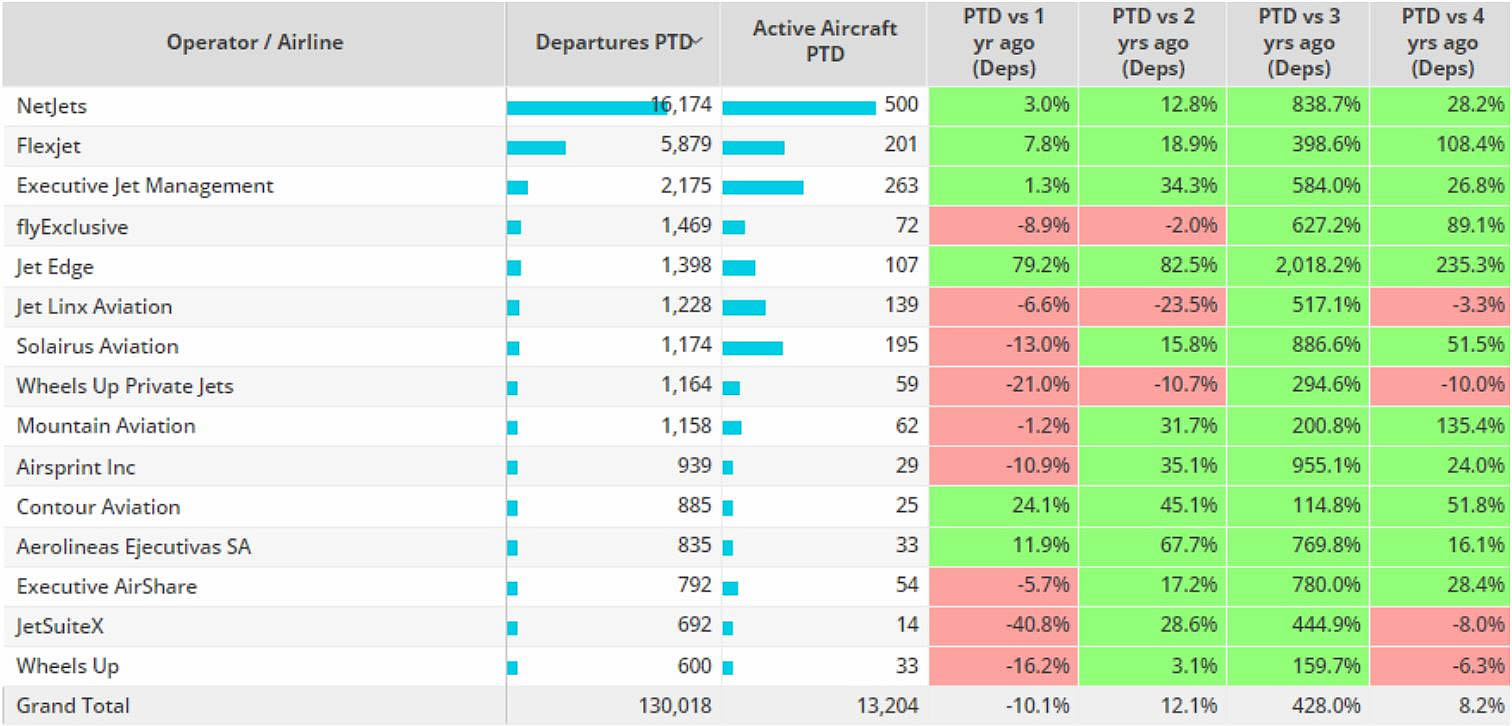

Chart 3: North American bizjet flights by operator, April 1st � 17th 2023 compared to previous years.

Europe

In Week 15 there were 9,553 bizjet departures from Europe, 8% more than week 14, 4% fewer than the same dates in 2022. In the last 4 weeks the trend has been 8% below the same dates in 2022.

So far this month European bizjet activity is down 7% compared to the same period last year, 3% below the same period in 2019. Excluding Russia and the trend is 7% below last year, on par with 2019. Part 135 & 91K bizjet sectors this month are 11% down compared to last year, 1% more than 2019. Part 91 activity is 5% ahead of last April, 12% behind 2019.

