Post-Covid demand for business aviation looks strong, notably in the United States where activity is well ahead of 2019. December ended ahead of last year, marking a strong end to the year. Fractional operators have made large gains compared to the last 5 years, contrasting Corporate Flight Department activity. Appetite for business aviation in Europe remains resilient, although small gains compared to pre-pandemic 2019.

Global

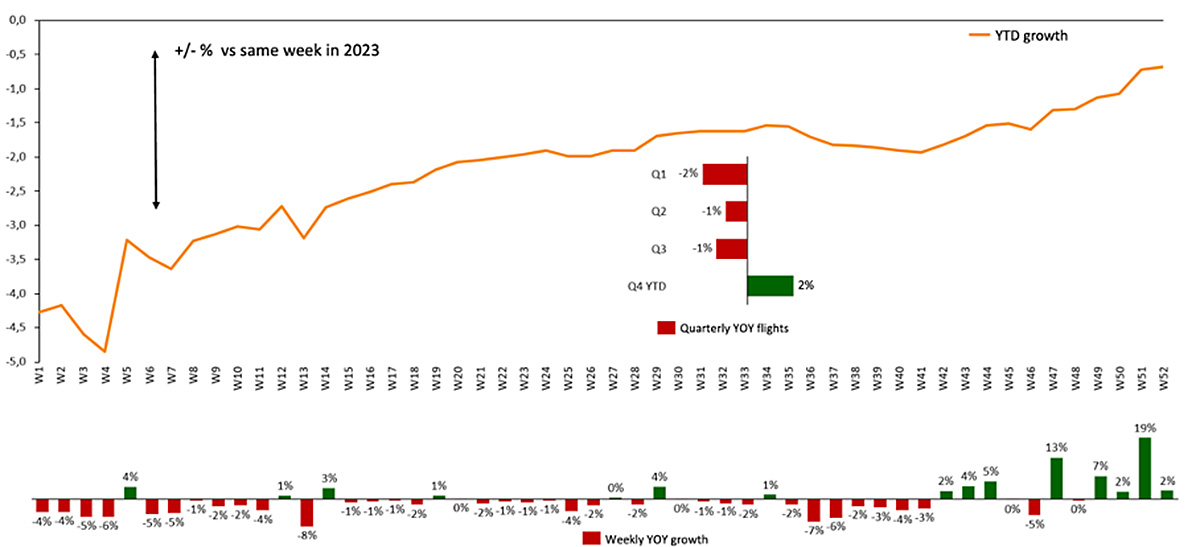

In Week 51, (16th – 22nd December), 74,688 bizjet departures flew globally, 19% ahead of W51 in 2023. Global Part 91K and 135 activity was also 19% ahead of W51 in 2023. In Week 52 (December 23rd � 29th), the final full Monday � Sunday week of 2024, global bizjet sectors grew 2% compared to Week 52 2023, Part 91k and 135 activity 6% ahead of last year.

Globally, 3.6 million bizjet departures were recorded in 2024, a slight decrease, -1%, compared to 2023 and 2022. Activity in 2024 was 59% greater than locked down 2020 and 30% ahead of pre-Covid 2019. Despite the slight year on year decrease, the year ended strong as December activity was 7% ahead of December last year. Fractional operators flew almost 700,000 bizjet sectors in 2024, more than any of the last 5 years, contrast Corporate Flight Departments, flying 11% fewer than last year, 12% fewer than 2019.

Chart 1: Global business jet departures by week, 2024 vs 2023

North America

In Week 51, North America bizjet sectors rose 23% compared to Week 51 in 2023. Part 91k and 135 sectors also rose 23% compared to W51 in 2023. Texas saw large increases in year-on-year activity, up 36% vs W51 in 2023, Part 91k and 135 activity in the State stretched out even further, +42% vs W51 in 2023. In Week 52, bizjet sectors rose 1% compared to last year, Part 91k and 135 sectors rising 6% compared to last year.

Focussing on the United States, bizjet activity in 2024 fell short of 2.5 million departures, on par with 2023 and 3% behind 2022. Post-Covid the business jet market looks robust, activity 27% ahead of 2019. Activity in December was 9% ahead of December last year, marking a strong end to the year in the US. Post US election, the market outlook is optimistic, bizjet departures between November 6th and December 31st were 5% ahead of comparable 2023.

