The recent weeks have shown a surge in demand for bizjet which we have not seen since the pent-up demand during the pandemic. The most obvious characteristic is fractional flying, with the top 5 fractional operators flying 12% more so far this year compared to last year. Eroding connectivity provided by US regional carriers could spur more users to shift to private aviation in the coming months.

Executive Summary

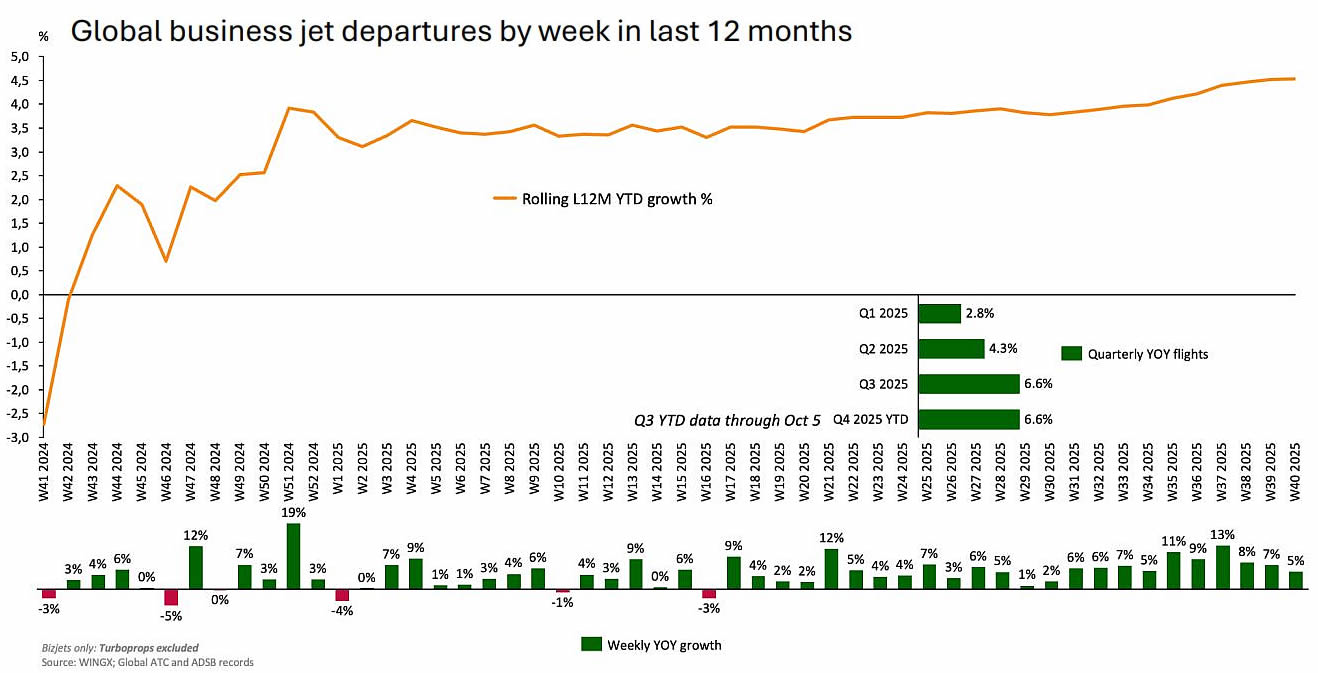

In Week 40 (29 September – 5 October), global bizjet activity reached 75,651 departures, down 5% compared to the prior week (Week 39) but up 5% versus Week 40 of 2024. On a rolling last four-week basis (W37 � W40), global business jets have accumulated 314,000 departures, an 8% increase compared to the same period last year.�

The streak continues: 24 consecutive weeks of year-on-year growth. Out of the 40 weeks so far in 2025, 37 posted gains, with the biggest surge of 13% in Week 37, and the largest decline just 3% in Week 16.�

Q3 2025 shattered records with over 1 million departures, it became WINGX’s busiest quarter ever, up 6.6% from Q3 2024 and a massive 33% above Q3 2019�s 750,000 flights.�

Fractional operators fuelled the boom, surging 12% in Q3. All top 10 fractional providers grew year-on-year, while NetJets commanded 57% of fractional traffic with 14% growth. Other standouts: Flexjet (+19%), Executive AirShare (+9%), Planesense (+23%), and JetFly Aviation (+10%). Fractionals now represent 19% of all business jet activity.�

Charter operations lagged significantly, crawling forward just 0.7% verus last year. One bright spot: top charter operator flyExclusive posted 13% year-on-year growth.�

Beyond Fractional and Charter, Q3 trends turned negative. Aircraft management slipped 1.5%, Private Operations fell 0.9%, and Corporate Flight Departments declined 5.7%.�

Chart 1: Global business jet departures by week in last 12 months

Regional Performance Analysis

North America: Steady 4% growth with strong four-week momentum

The North American market recorded 4% more activity in W40 2025 vs W40 2024, with total departures at 53,357. The U.S. mirrored this trend with a 4% expansion and 51,523 flights. Among key states, trends varied with Texas realising 7% growth, California with 4% growth, and finally Florida with 2% growth. North America�s rolling four-week trend tells a stronger story, now 9% ahead of the comparable period in 2024.