Le Bourget is the busiest bizjet airport in Europe so far this month, activity in decline compared to pre-pandemic April as well as last year. Sectors are down 14% compared to April 2022, 4% below 2019. Nice is well ahead of last year, departures are up by 14% compared to April 2022, 20% ahead of 2019.

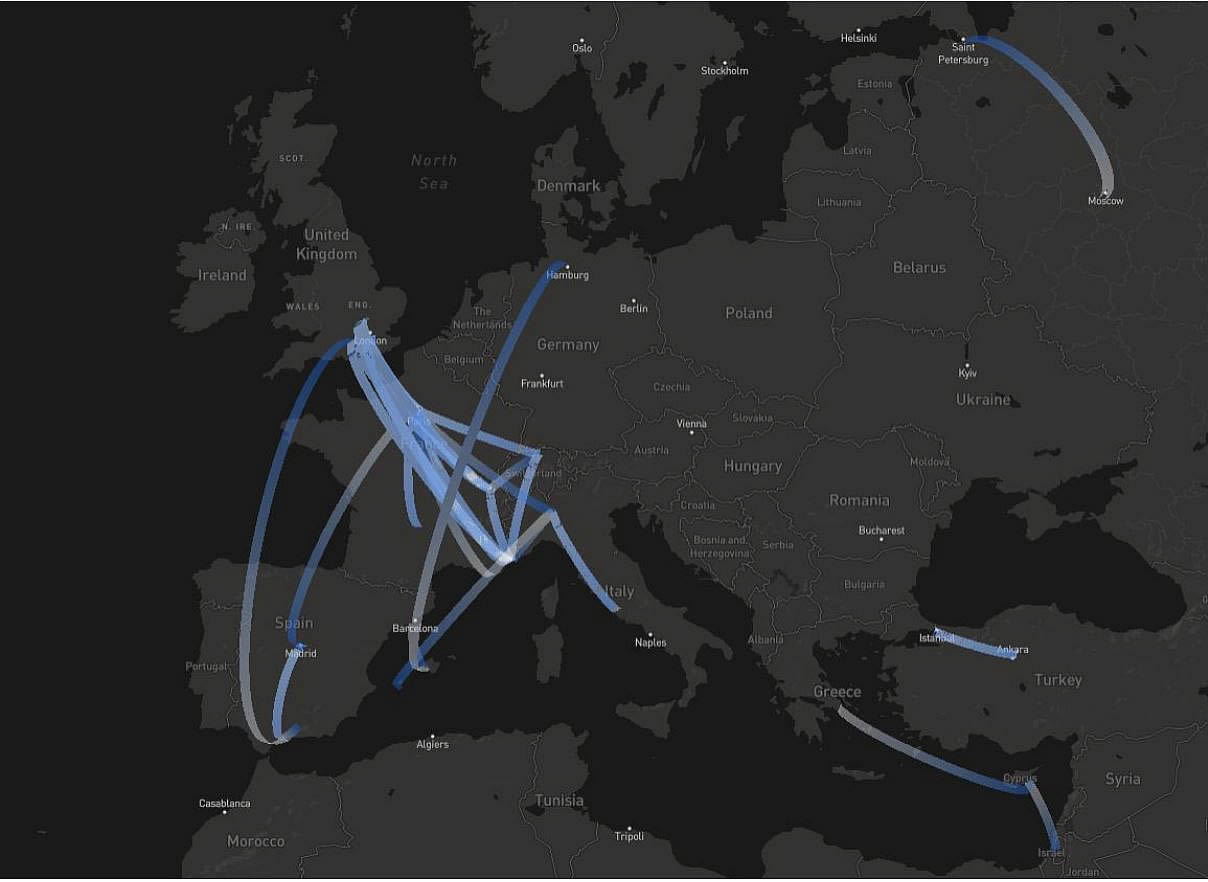

Chart 4: Top Airport Pairs, Bizjets Europe April 1st � 17th 2023

Most bizjet flights this month have been on Aircraft Management fleets, departures down 18% compared to 2019, 13% down on last April. Branded Charter flights are down 7% compared April last year, although 4% ahead of 2019. Private and Fractional fleets are seeing double digit growth compared to 2019, 1% and 6% compared to last year retrospectively.

