WINGX’s weekly Business Aviation Bulletin.

Summary

Business jet demand has fallen well off last year’s peaks, but at least appears to be stabilising at around 10% down compared to the Spring of 2022. As growth trends started to taper last summer, we expect to see a narrower year-on-year deficit in the next few months of 2023, barring further economic shocks, especially in the banking sector.

Global

In Week 17 Global business jet activity fell 1% compared to the previous week, 10% below the same dates in 2022. In the last four weeks activity has fallen 9% below comparable 2022. Year to date (1st January – 30th April), business jet and turboprop sectors have fallen 3% behind the same period last year, despite 14% gains over comparable 2019. Year-to-date business jet activity is further behind, sectors are down 5% compared to the first 4 months of 2022, although 16% ahead of 2019. Year-to-date scheduled airline activity has grown 20% compared to last year, still lagging 14% behind pre-pandemic 2019.

Chart 1: Global fixed wing flights, January 1st – April 30th 2023 compared to previous years. (Note business aviation includes turboprops)

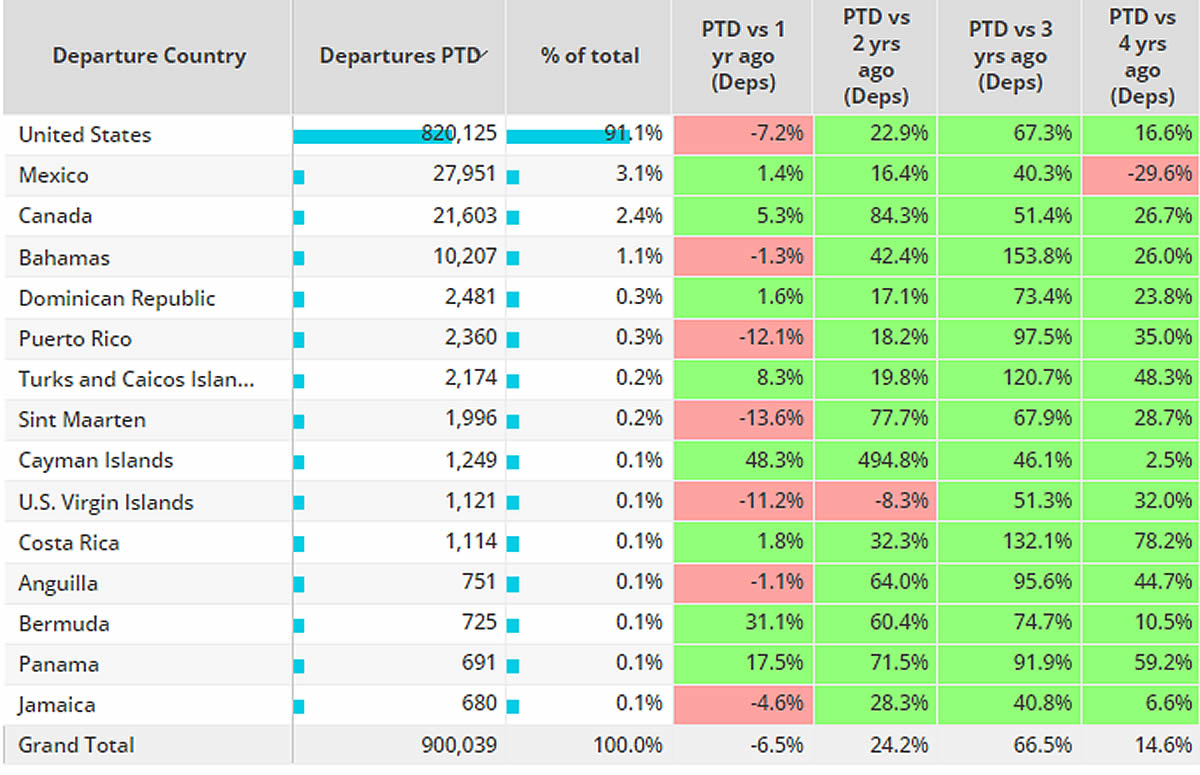

North America

In Week 17 2023 business jet activity in North America declined 2% compared to Week 16, and was 11% behind the same dates in 2022, the same trend as for the last 4 weeks.

