WINGX�s weekly Business Aviation Bulletin.

Overall Comment

After seven months of trailing behind the recovery in the US, the recovery in business jet demand in Europe is surging ahead as we reach the peak of the summer season. Growth in the US market has softened slightly but it´s not yet clear whether the resurgence of the Delta variant will put a dent in the record-breaking trend established since the Spring of this year.

Global

Business jet activity continues to exceed comparative activity in 2019, with 91,424 jet sectors flown globally in the first 10 days of August 2021, up by 8% compared to August 2019, up by 31% compared to August last year. This compares to Scheduled Commercial Airlines, activity still trailing comparable August 2019 by 40%. North America region is seeing 6% growth in bizjet sectors this month, with the airline sectors back by 38%. The recovery in Europe is now stronger, with 12% more business jet activity so far this month than in August 2019. In aggregate, the recovery in all other regions is also robust, business jet flights up by 13% compared to August two years ago.

Global Business Jet flight activity in Jan 1st– August 10th 2021

North America

In the North American region, business aviation activity is 2% behind August 2019, with the turboprop sector slowing this month. The United States, with an active fleet of 9,732 business jets this month, is still posting some significant growth, jet sectors up by 16% through 10th August 2021 versus same period August 2019. Business jet demand in Canada and Mexico is stuttering back to normal, flights down by 30% compared to two years ago. That´s not much improved on a YTD basis, in contrast to the US for which activity is up 8% so far this year, the rebound still accelerating. A slew of Caribbean destinations continues to see record activity, with US Virgin Islands, Dominican Republic, Puerto Rico seeing 20% more activity than ever before this year. Business jet arrivals into Turks and Caicos this month are up 147% compared to August 2019.

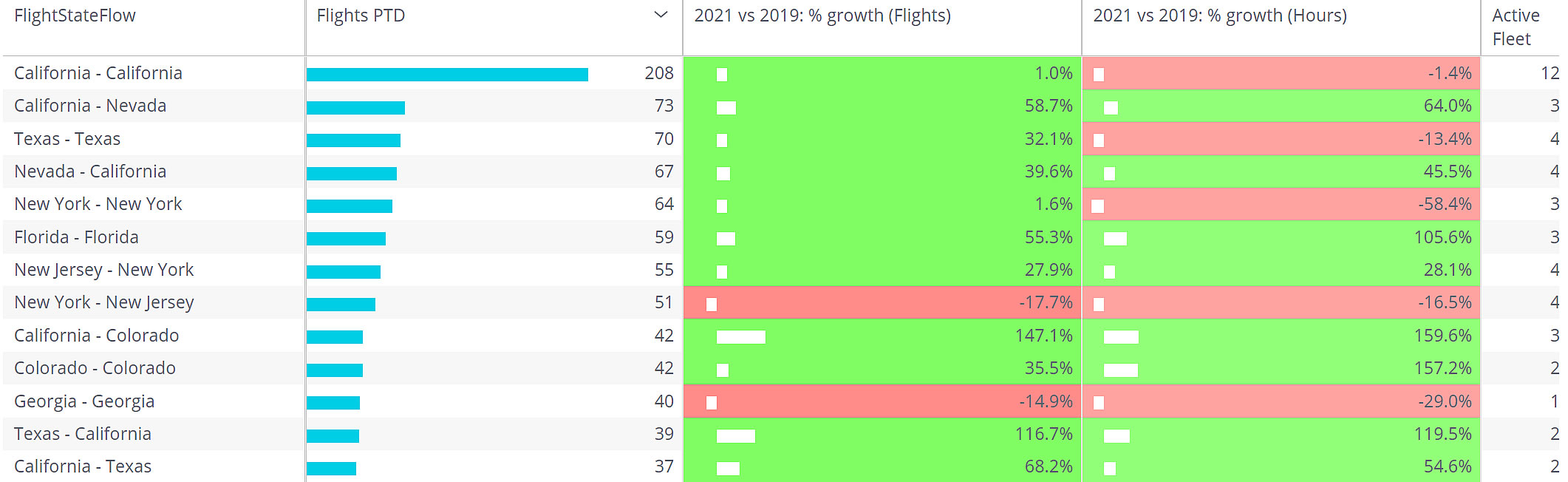

Year to date, super midsize jets have flown 12% more activity than in 2019, with the same trend holding through August. Ultra-long range jet activity is still trailing 2019 levels by 10% but in the last two months the longest-range jets have flown more than ever, sectors up 15% so far this month compared to August 2019. Even flight hours are up 8%, indicating a recovery in longer trips. There is a marked divergence in trends, with ULR flights within California just about restored to 2019, whereas ULR departures from California to Nevada are up 54%. Flights from California to Colorado are up by 150%, and ULR flights from the US to Turks & Caicos are up 600% compared to August 2019. Teterboro has had the largest share of ULR flights, but biggest growth has come from airports like Westhampton, McCarren and Burbank.

