WINGX�s weekly Business Aviation Bulletin.

Summary

The steep declines in activity compared to 2022 have softened in late May, steadying the gains compared to pre-pandemic 2019. Europe appears to be the weak spot, with activity in Germany almost 20% down on last year, and busiest market France seeing only 2.5% increase on 2019, 2% decline compared to four years ago for domestic flights.

Global

There have been almost two million business jet and turboprop flights operated between January 1st and 21st May 2023, 4% fewer than during the same period 2022, 14% ahead of comparable 2019. So far this year, scheduled airline departures are 19% ahead of comparable last year, although still 14% below 2019. Focussing on the top 5 global airlines (Southwest Airlines, American Airlines, Delta Air Lines, Ryanair, United Airlines), activity is 14% ahead of comparable last year, 5% ahead of 2019.

Chart 1: Global fixed wing flights, January 1st – May 21st 2023 compared to previous years. (Note business aviation includes turboprops)�

North America

In Week 20, ending 21st May, business jet activity in North America grew 5% compared to the previous week, 5% fewer than in the same dates in 2022. In the last four weeks the trend is 8% down compared to the same dates last year. Part-135 and 91K certified business jet flights were up 5% compared to week 19 and dipped 6% below the same dates in 2022. So far in May 2023, sectors in North America are 7% down on comparable May 2022, 16% ahead of May 2019. Business jet sectors between 90 minutes and 3 hours have seen the largest increase since pre-pandemic May 2019, sectors up 28%, although down 9% compared to May last year.

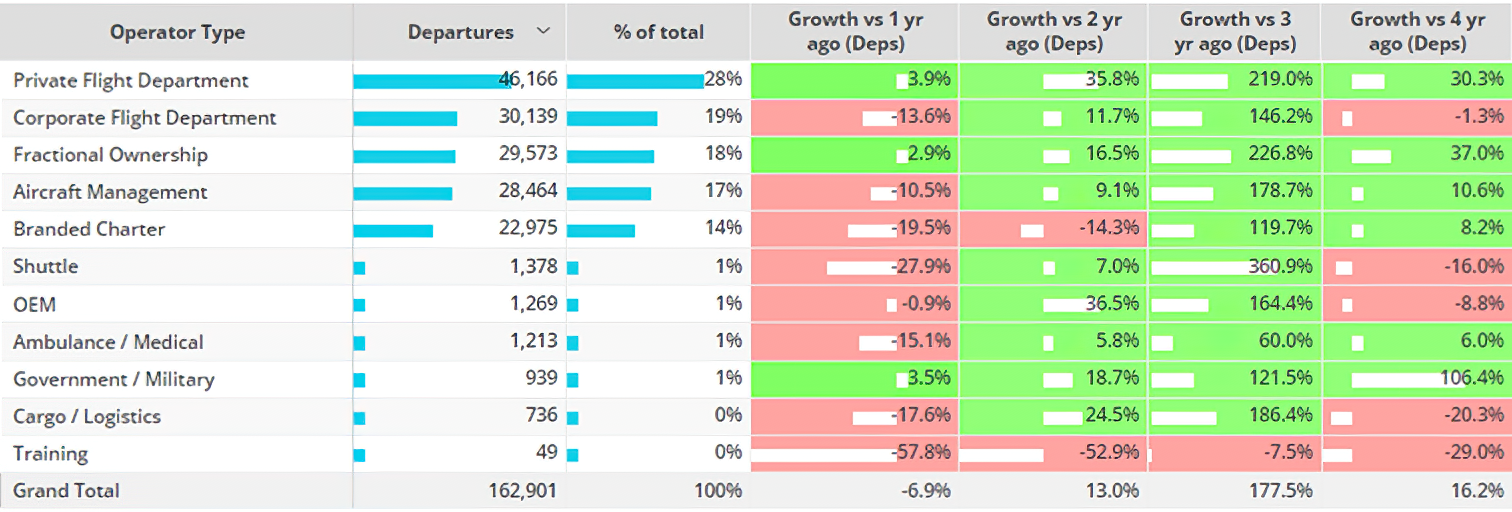

Private flight departments and Fractional Ownership operators are busier this year than last year and more than 30% up on 2019. Branded charter operations have fallen 20% in May 2023 versus May 2022, but still up 8% compared to May 2019. Amongst the busiest US airports for business jet departures, Teterboro is seeing 3% fewer departures this May than May 2022, just 2% ahead of May 2019. Business jet departures from Palm Beach are down by 12% compared to last year, although 57% ahead of May 2019.

Chart 2: North American business jet operator types 1st � 21st May 2023 vs previous years.

