WINGX�s weekly Business Aviation Bulletin.

Summary

In terms of aggregate flight activity, the business jet market has moved well off the peaks we saw early last year, with the charter market particularly choppy. The gap between this year and last, week-to-week, has been diminishing since March, suggesting we may be moving past the biggest corrections, with a new level of flight activity normalising as we head into the summer.

Global

In Week 19 (8th to 14th May) global business jet departures fell 2% compared to Week 18, and activity was down 8% compared to the same dates in 2022. For the month so far, including turboprops, flight activity is down 5% on May last year, still 13% ahead of May 2019. Comparably, scheduled airline activity is 10% ahead of last year, still 14% behind 2019. The recovery is much stronger for the top 5 global airlines (Southwest Airlines, American Airlines, Delta Airlines, Ryanair, United Airlines); in the first two weeks of May these operators’ activity is 11% ahead of last year, 7% ahead of 2019.

Chart 1: Global fixed wing flights, May 1st – May 14th 2023 compared to previous years. (Note business aviation includes turboprops)

North America

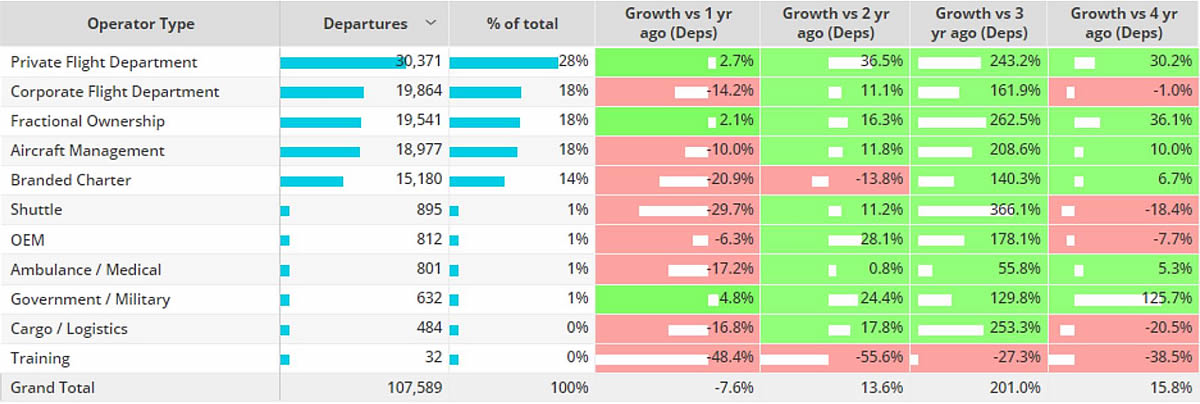

Week 19 business jet departures in North America dropped 5% from Week 18, 10% fewer than the same dates in 2022. In the last four weeks bizjet activity in the region has dropped 9% behind last year. The trend compared to 2019 is still strong, with bizjet activity 16% ahead of May 2019 so far this month. Charter and Corporate Flight departments have the weakest trends, respectively 14% and 21% below 2022 trends this month, with Corporate departments flying a fraction below May 2019.

Across North America Wheels Up (Wheels Up, Wheels Up LLC, Wheels Up Partners LLC, Wheels Up Private Jets, Delta Private Jets, Gama Aviation, Travel Management Company, Mountain Air Charter LLC, Air Partners Corp, Alante Air Charter) departures are down 23% compared to the first two weeks of May 2022, down 27% compared to 2019. Year to date (1st January � 14th May) departure trends are the same, -23% compared to 2022, -27% compared to 2019. DeKalb Peachtree is the busiest departure airport so far in May for Wheels Up, followed by Teterboro. Year to date Palm Beach is the busiest departure airport, followed by DeKalb Peachtree.

Chart 2: North American business jet operator types 1st � 14th May 2023, compared to previous years.

So far this month Trans-Atlantic Business Jet activity (North America � Europe) is 2% ahead of last year, 18% ahead of 2019. Teterboro is the busiest departure airport for Trans-Atlantic bizjet activity, departures down 1% compared to last year, although 7% ahead of 2019. The majority of traffic this month is between the United States and the United Kingdom, flights are down 20% compared to May last year, although 15% ahead of 2019. Contrast US to France flights which are up 39% compared to last year.

