Compared to last year, April�s trends are stronger than March, with growth in most of the top markets. UK, France and Germany were exceptions in Europe, with the charter market notably weakening. Bizjet activity in the Middle East saw further erosion, markedly Saudi Arabia. In the US, large business jets are seeing strongest demand. US charter demand is tailing off this month, Part 135 flights down 6% in week 16.

Global

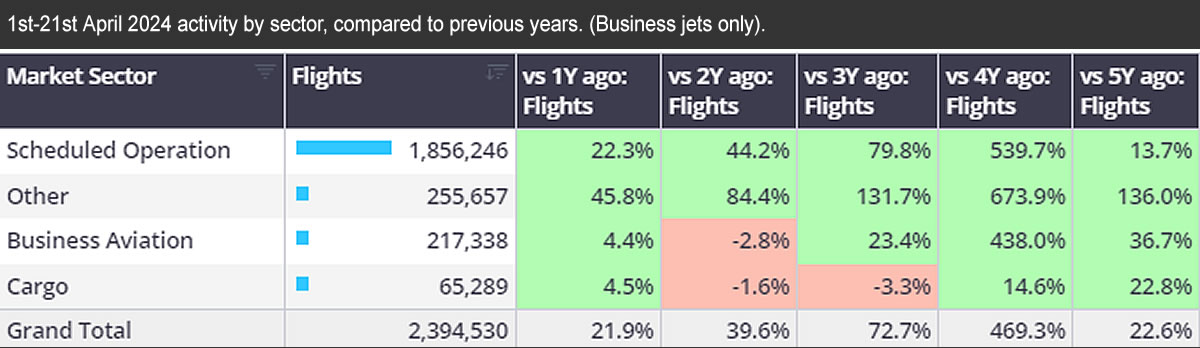

So far this month (1st – 21st April), global bizjet sectors are 4% ahead of comparable April last year, trailing April 2022 by 3%, 37% ahead of April five years ago. For week 16 (15th-21st April), seventy-two thousand global bizjet sectors were up 2% on the previous week, up 4% compared to week 16 in 2023. By comparison, scheduled flight activity so far this month is up by 22% compared to last year, 14% ahead of 2019. Cargo sectors are 5% ahead YOY, 23% ahead of 5 years ago. Year to date, bizjet sectors are 1% ahead of last year, 33% ahead of 2019.

Chart 1: 1st � 21st April 2024 activity by sector, compared to previous years. (Business jets only)

