WINGX�s weekly Business Aviation Bulletin.

Overall Comment

Last month IATA estimated that its passenger numbers would not recover before 2024, which gives business aviation an extended window to consolidate its advantage in connectivity and keep first time users in the industry. The challenge which is clearly emerging is capacity constraint; the leading charter and fractional operators in October 2021 are flying at annualised rates of over 1,000 hours a year, which may not be sustainable. With seasonal demand peaking in the next month in the US, it will prove very challenging to maintain service levels.

Global

October 2021 is well-set to be the busiest ever month for the activity of business jets globally. After almost three weeks of the month, 200,000 sectors have been operated, surpassing the number of flight departures in October 2019 by 19%, and eclipsing October 2020 by 44%. The recovery of the commercial airlines, which stuttered as the Delta variant prolonged the pandemic, are flying 30% below levels in October 2019. Almost ten months into the year, business jet sectors are 4% up on the comparable pre-pandemic 2019 period. The cargo sector continues to thrive, although these operators are up only 1% this month, up 7% for the year. Scheduled airlines are flying 40% below pre-pandemic so far this year, with stronger improvements finally coming through this summer.

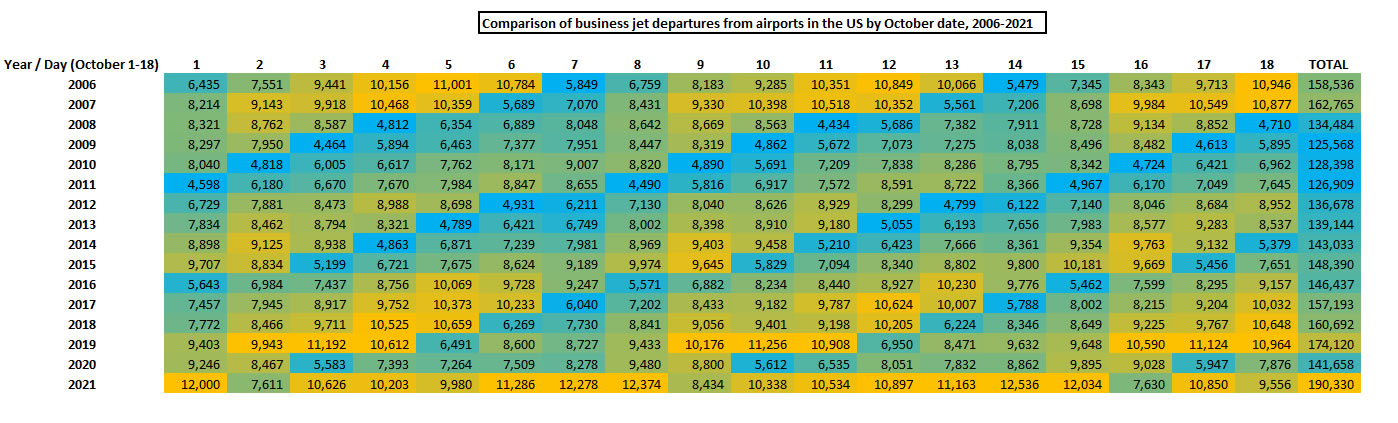

Analysis shows that in eight of the first eighteen days of October, this month has seen the busiest days since 2006 for the US, for business jets and turboprops. The strongest periods this month are clearly Wednesday to Thursday traffic, and Sundays. Thursday 14th October was almost certainly the busiest ever day, eclipsing the busiest ever previous 14th October, back in 2015, also a Thursday, by 27%. By aircraft segment, October is the busiest on record for Ultra-Long Range, Heavy, Super Mid, Super Light and Very Light Jets. Midsize Jets were much busier in 2006, mainly the Hawker fleet, and Light Jets were slightly bigger at their peak in 2007. Ultra Long Range jets have operated 3,174 sectors from US airports 1st-18th October, 94% up on activity back in 2006. Versus October 2019, the two ULR jet platforms with the most growth, over 30%, are Gulfstream 600 and Global 5500.

US business jet activity by day, October 1st-18th 2006-2021

North America

Record-breaking business jet activity was one reason for the optimism at NBAA last week, the first convention since 2019. As a proxy for the event’s popularity this year, business arrivals into all the Last Vegas airports in the 5 days running into the show were up 16% on the number of inbound flights into NBAA in 2019. Stepping back to the overall North America region, for jets and props, movements this month are up 16%, up 19% in flight hours. Domestic US traffic is up 20%, with double or even triple that growth for Caribbean islands including Dominican Republic, Turks & Caicos and Aruba. The Part 135 and 91K market is booming in the US, with branded charter operators running at 30% above comparable 2019. Florida this month is seeing more than 50% increase in charter and fractional activity, South Carolina is up more than 70%. Year to date, Palm Beach airport departures are up 38%.

US business jet arrivals into Las Vegas airports during NBAA, 2021 vs 2019

Europe

After two exceptionally busy months, European business aviation activity is back on par with pre-pandemic volumes. Business jet departures from airports in Europe are up 29% against October 2019. Busiest country France has seen a 22% bounce vs 2019 in departures this month, the UK is next busiest, having been outside the top five countries earlier this summer. Business jet arrivals into Italy and Spain are up 40%, into Turkey, up almost 70% compared to October 2019. Arrivals into Greece are actually down 0.1% versus October 2020 but up 40% compared to October 2019. Ireland and Norway are two of the only countries with fewer arrivals this year than October 2019. Charter operators are clearly at full stretch, fleets operating 36% more than in October 2019. The top 12 charter operators in Europe all have a run-rate of more than 50 flight hours per unit, through 19th October.

Business aviation sector length, departures from Europe October 2021 vs 2020, 2019

Rest of World

Utilisation of business jets outside Europe and the US is at a much lower ebb, averaging only 10 hours per aircraft during the first half of October. But overall flight activity is still well up on October 2019, sectors +31%, flight hours up by 12%. Brazil, China, UAE and India are seeing record numbers of business aviation departures, although China is still behind 2019 in flight hours. Of the leading markets, Australia and Saudi Arabia have lower volumes than in October 2019. Compared to last year, domestic flights outside North America and Europe are up by 27%, and international flights are on the rebound up by 51%. But to put that in context, domestic flights compared to October 2019 are up 59%, with international flights still lagging by 2%.