WINGX�s weekly Business Aviation Bulletin.

Summary

Business aviation activity is still well ahead of pre pandemic, despite the weakening economy, with falling freight traffic underlining this decline. The sclerotic pace of recovery in scheduled airline is almost certainly sustaining the momentum in bizjet demand.

Global

17 Days into October global business jet and prop activity was 1% behind October last year, 10% above pre-pandemic October 2019. Focusing on business jets, flights so far this month are down 3% compared to last year, although still up 15% compared to pre-pandemic October 2019. Scheduled airlines are flying 9% more than last October, however, activity is 22% below three years ago. Focusing on the top global airlines – Southwest Airlines, American Airlines, Ryanair, Delta Airlines and United airlines, passenger airline flights so far this month are 16% above last year, 1% less than three years ago. Dedicated freight activity is down compared to the last three years, 10% below last year, 7% below 2020 and 8% below 2019.

Global Fixed Wing activity October 2022 compared to previous years

North America

Business jet flights in North America are recovering from an initial hit due to Hurricane Ian, activity is now within 1% of October last year, 15% busier than October 2019. In Week 41 ending 16th October, activity increased by 4% compared to the previous week, in the last four weeks activity is 1% above the same period last year.

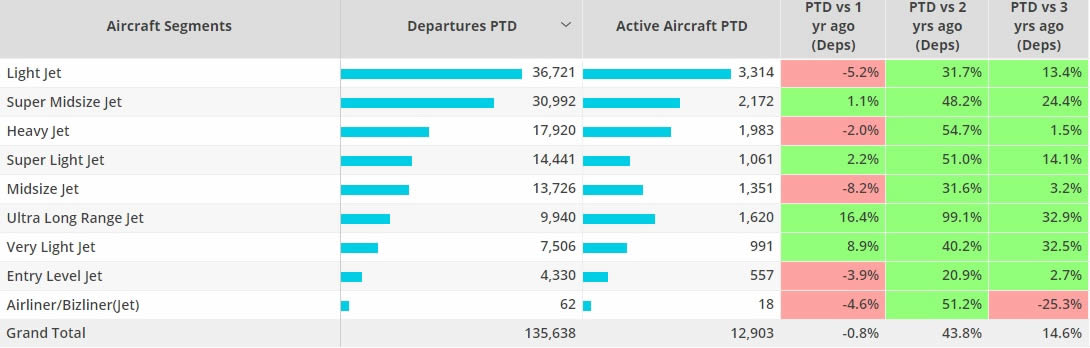

Activity across aircraft segments is mixed, light jets are the busiest, although activity is down 5% compared to last October. Midsize jets are seeing the greatest declines compared to last year, activity is down 8%, although 3% above three years ago. Ultra-Long Range jets continue to see the largest rebound compared to pre-pandemic October, activity is 33% above three years ago, 16% above last year.

North American Business jet segments, October 2022 compared to previous years

Private flight departments are driving demand in October across the region, activity is up 13% compared to last year, 23% above three years ago. Fractional programmes, aircraft management and branded charter are all seeing dips in demand compared to last year.

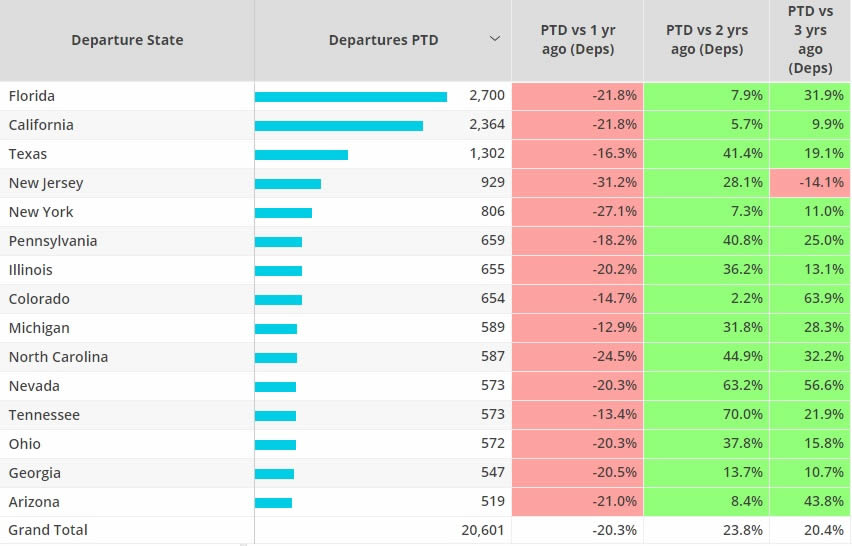

Branded Charter fleets are seeing the biggest decline across North America, flights are down 20% compared to last year, although 20% above three years ago. In week 41 Branded Charter flights across the region were down 17% compared to last year, down 18% in the last four weeks compared to last year. So far this month Light jets are the busiest aircraft in branded charter fleets, activity is 39% above three years ago, although 16% below last year. Heavy jets are seeing the largest declines year on year, down 33%, down 2% compared to three years ago. The main bizjet hotspots are seeing a drop off in branded charter departures, Teterboro and Van Nuys seeing Y-O-Y declines as well as declines compared to three years ago. Florida and California have seen activity drop 22% compared to last year, although both above October 2019. New Jersey has seen demand slump, departures down 31% compared to last year, 14% below three years ago.