United States

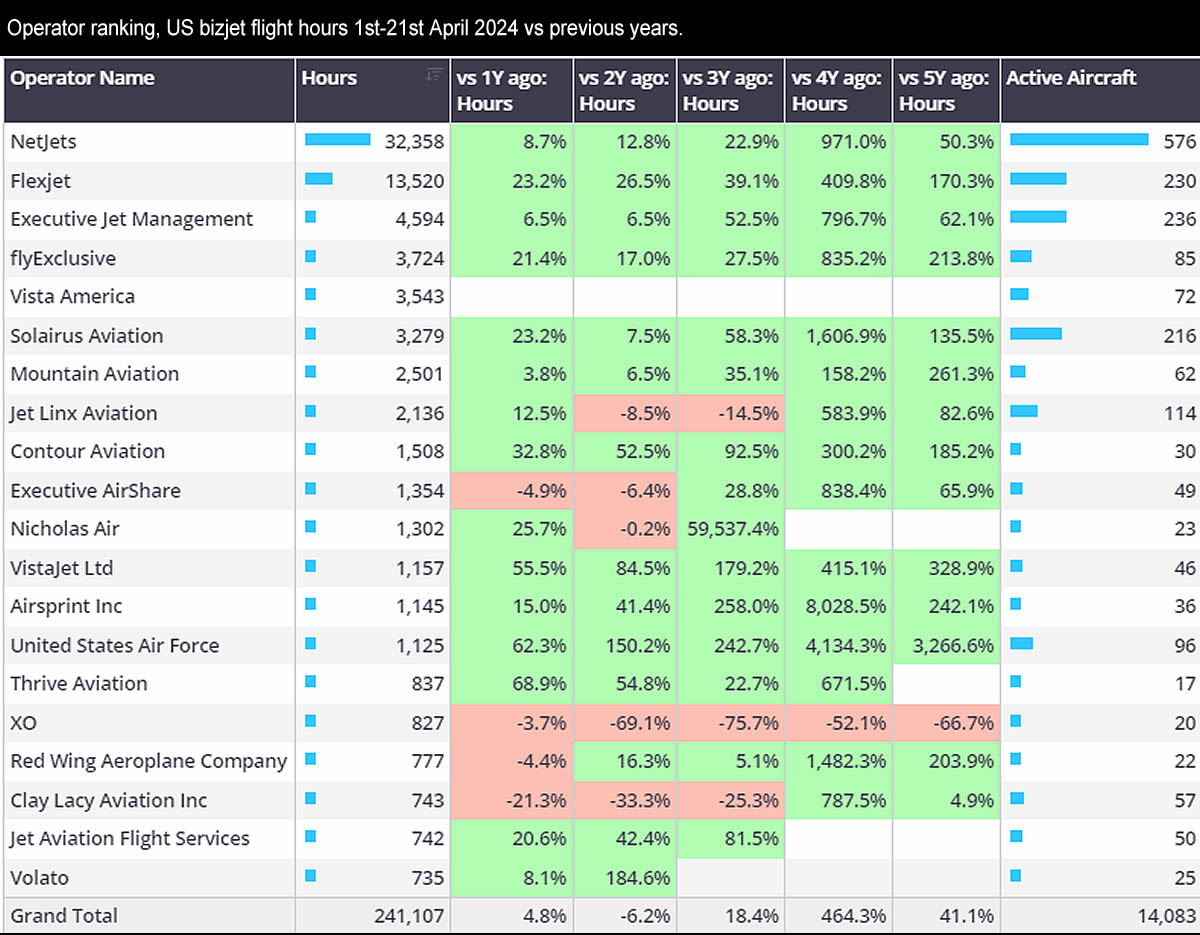

In Week 16, 49,429 business jet sectors were flown in the United States, 5% fewer than the previous week, 2% more than Week 16 in 2023. So far this year (1st January � 21st April 2024), US bizjet activity is 1% ahead of last year, 5% below 2022, 30% ahead of comparable 2019. Several operators are seeing all-time peaks in flight activity this month, notably Netjets, Flexjet, flyExclusive and Jet Aviation. In terms of bizjet flight hours, the NetJets fleet is flying 8% more than last year, 52% ahead of 2019. Flexjet recording triple digit growth in flight hours compared to April 2019, bizjet hours for WheelsUp have fallen 25% year-on-year.

Chart 2: Operator ranking, US bizjet flight hours 1st � 21st April 2024 vs previous years.