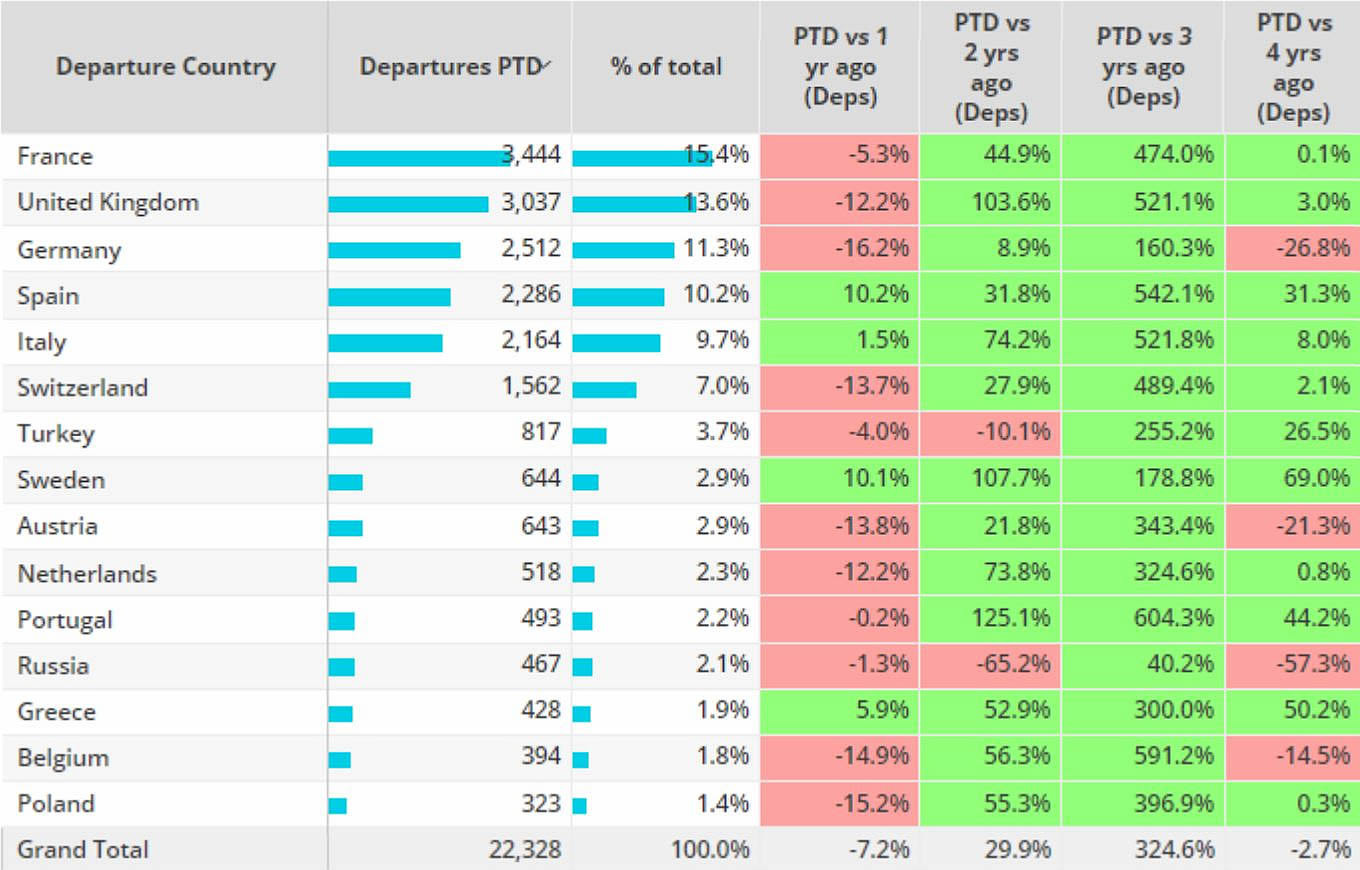

Chart 5: Top European Business Jet Markets, April 1st � 17th 2023 compared to previous years.

Rest of World

In Week 15 bizjet departures in Africa were 1% below the same dates in 2022, Asia up 17%, South America up 37%, Middle East down 4%. Excluding North America & Europe, bizjet activity in the Rest of World region is 8% ahead of last April, 58% ahead of 2019.