In the United States, Part135 & 91K bizjet sectors in Week 17 fell 2% compared to Week 16, 12% below the same dates in 2022. In Week 17 Branded Charter and Fractional bizjet sectors fell 11% compared to the same dates in 2022.

There were 820,000 departures from United States airports in the first four months of 2023, 7% fewer than 2022, although 17% ahead of 2019. Activity this year in Mexico is still substantially down on pre-pandemic levels, sectors down 30%. Activity in Canada is 27% ahead of 2019, edging 5% out on last year.

Chart 2: North America Business Jet markets, 1st January – 30th April 2023 compared to previous years.

So far this year the Bombardier Challenger 300/350 is the busiest aircraft type. There were 66,000 departures between 1st January and April 30th, 2% fewer than 2022, 17% more than 2019. The Embraer Phenom 300 and Cessna Citation Latitude are the only aircraft types in the top 5 to see activity ahead of last year, sectors up 3% and 6% retrospectively this year.

With 134,000 business jet sectors so far this year, Florida is the busiest US State despite departures being 11% below last year. Texas is the second busiest US State this year, although 50,000 fewer departures than Florida, activity down 6% compared to last year.

Year to date business jet departures from Teterboro airport are down 2% compared to 2022, 2% down compared to 2019. Corporate flight departments are flying 5% more flights compared to last year out of Teterboro, although still 17% fewer than in 2019.

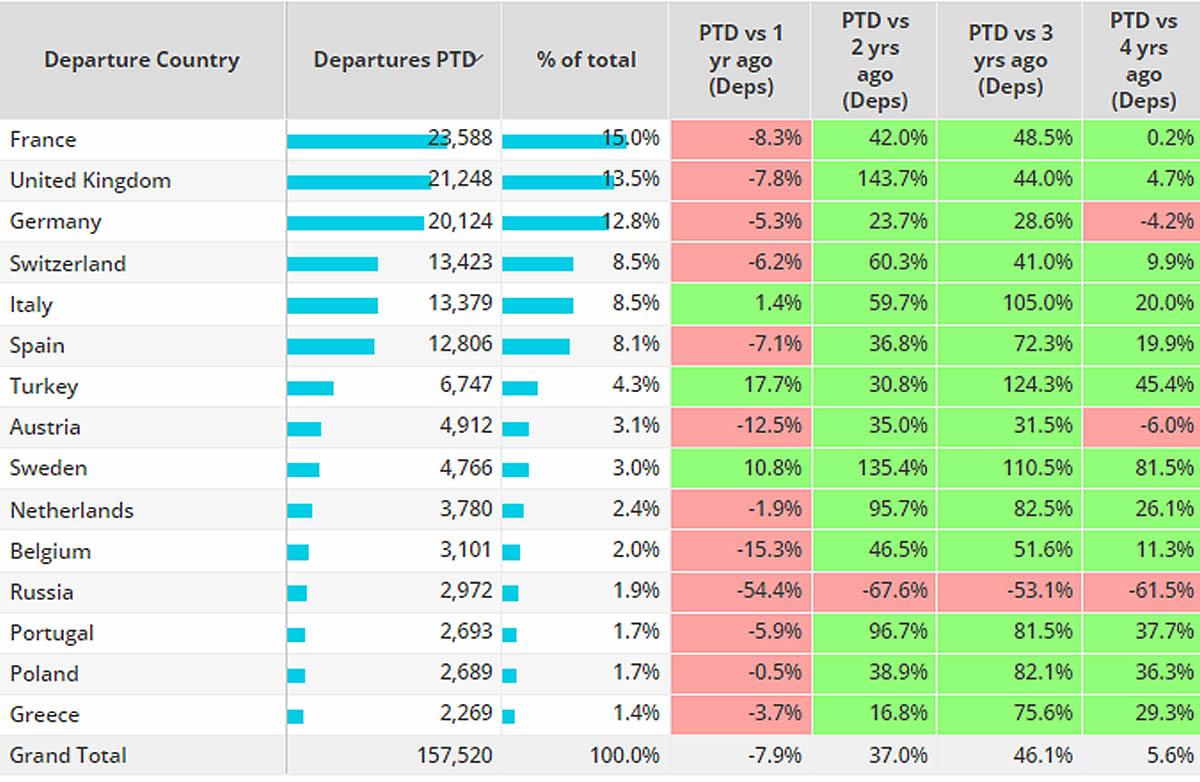

Europe

In Week 17 business jet activity in Europe grew 1% compared to Week 16, 11% below the same dates in 2022. In the last four weeks the trend is 8% below the same dates in 2022. So far this year European business jet traffic is 8% behind comparable 2022, 6% ahead of 2019.