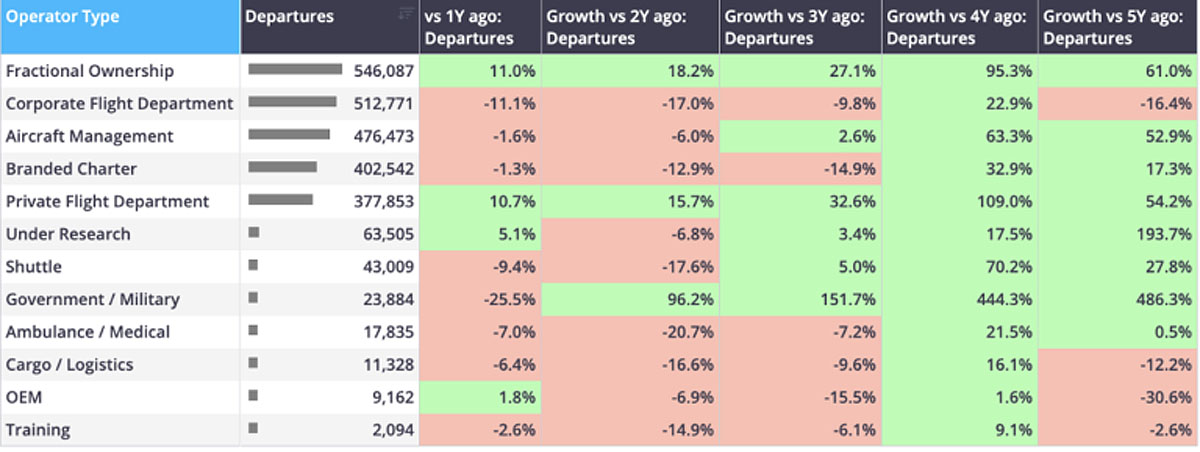

Chart 2: Business jet departures by operator type, US, full year 2024 vs previous years

2024 was the year of the Fractional operator in the US, fractional fleets posting record levels of activity. Over two thirds of Fractional activity was flown by NetJets, 2nd ranked Flexjet captured a quarter of market share. Several fractional operators recorded triple digital growth compared to 2019, notably Flexjet, Planesense and Airsprint.

In contrast to booming Fractional activity, Corporate Flight Departments flew 11% fewer flights compared to 2023, the active number of tails falling 7% compared to 2023. Private flying rose 11% compared to 2023, although the average hours per tailsign fell 1% compared to 2023.