Ultra Long Range Jet connections in the US August 2021 vs August 2019

Europe

Just like last year, August is seeing a strong resurgence of business jet demand. The pace of the recovery is unevenly spread, with Italy, unusually, posting the largest number of business jet sectors so far in August. With departures in Italy up 22% compared to the first ten days of August 2019, this is undoubtedly a new record. The only European countries with business jet activity materially below pre-pandemic trend this month are UK, Ireland, Sweden and also Turkey, which correlates with renewed concerns and restrictions around the pandemic. Switzerland has seen a very big jump in business jet activity this month, arrivals up by 26% compared to August 2019. Flights into Croatia and Montenegro are 50% above pre-pandemic levels.

The most fashionable sunspot locations � Ibiza, Olbia, Mallorca � are the busiest business jet hubs this August. Olbia´s arrivals are 18% higher than August two years ago. Most of this growth is coming from light jets, with Phenom 300 arrivals to Olbia up by 130%, Citation CJ1 flights up by 70%, CJ3 arrivals up by more than 10X. Most of the departure points into Olbia are from within Italy, this activity up 40% on pre-pandemic August 2019. Nice is the busiest airport in Europe this month, registering 23% more activity than two years ago. Thirty eight percent of these operations are branded charter. Most of the other busy European airports are showing trends higher than in August 2019, notably Zurich, Geneva, Ciampino. Leading UK airports such as Luton and Farnborough are starting to see more activity but still behind 2019 trends. Biggin Hill is an exception, with business jet departures this month up by 15% compared to two years ago.

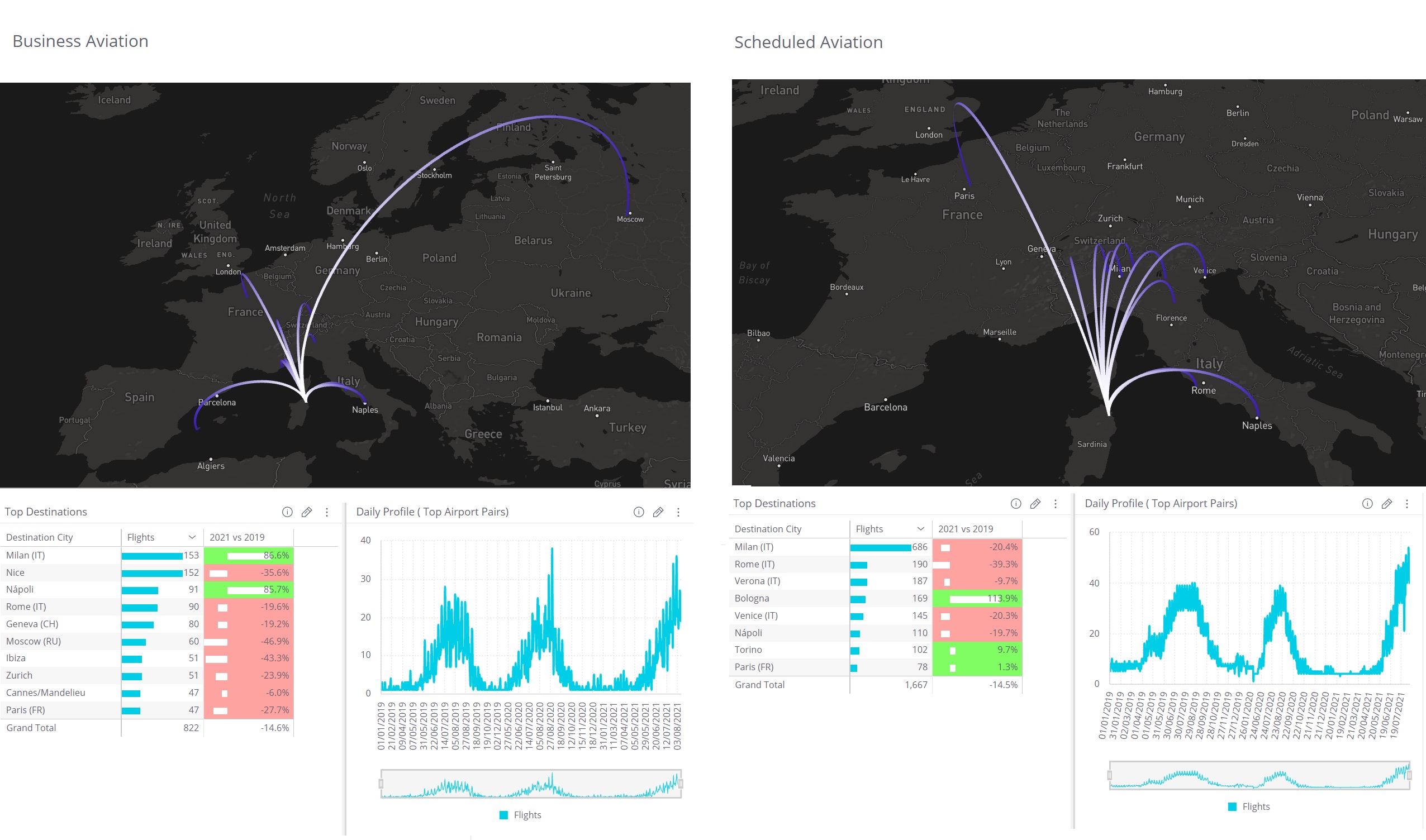

Business Aviation vs Scheduled Aviation connections with LIEO / Olbia Airport, July and August 2021