Europe

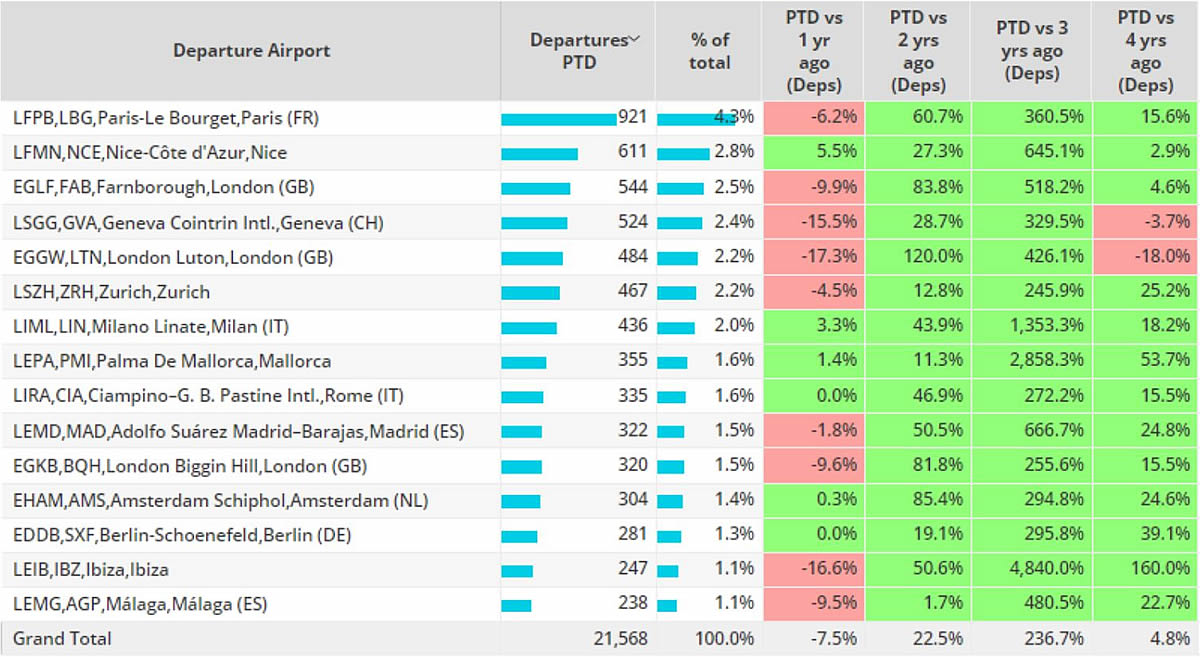

In Week19 business jet activity rose 10% compared to the previous week this year, 6% below the same dates in 2022, and in the last four weeks activity is 7% behind the same dates in 2022.France is the busiest European market in the first 2 weeks of May, bizjet flights down 5% compared to last year, still 7% ahead of 2019. The United Kingdom and Germany are seeing double digit declines compared to last year, -10% and -14% respectively. Italy and Russia are the only countries in the top 15 to see demand fall behind May 2019, flights from Italy down less than 1%, Russia down 64%. Russian business jet activity has eroded even further than last year, departures down 3% compared to the first two weeks of May last year.

Chart 3: Top European business jet airports, 1st � 14th May 2023 compared to previous years.

Just over 5,000 flights have been operated on Light Jets segment in the first two weeks of May, making the segment the busiest, although flights are down 9% compared to last May, 8% ahead of 2019. Bizliner activity is still well behind 2019 activity levels, flights 52% behind comparable May 2019.

Rest of World

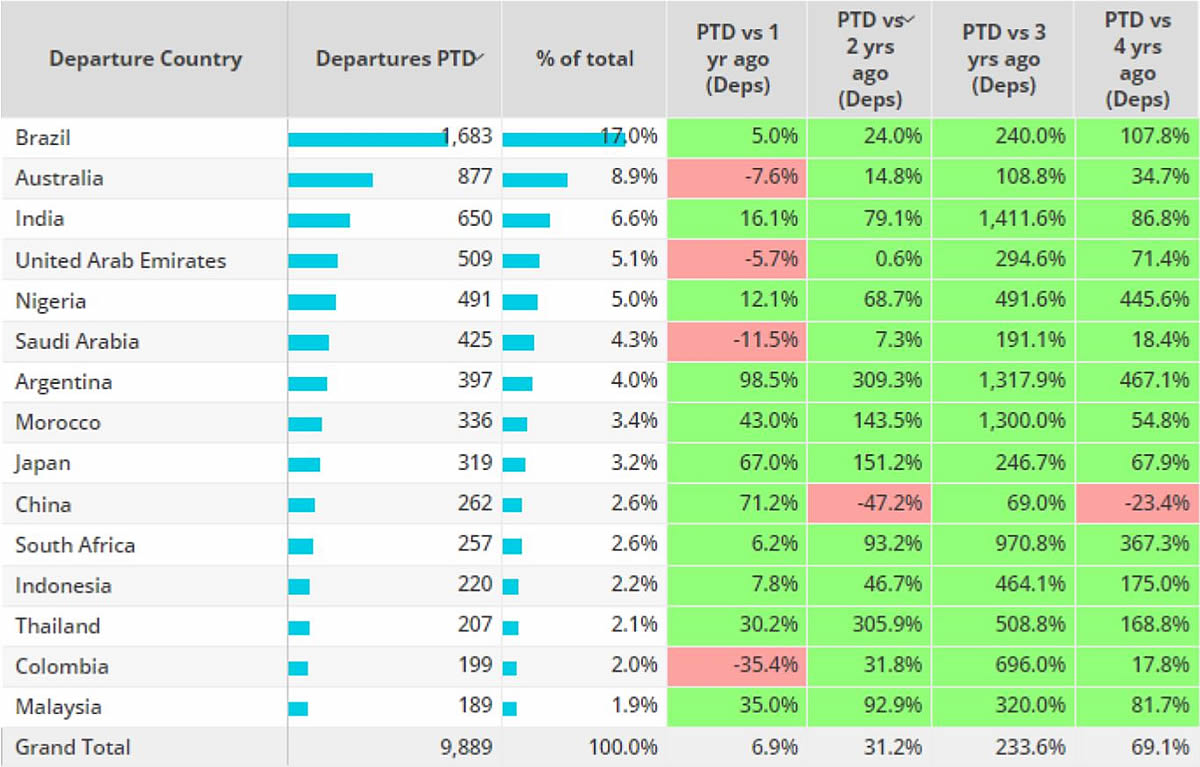

So far this month bizjet activity outside of North America and Europe is 7% ahead of the opening two weeks of May 2022. Brazil, the busiest market is seeing 5% growth compared to last year, whereas bizjet activity in Australia has fallen 8% behind May 2022. Leading Middle East markets United Arab Emirates and Saudi Arabia are behind 6% and 12% retrospectively. Activity in China is trailing 2019 by 23%, although rebounding 71% ahead of last year.

Chart 4: Rest of World Business jet countries, 1st � 14th May 2023 compared to previous years.