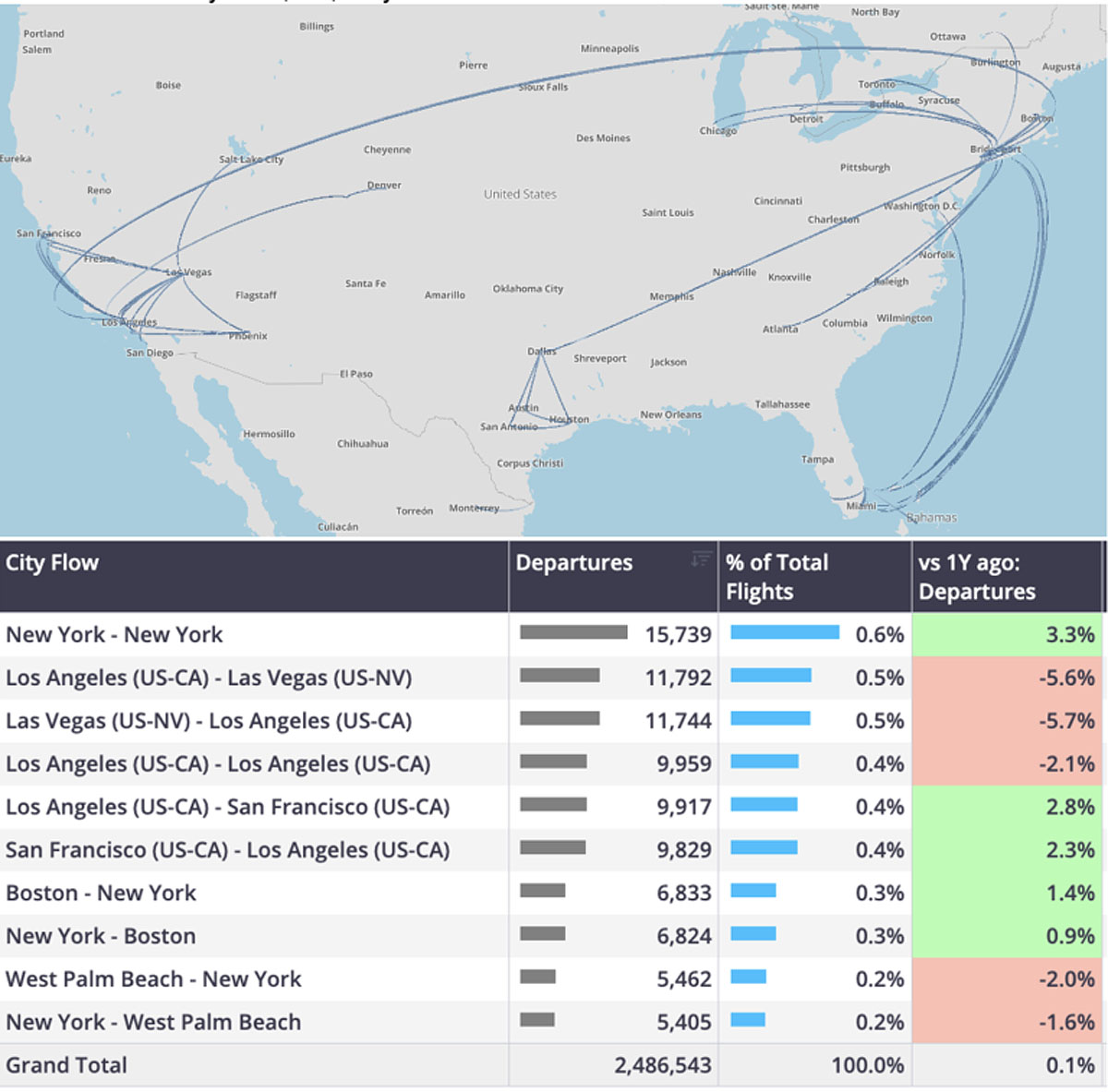

Chart 3: Busiest city flows, US, full year 2024.�

Florida earned the top spot for bizjet departures in 2024, activity out of the State on par with last year, 56% growth compared to pre-pandemic 2019. Texas and California completed the top 3 busiest States, Texas 1% ahead of 2023, California 1% below 2023. New Jersey, Tennessee and Ohio were busier than the last 5 years, Colorado behind the last 3 years.

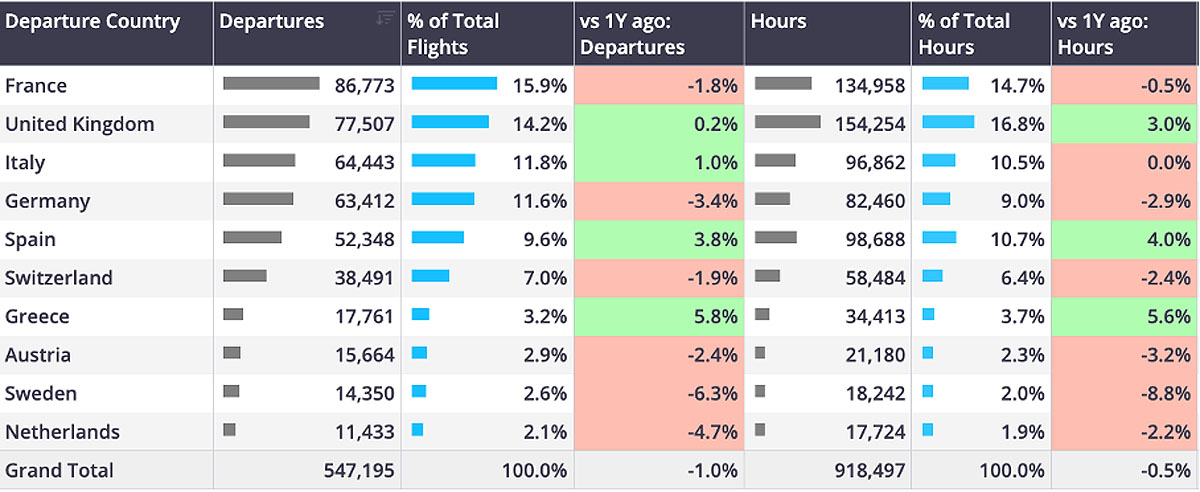

Europe

In Europe, bizjet activity in W51 grew 13% compared to W51 in 2023, strong rebounds in the UK, Germany and France compared to the same week in 2023. In Week 52, bizjet sectors were 7% ahead of last year, Part 91k and 135 sectors were 9% ahead of last year.

In Europe, the bizjet activity outlook is significantly subdued compared to the US. Bizjet activity in 2024 fell 1% compared to last year, 9% behind 2022, edging out ahead of 2019 by just 5%. Top market France saw declines compared to 2023 and 2022, 2nd ranked UK was on par with last year. Bizjet performance in Germany and Austria scored poorly in 2024, 7% declines compared to 2019, the only growth in the last 5 years was compared to locked down 2020. Elsewhere across Europe bizjet activity stalled in the Baltic countries and activity in Russia was almost 80% below 2019.��

Chart 4: Bizjet activity in Europe by country, full year 2024.