The big three states are driving momentum. Over the past four weeks, Florida and Texas both surged 8% while California rose 7%, collectively powering North America�s robust four-week performance.

Canada is having a breakout year. Q3 2025 delivered over 26,000 business jet flights, which is the busiest third quarter on record and more than 50% above Q3 2019 levels.

Europe: UK and Germany lead with 9% gains

The European market outperformed the overall global trend in Week 40, flights rising 6% compared to Week 40 in 2024. The top country performers in Europe were the UK and Germany, both recording a notable a 9% increase in flights compared to W40 last year. Switzerland and Italy grew below the European market trend, notching 2% and 3% gains respectively, while France was stagnant with no growth last week. Over the last four weeks, European activity has totaled over 50,000 flights, reflecting modest 3% growth.

The UK�s and Germany�s 9% growth last week was a significant improvement compared to their year-to-date trends of +1.5% and -6.3% respectively.

Rest of World: South America surges 28% year-over-year

Week 40 bizjet activity saw significant growth trends outside of North America and Europe. South America led growth yet again, outperforming mature markets with 28% higher traffic levels year-on-year. Africa was right behind and saw the second largest growth amongst ROW regions, +23%, while Middle East activity grew 15% and Asia grew 10%. These trends compared to the year-to-date growth rates of +9.5%, +13.8%, +7.0%, +2.1%, for the 4 regions respectively.

Current Events Analysis

WINGX estimates 2,000 SkyWest passengers at risk of losing service daily if Essential Air Service funding expires

The Trump administration announced that funding for the Essential Air Service (EAS) program will expire on Sunday, 12 October, as part of an ongoing partial government shutdown. The program subsidises commercial air service to 65 Alaska communities and 112 communities across the other 49 states and Puerto Rico that otherwise may lack scheduled air service. Among 28 participating airlines, SkyWest Airlines dominates with $195.8 million in annual government funding, serving 36 communities nationwide.

SkyWest operates these routes under its regional carrier brands: Delta Connection, United Express, and American Eagle. WINGX analysis of flight activity at the 36 EAS communities served by SkyWest from October 2024 through September 2025 shows the carrier operated 23,084 flights connecting 212 city pairs. WINGX translates this to approximately 436 weekly flights, or roughly 62 daily departures from these communities. The majority of these flights utilize small regional jets with 30 to 50 seat configurations. Using a conservative estimate of 30 passengers per flight, the loss of these 62 daily SkyWest EAS flights would impact approximately 1,860 passengers per day who would need alternative transportation options from their rural communities.

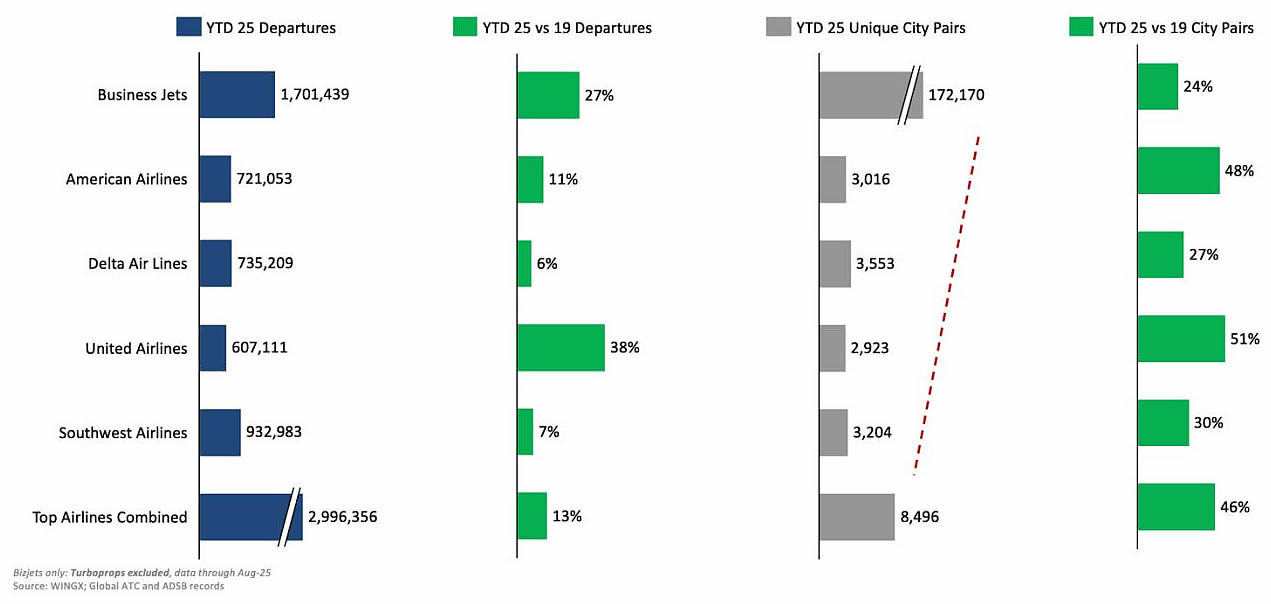

Chart 2: Unique city connections served by business aviation vs major air carriers. US business aviation departures provide 20x more unique city pairs than the major US scheduled airlines