Brazil is the busiest market this month, demand is down 1% compared to last year, 89% above 2019. Argentina, Japan and China are seeing triple digit growth compared to last year.

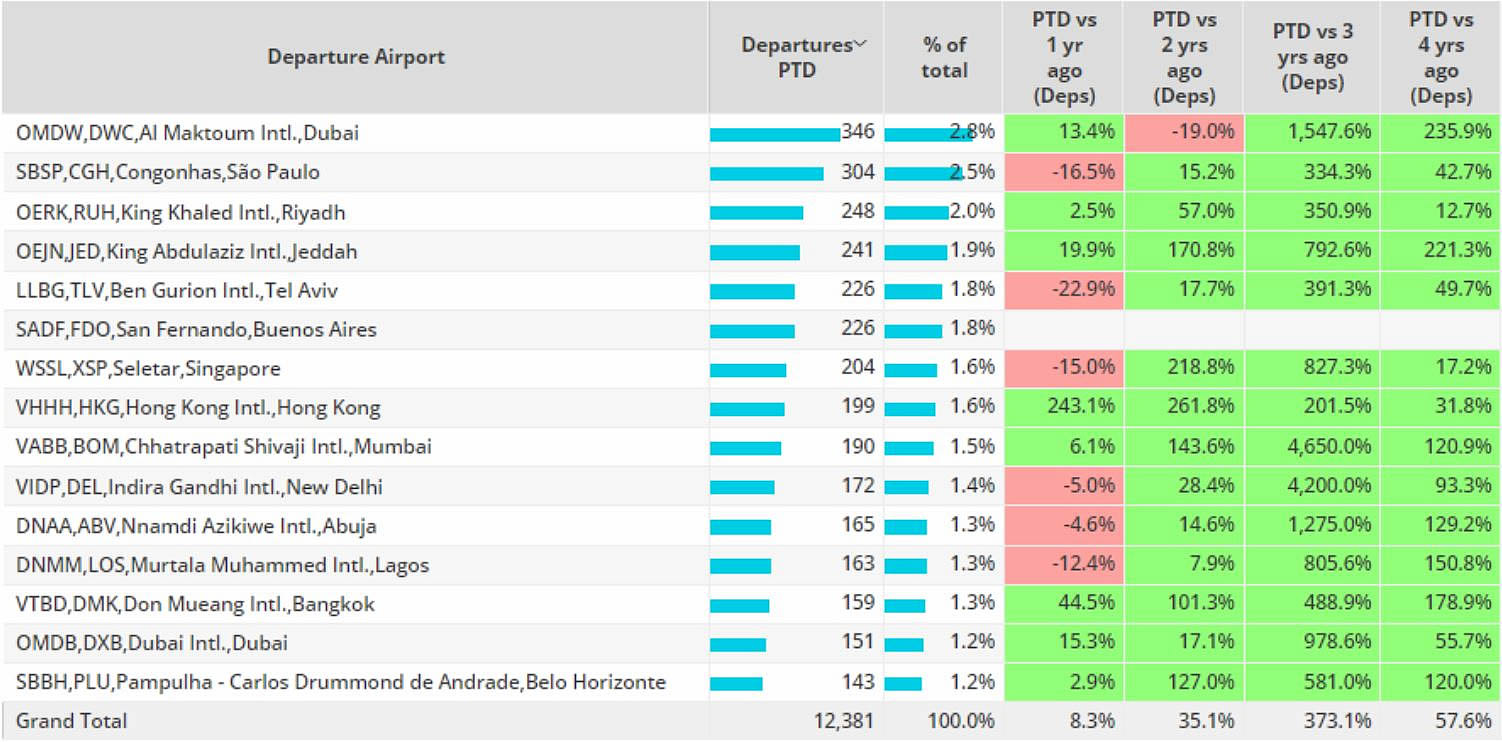

China sectors are down 6% compared to 2019. Year to date bizjets in China are flying 42% more sectors than comparable 2022, 5% below 2019. Elsewhere Al Maktoum is the busiest ROW airport, triple digit growth vs 2019. Congonhas, Ben Gurion and Seletar are seeing declines vs last April.

Chart 6: Top ROW airports, bizjets, 1st � 17th April 2023 vs previous years.