Year-to-date France is the busiest bizjet market in Europe this year, activity out of France is 8% below comparable 2022, now on-par with 2019. The United Kingdom and Germany complete the top 3 markets YTD, both markets are down compared to last year. YTD activity in Germany slipping 4% behind 2019.

Chart 3: Top European Business Jet Markets, January 1st – April 30th 2023 compared to previous years.

Year-to-date, 4 out of the top 5 busiest bizjet airports in Europe have seen activity drop behind last year’s volumes. Zurich is the only top 5 airport to see growth compared to 2022, London Luton seeing 3% declines compared to 2019.

In April European bizjet activity fell 8% behind April 2022, although 7% ahead of 2019. France, the busiest market, saw activity dip 1% behind 2019, activity in 3rd ranked Germany dropped 3% compared to 2019. Spain was the only top market in April to see activity grow compared to last year, departures up 1% compared to 2022, 32% ahead of 2019.

Rest of World

In Week 17 activity in Africa was 34% ahead of the same dates in 2022, Asia up 1%, South America down 4%, Middle East down 9%.

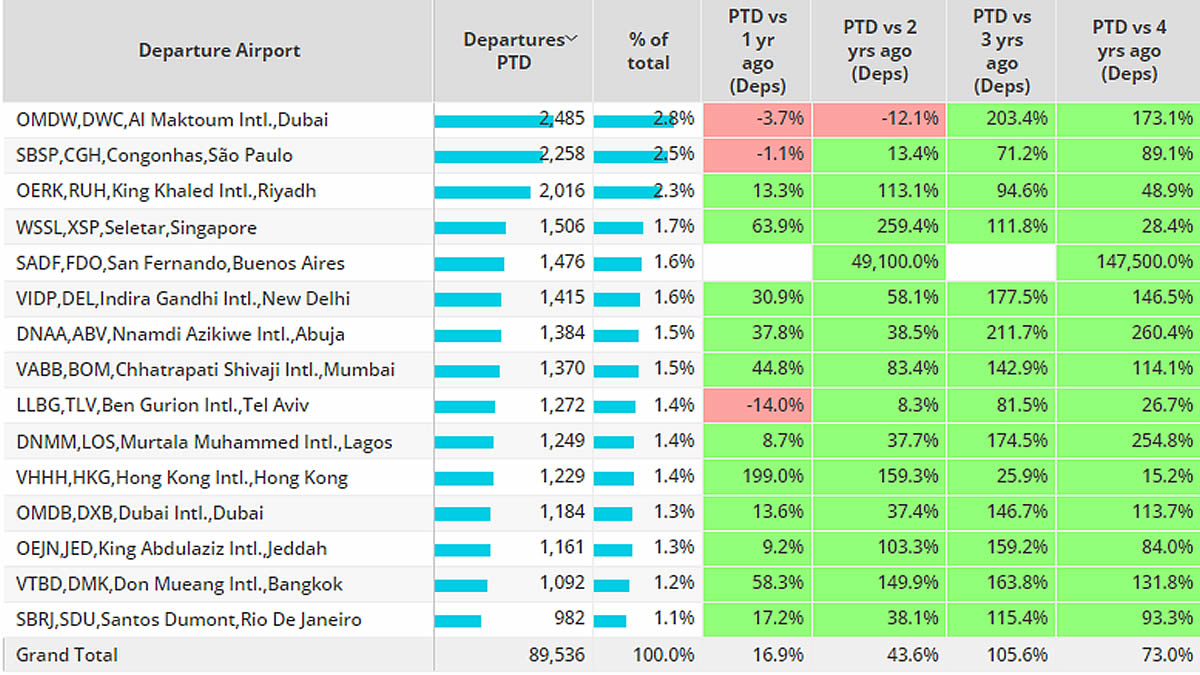

Excluding North America and Europe, year-to-date business jet activity was 17% ahead of last year, 73% ahead of 2019. Brazil, the busiest ROW market so far this year has seen activity grow 12% compared to last year, triple digit growth compared to 2019. Elsewhere activity in the United Arab Emirates is up 6% compared to 2022, 97% ahead of 2019. So far this year departures from China are up 45%, although down 6% compared to 2019.

