WINGX�s weekly Business Aviation Bulletin.

Summary

During this month we have the largest ever number of commercial airline flights, but for business aviation aircraft, activity so far in July 2023 is behind comparable July in 2021 and 2022. The post-pandemic surge in bizjet demand has fallen well behind in Europe, is still holding up quite well in North America, and continues to climb in other parts of the world, notably in Turkey, Qatar and India.

Global

Global bizjet and turboprop departures are down 4% compared to comparable July last year, although 13% ahead of 2019. Focussing on just business jets, just under 2 million flights have been flown so far this year, 5% behind last year, although 19% ahead of 2019. So far this month departures are 5% behind last year, 17% ahead of 2019. In Week 29 (ending 23rd July), global business jet activity was on par with the previous week, 4% behind the same dates in 2022. Scheduled airline departures are 9% ahead of last year, although still 12% behind pre-pandemic July 2019. The trend for the top 5 business airlines (Southwest, American, Delta, Ryanair & United Airlines) is slightly ahead of the global airline trend, departures so far this month are 10% ahead of July last year, 8% ahead of July 4 years ago.

Chart 1: Global fixed wing flights by sector, July 2023 compared to previous years. (Note business aviation includes turboprops)

North America

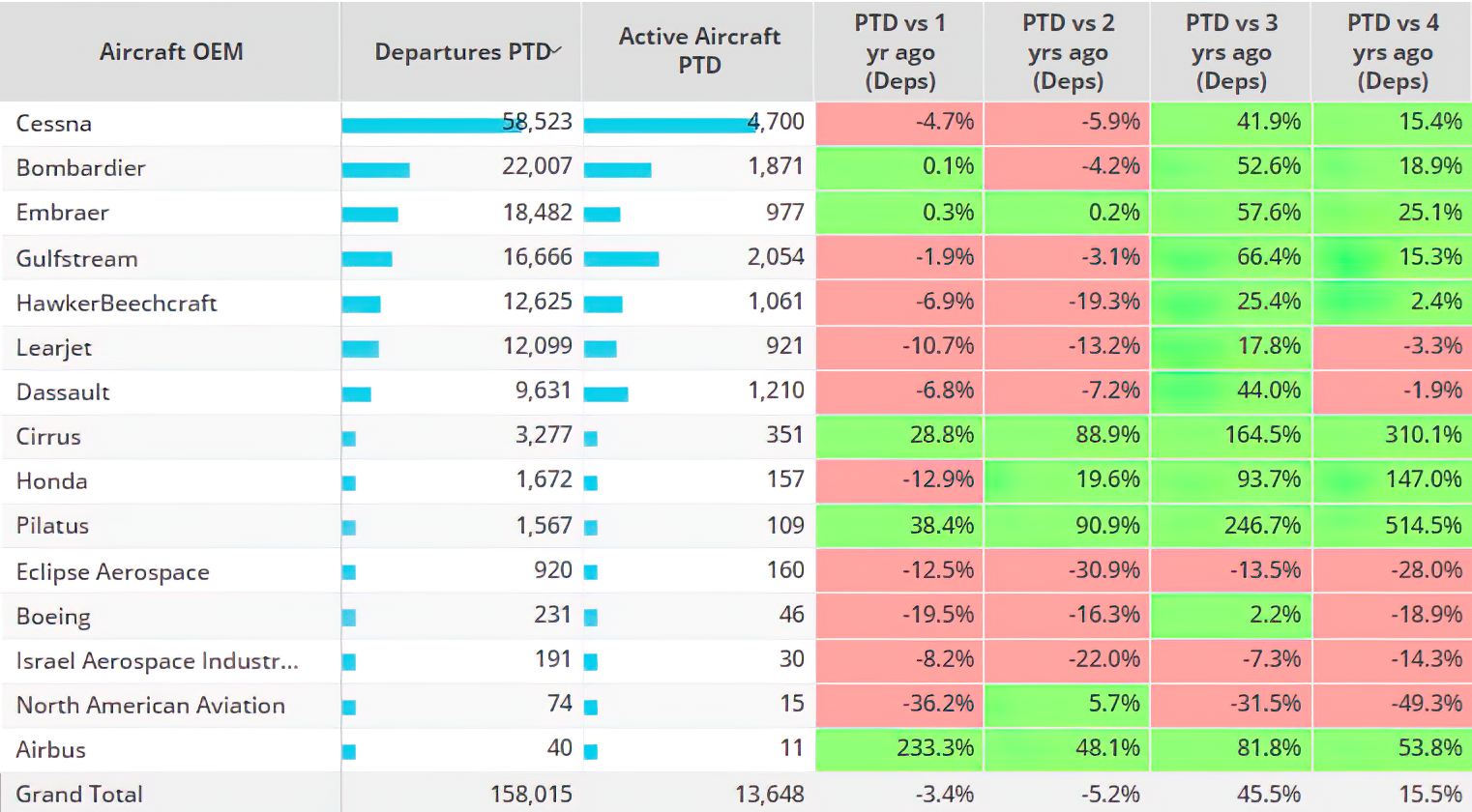

In Week 29 bizjet activity was 1% ahead of Week 28, 3% behind the same dates in 2022. There have been 20,596 bizjet sectors flown in Week 29, comparing to the last 52-week high of 30,512. In the last 4 weeks the regional trend is 2% down compared to last year. Year-to-date business jet activity across the North America region is 6% below last year, although 18% ahead of 2019. Focussing on July, activity this month is 3% behind last year, 16% ahead of 2019. Intra-regional flights are down 4% compared to last year, international flights down only 1% YOY.

The busiest OEM fleet this month is Cessna, activity down 5% vs 2022, up 15% vs 2019. Bombardier and Embraer fleets are busier this year than last year, whereas Gulfstream and Dassault are flying less. Compared to July 2019, Embraer executive jet activity is up 25%. Honda Jets are flying 13% less than July 2022, up 147% compared to July 2019. Pilatus PC-24 traffic is up 38% compared to July 2022.

Chart 2: Business Jet OEMs, North America, July 2023 compared to previous years.