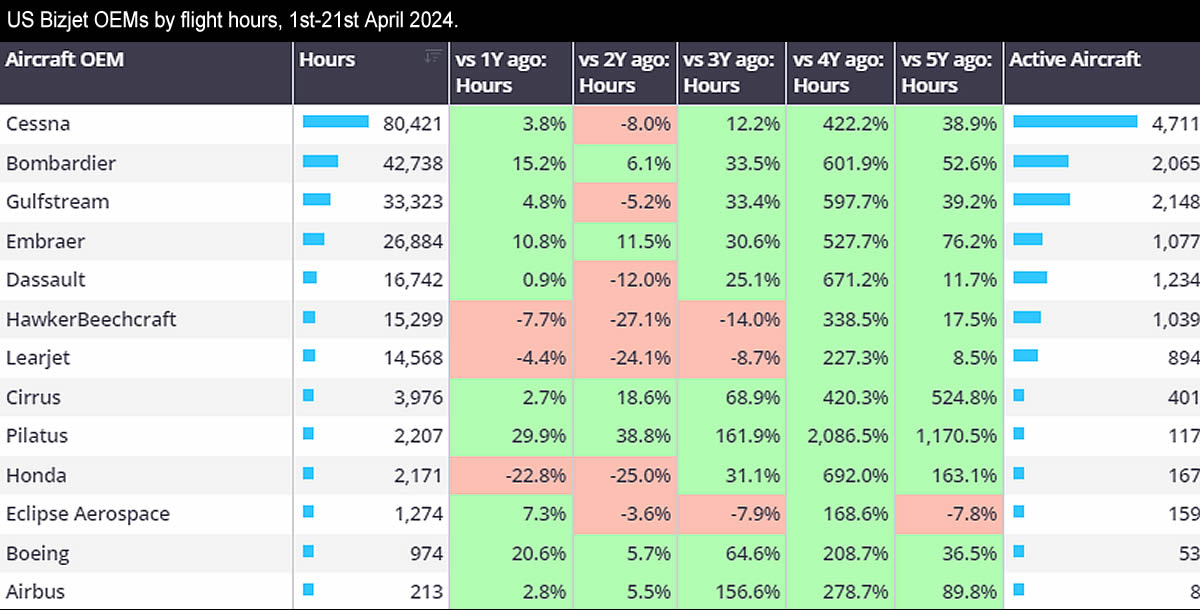

Cessna bizjets are the most active in the US in both flights and hours flown, 4,711 unique aircraft active so far this April, flying 7% fewer sectors than in April 2022. In contrast, Bombardier and Embraer business jets are seeing all time peaks in activity in the US. Embraer bizjets represent 13% of all bizjet departures in the US this month, activity 11% ahead of April last year, 76% ahead of April 2019. New York is the largest metro area departure point for Embraer aircraft this month, Flexjet the largest operator in terms of flights flown.

Chart 3: US Bizjet OEMs by flight hours, 1st � 21st April 2024.

Europe

In Week 16, European business jet activity rose 2% above comparable Week 16 2023, sectors up 11% up on Week 15 this year. So far this year, European business jet activity is 2% down on same period 2023, 2% above 2019 levels.