Europe

In Week 20, ending May 21st, European business jet sectors grew 3% compared to the previous week, 12% below the same dates in 2022. In the last four weeks the trend is 10% below the same dates in 2022. Business jet departures in Europe this month are 9% below May last year, although 6% ahead of 2019. 63% of business jet flights this month have been under 90 minutes in length, flights of these duration are down 11% compared to last year, 6% ahead of 2019. Medium haul (3-6hours) down 15% compared to 2019, 6% behind last year.

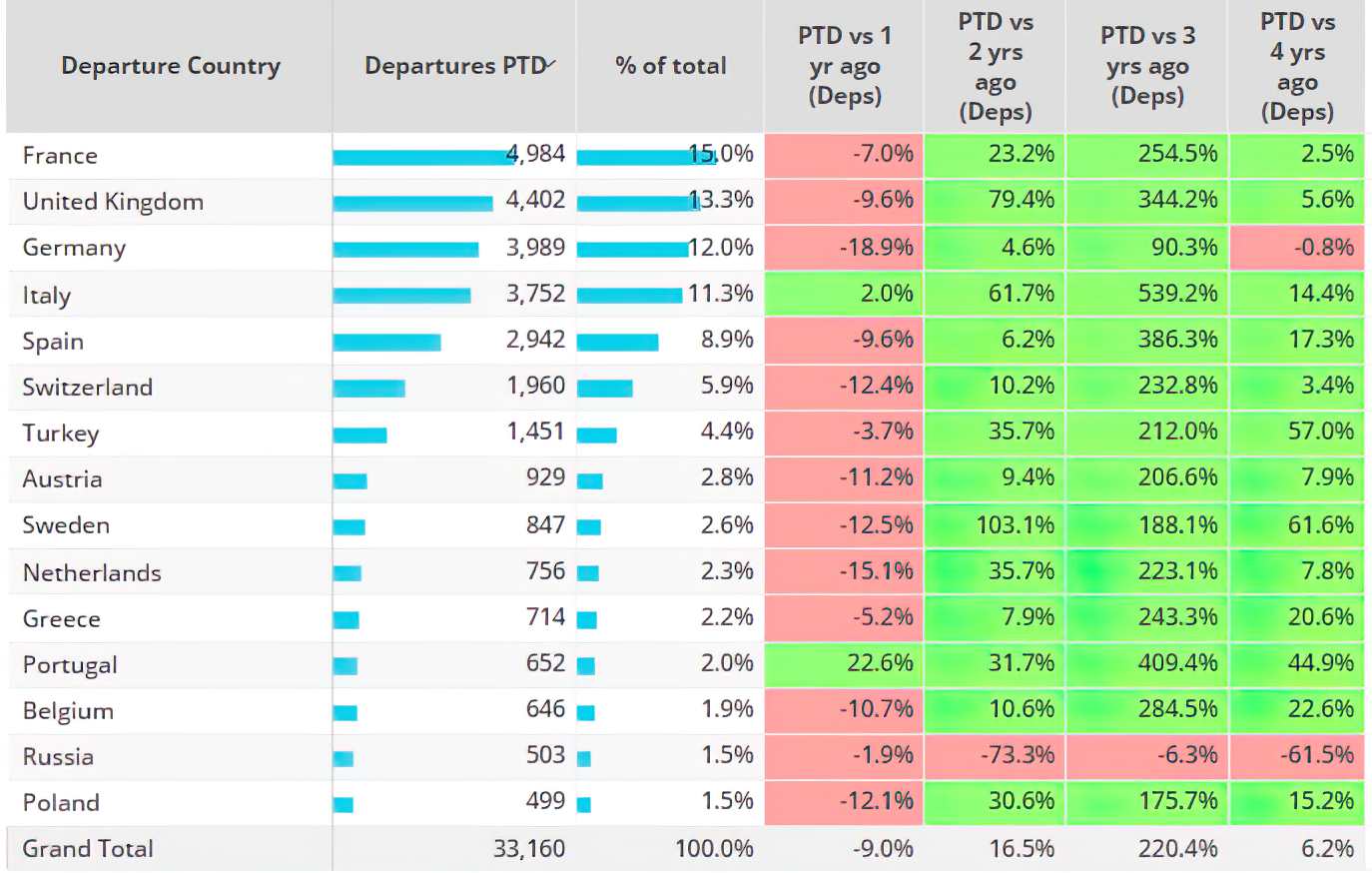

France is the busiest bizjet market in Europe this month, accounting for 15% of the region’s business jet departures. Departures from France are down 7% compared to last May, 3% ahead of May 2019. The United Kingdom is the second busiest market, departures are down 10% compared May 2022, 6% ahead of May 2019. Germany�s business jet activity is stalling, 19% fewer departures than May last year, 1% below 2019.