The Bombardier Challenger 600 series is the busiest aircraft type YTD, departures up 28% compared to 2022, up 59% compared to 2019. The Embraer legacy 600/650 platform is the only aircraft in the top 10 to see activity levels drop compared to last year, departures down 1% compared to 2022.

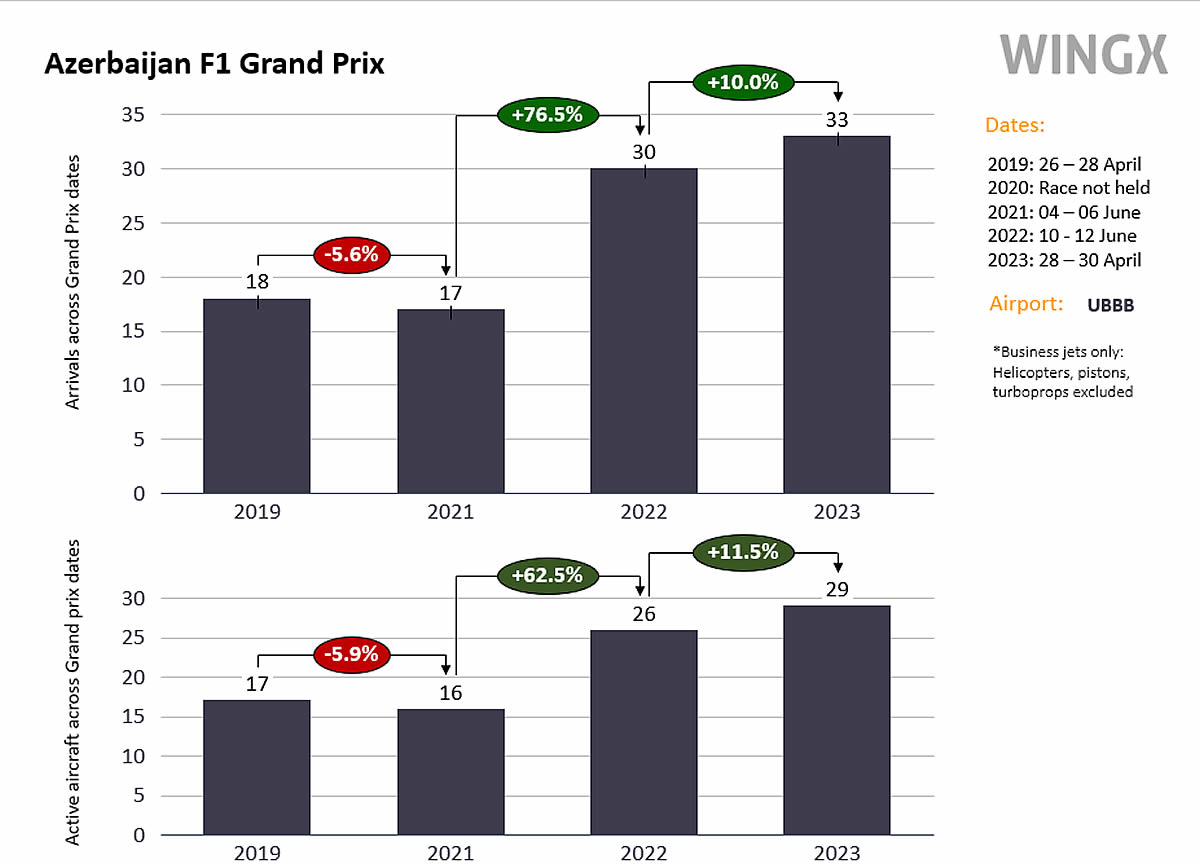

In Azerbaijan the Formula One Grand Prix last weekend (28th – 30th April) contributed to business jet arrivals into Heydar Aliyev International Airport (UBBB). During the Grand Prix weekend (April 28th – 30th) there were 33 business jet arrivals, more than double the previous Friday-Sunday period (April 21st -23rd). This year’s Grand Prix attracted 10% more bizjet arrivals than the 2022 edition of the race, 83% more than the 2019 edition.

Chart 4: Azerbaijan 2023 Grand Prix.

Chart 5: Top Rest of World airports, bizjets, 1st January – 30th April 2023 vs previous years.