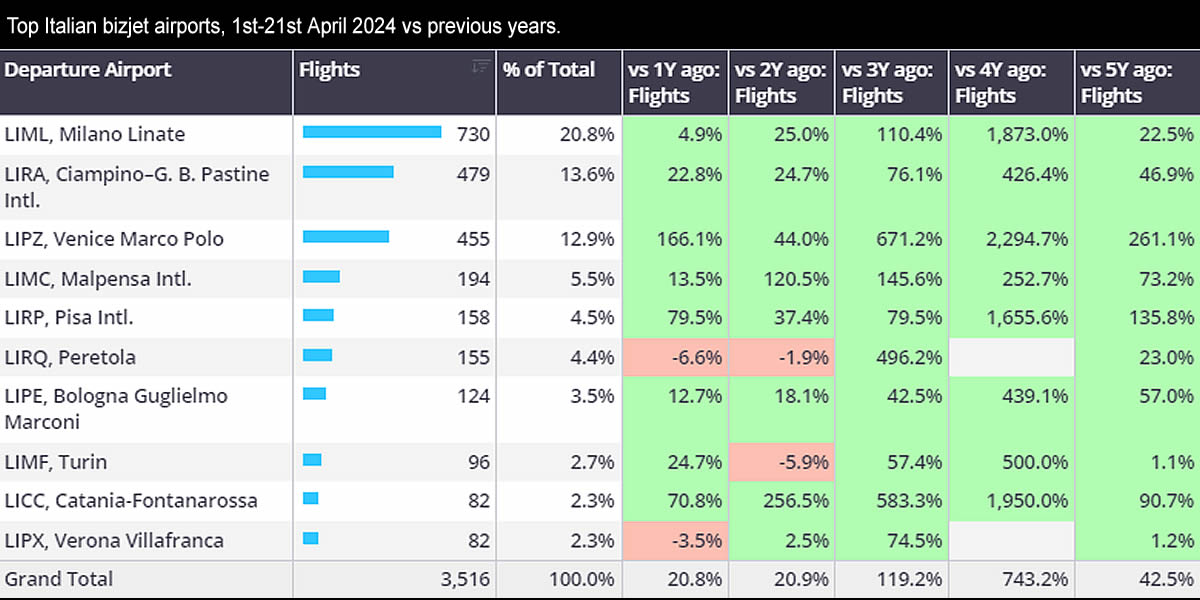

So far in April, European bizjet activity is on par with last year, 7% behind 2022, 4% above 2019. Top market France is 1% behind April 2019, Germany 12% behind April 2019, down 19% in the charter market in Week 16. Contrast Italy and Spain seeing all-time highs so far this month. Italy saw 56% growth in Week 16 compared to Week 15 this year. So far this year, bizjet activity in Italy in Week 1 � 16 has been ahead of the same 16 weeks in 2023. Domestic bizjet flights in Italy jumped from 382 in Week 15 to 590 in Week 16, connections to Germany more than doubled from Week 15 to Week 16, top international connection was to France, 58 more flights in Week 16 compared to Week 15.

So far in April, Le Bouget is the busiest bizjet departure airport in April this month, activity is 3% ahead of last April, 4% ahead of April 2019. Almost a quarter of bizjet departures out of Le Bourget this month are domestic flights, busiest international connection is with Italy, flights up 59% compared to April last year. With 87 flights so far this month, Geneva is the busiest bizjet arrival airport from Le Bourget this month.

Chart 4: Top Italian bizjet airports, 1st � 21st April 2024 vs previous years.

Rest of World

In Week 16, bizjet activity in the Middle East fell 11% behind Week 16 in 2023, although 14% above the previous week. Year to date, Middle East bizjet activity is 8% behind 2023, 46% ahead of 2019.

So far this month bizjet activity in the Middle East is trending 14% behind last year, although 20% ahead of 2019. Activity out of United Arab Emirates, Saudi Arabia and Israel are 5%, 59% and 19% below last April. Busiest international connection out of the UAE is Russia, flights up 49% compared to last year, 28% ahead of April 2019.

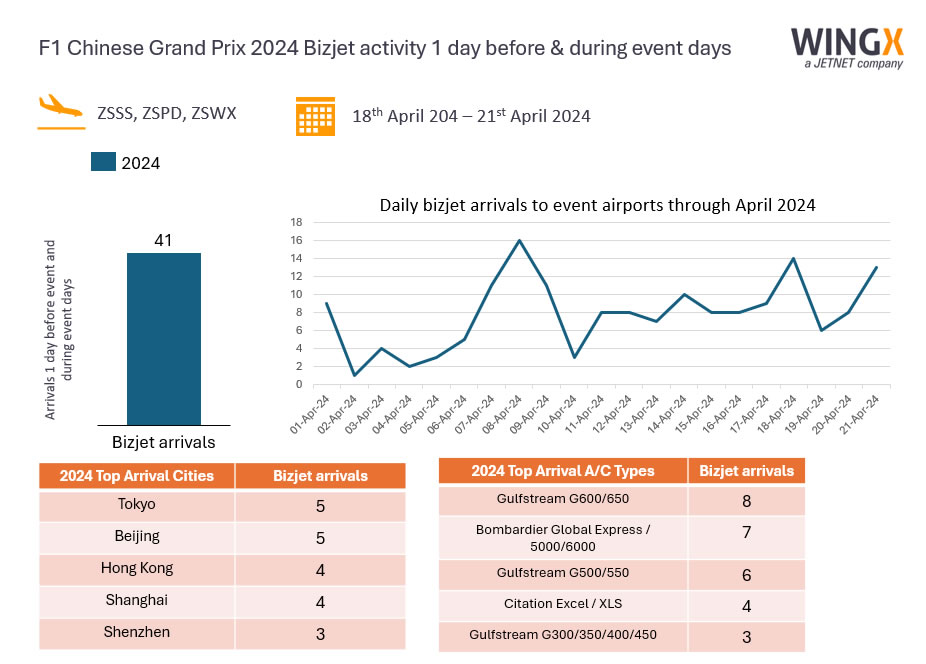

Elsewhere activity out of China is up 94% year-on-year, the hosting of the F1 Grand Prix last weekend (19th � 21st April) had little impact on bizjet arrivals at nearby airports. Just 41 arrivals into ZSSS, ZSPD, ZSWX airports 1 day before and during the Grand Prix weekend, with no notable spike near the event days.

Chart 5: Chinese F1 Grand Prix 2024