Rest of World

Outside the US and Europe, there are mixed trends in recovery in the largest markets for business jets: the recovery in Canada is very sluggish, consistent with ongoing restrictions; but across Australia and New Zealand, despite international travel restrictions, domestic business aviation traffic is higher than ever; in Africa and South America, where the pandemic is still very much at large, several countries have seen much more business jet travel than before 2020; in China, domestic business aviation travel has beaten records, but international traffic is almost standstill. The Middle East, specifically the UAE, has seen very resilient business jet travel, especially to and from Dubai.

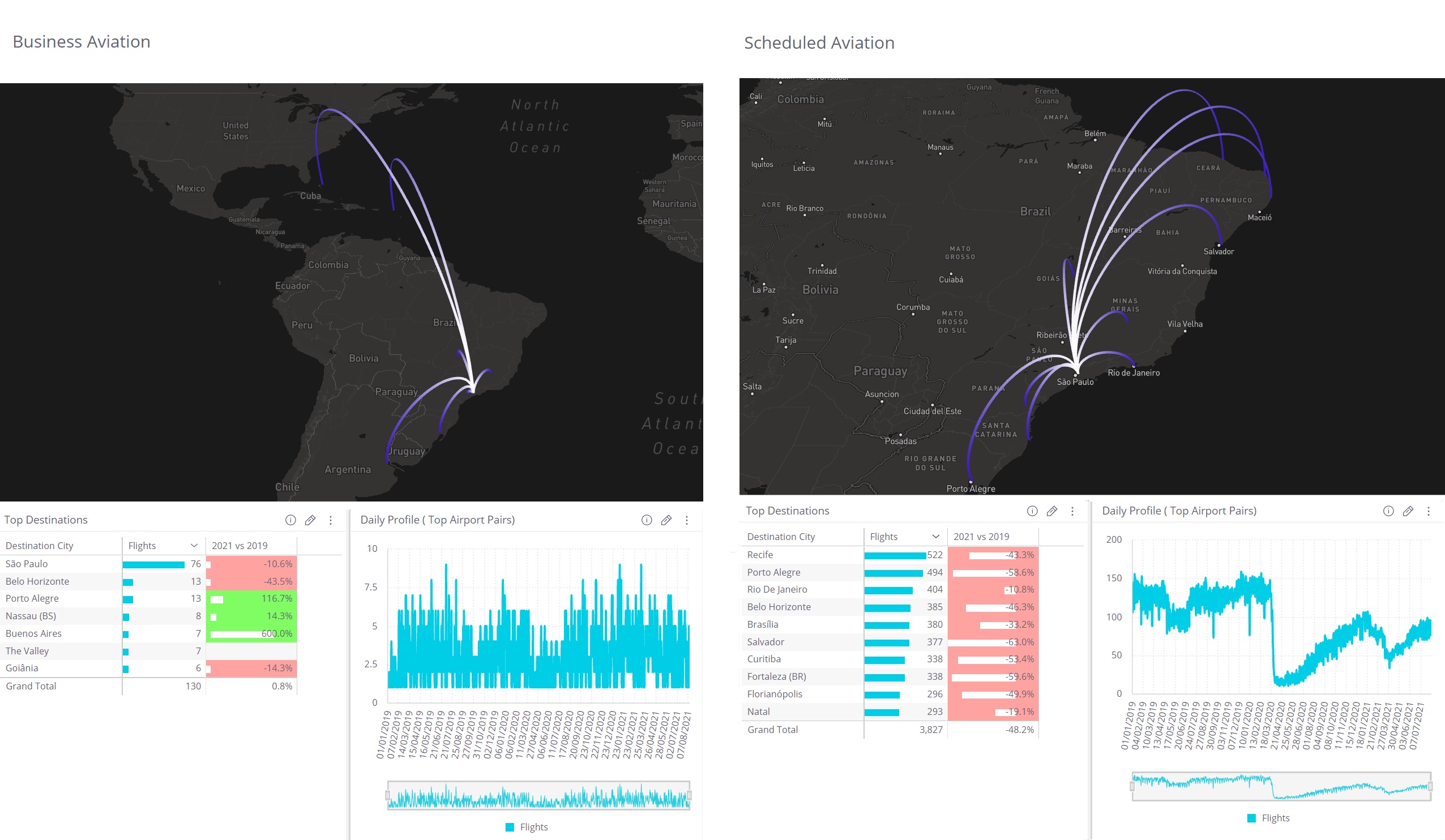

Business Aviation vs Scheduled Aviation connections with SBGR / São Paulo/Guarulhos International Airport, YTD 2021