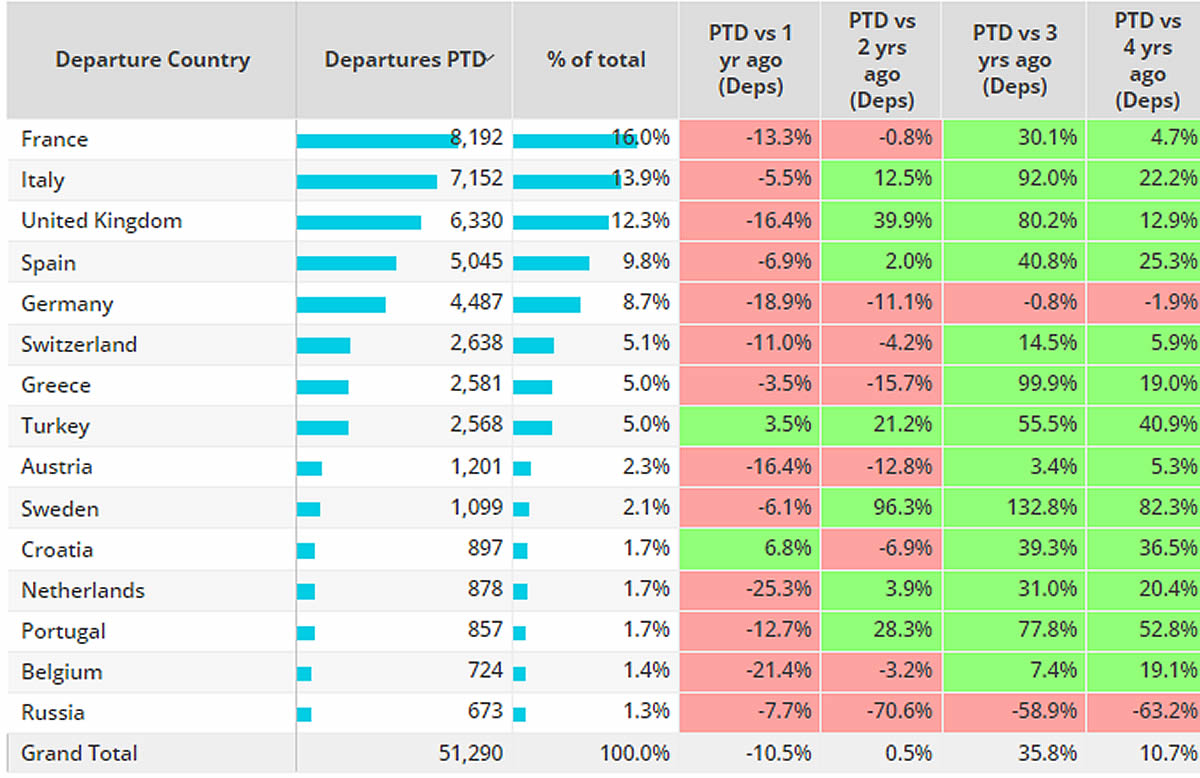

Europe

Week 29 European bizjet activity fell 4% compared to the previous week, 13% behind the same dates in 2022. In the last 4 weeks activity has fallen 10% compared to last year. The busiest day for business jet activity since January 2021 was the 1st July 2021, 2,900 sectors were flown.

France is the top bizjet market so far this month, activity down 13% compared to July last year, 5% ahead of 2019. United Kingdom, Germany and Switzerland are seeing double digit declines compared to July last year, Turkey and Croatia are ahead of last year. All major bizjet hotspots are seeing declines compared to last year, Farnborough the exception, departures 14% ahead of last year, although 3% behind 2019.�

Chart 3: European Business Jet Country Trends, July 2023 compared to previous years.

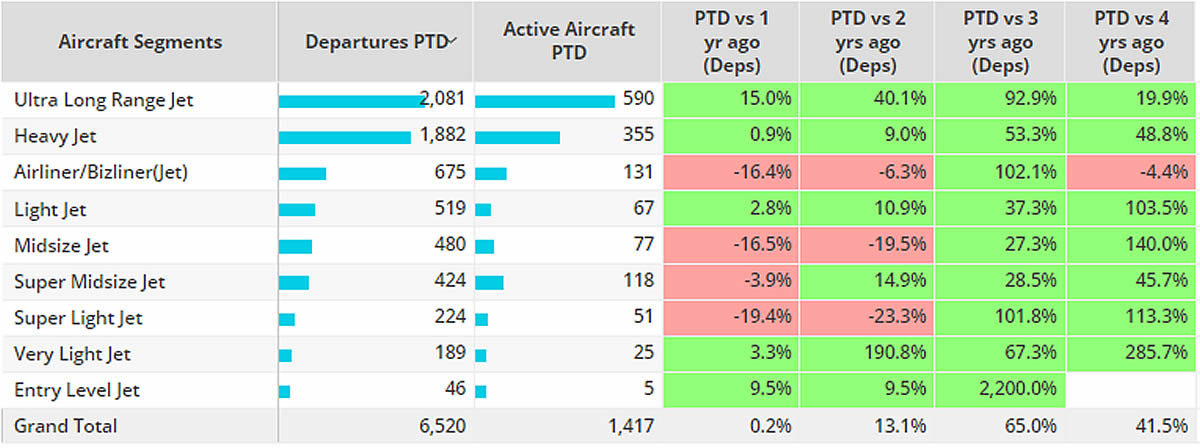

Asia

So far this month business jet activity across Asia is on par with July last year, 42% ahead of 2019. Departures from China are up 22% compared to last year, 4% below pre-pandemic July 2019. Elsewhere Japan up 46% compared to last year, Singapore down 11%. Bizliners are the only aircraft segment in the region still below comparable 2019 activity levels, departures down 4% compared to July 2019. Midsize and Superlight jets are both seeing double digit declines compared to last July, although both well ahead of 2019.