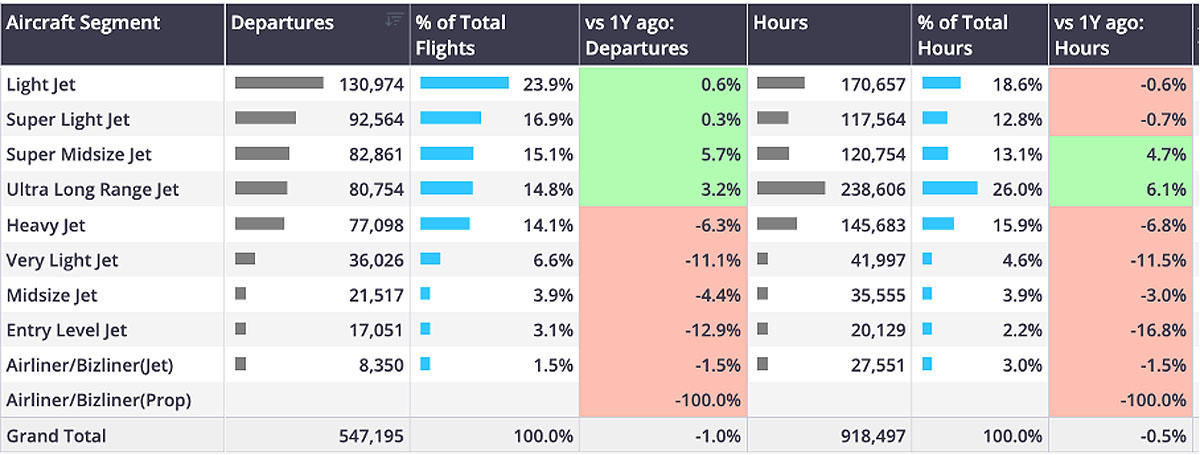

Fractional operators in Europe enjoyed similar success to their US counterparts, activity ahead of the last 5 years. Private fleets in Europe also recorded a strong year, activity ahead of the last 5 years. Across the OEMs in 2024, Cessna bizjets accounted for 36% market share, 5% fewer departures than 2023. Bombardier and Embraer types flew 4% more flights than last year, more deliveries of the Pilatus PC-24 aircraft in 2024 meant the type flew 15% more flights than 2023.

Chart 5: Bizjet activity in Europe by aircraft type, full year 2024.

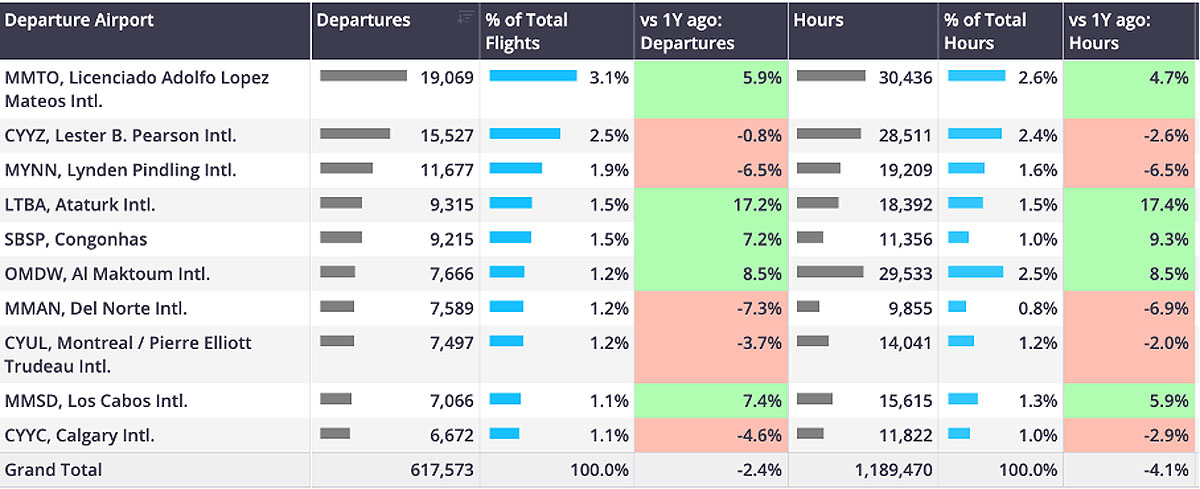

Rest of World

Outside of Europe and the United States, bizjet activity in W51 was 6% ahead of W51 in 2023, most growth coming from the Middle East, bizjet departures 14% ahead of last year. In Week 52 activity in the ROW region was 5% ahead of last year.

In 2024, bizjet activity outside of the United States and Europe fell 2% compared to 2023. Mexico and Canada were the busiest markets, although both in decline compared to last year. Pockets of growth recorded in Brazil, Australia and India, contrast 12% declines in China. Fractional operators recorded strong growth in the ROW region, departures up 10% compared to 2023, private flight departments recording 14% growth. Light jets flew the most flights, bizliners flying 19% fewer flights compared to 2023.

Chart 6: Bizjet activity in the ROW region by airport, full year 2024.