Chart 3: Top European business jet markets, 1st � 21st May 2023 vs previous years.

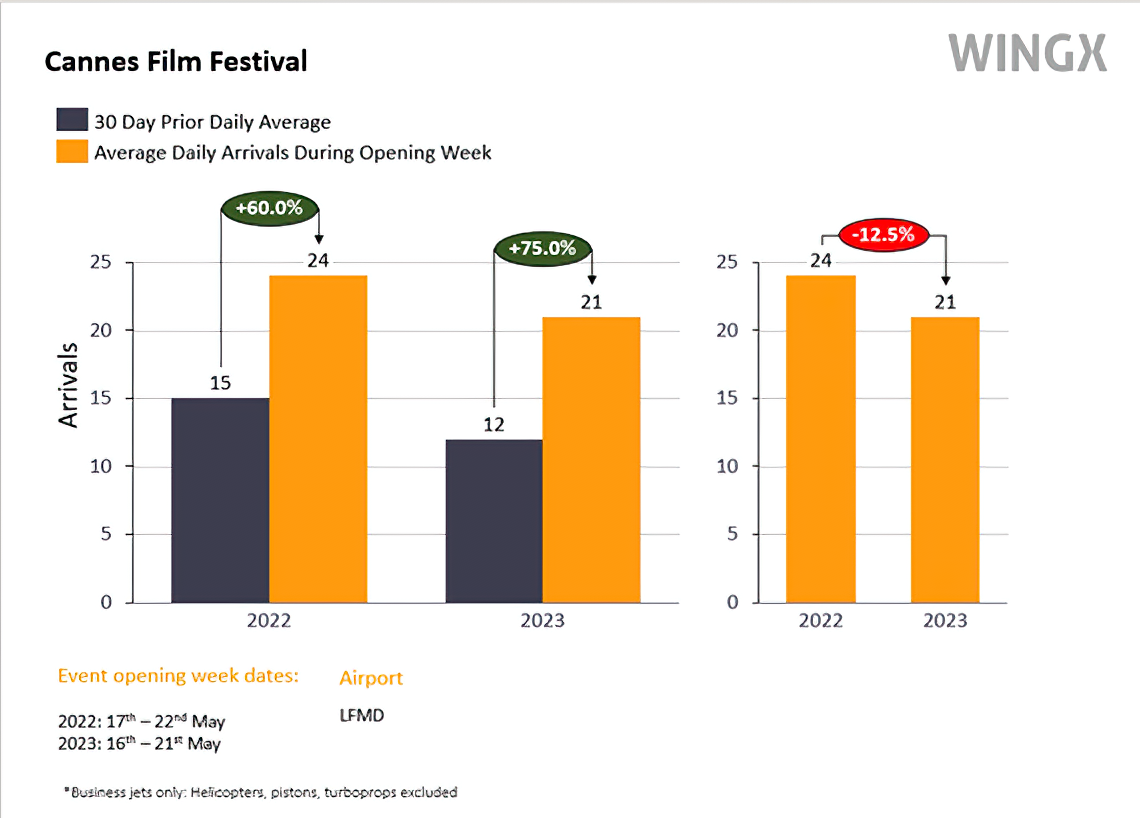

So far this month there have been almost 1,800 domestic business jet flights in France, 2% fewer than comparable 2019, contrast domestic scheduled airline activity which is down 30% compared to 2019. Paris to Nice is the busiest domestic bizjet city flow, departures 25% ahead of 2019, contrast scheduled airline flights between the two cities, departures are down 3% vs 2019. Elsewhere in France, the first week (16th � 21st May) of Festival de Cannes International Film Festival had a positive impact on business jet arrivals into LFMD (Cannes Mandelieu Airport). During the opening week, average daily bizjet arrivals into LFMD were 75% higher than the average daily arrivals for the previous 30 days, however, the average daily arrivals during the event dropped 13% compared to the first week of the 2022 edition of the event.

Chart 4: Business jet arrivals to airports near Festival de Cannes International Film Festival

Rest of World

Outside of North America and Europe, business jet departures this month are 8% ahead of last year, although activity was down 10% in the Middle East in Week 20 2023 compared to same dates in 2022. So far this month, business jet flights from India and Nigeria are up 15% and 12% respectively, United Arab Emirates and Saudi Arabia seeing demand fall 10% and 6% respectively, compared to last year. Business jet flights from China have rebounded 77% compared to May 2022, but still 16% below comparable 2019. Ultra-long-range jets are the busiest jet segment operating outside North America and Europe, their flights 22% ahead of last year, 49% up vs May 2019.