Chart 4: Asia Business Jet Segments, July 2023 compared to previous years.

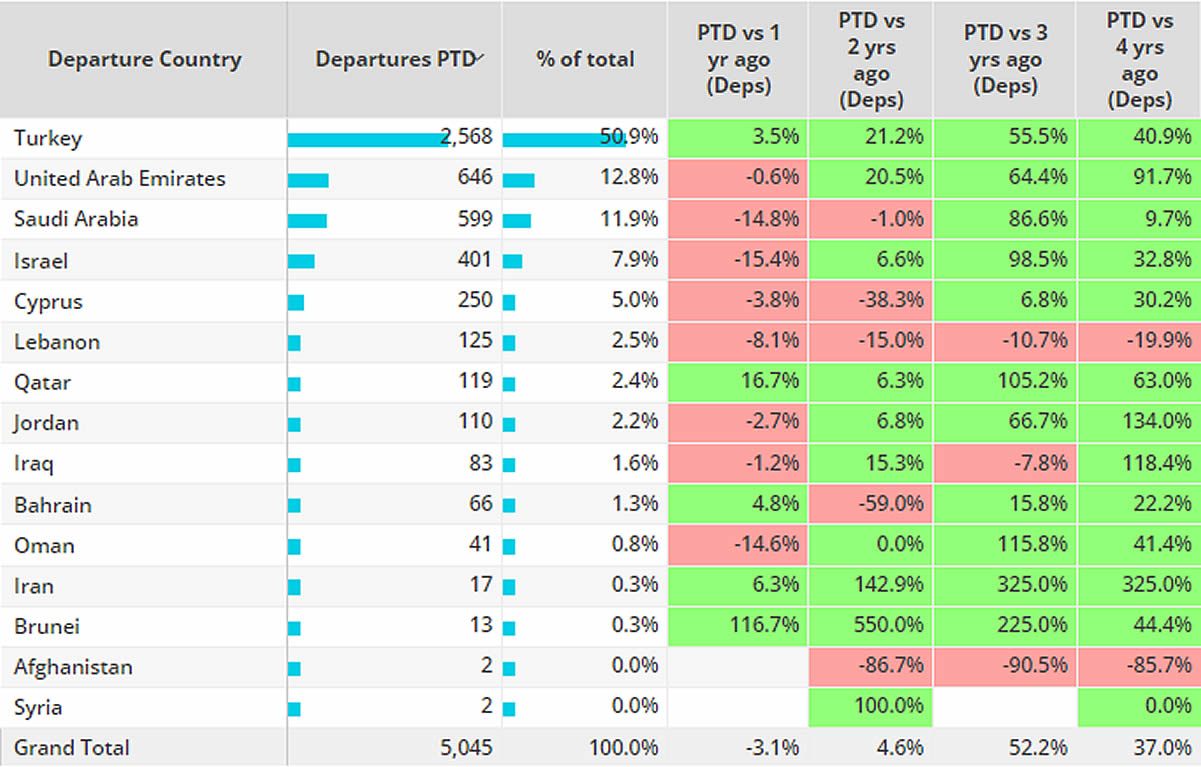

Middle East

Regionally business jet departures are 3% below July last year, 37% ahead of 2019. Turkey tops the Middle East market this month, business jet departure 4% ahead of last year, 41% ahead of July 4 years ago. Elsewhere demand is mixed, Saudi Arabia and Israel seeing double digit declines compared to last year, business jet departures from Qatar seeing a big increase. Ataturk is the busiest departure point in the region, activity is 3% ahead of July last year, 61% ahead of 2019. Departures from Ben Gurion and King Khaled International are seeing double digit declines compared to last year, Dalaman and Istanbul seeing double digit increases compared to last July.

Chart 5: Top Middle East business jet markets, July 2023 compared to previous years.