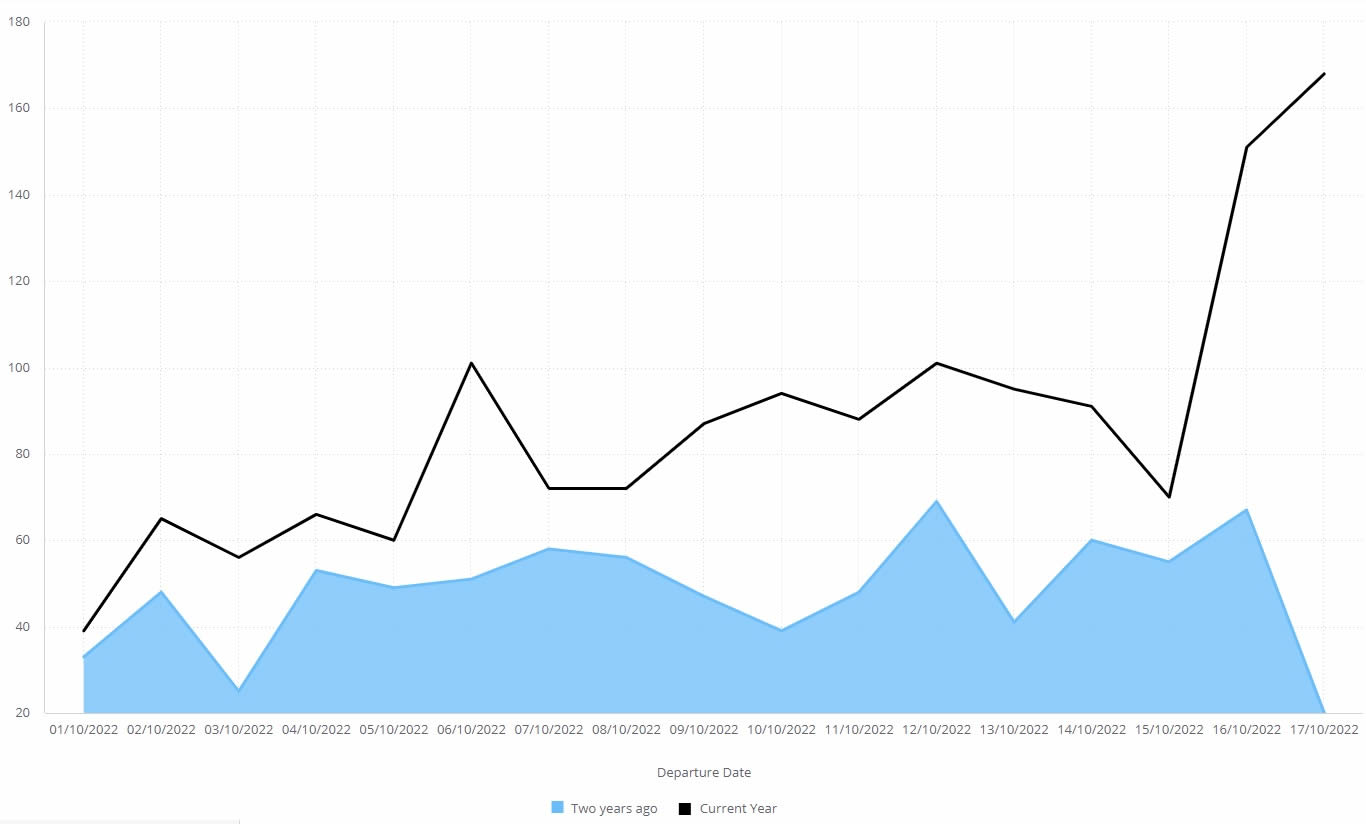

Airports near NBAA-BACE conference this week are seeing a large influx of business jets. Between October 1-15 there were on average 77 daily bizjet arrivals into KORL, KISM, KMCO and KSFB airports. During the two days prior to the conference this had jumped 106% to 159 average daily arrivals. Compared to the 2019 event in Las Vegas (KLAS, KVGT, KHND), total business jet arrivals in the 7 days prior to the event are down 29%.

Bizjet Arrivals into NBAA � BACE Orlando airports, October 1 � 17 2022 compared to 2020 non-event year

Branded Charter Departures by North American state, October 2022 compared to previous years

Europe

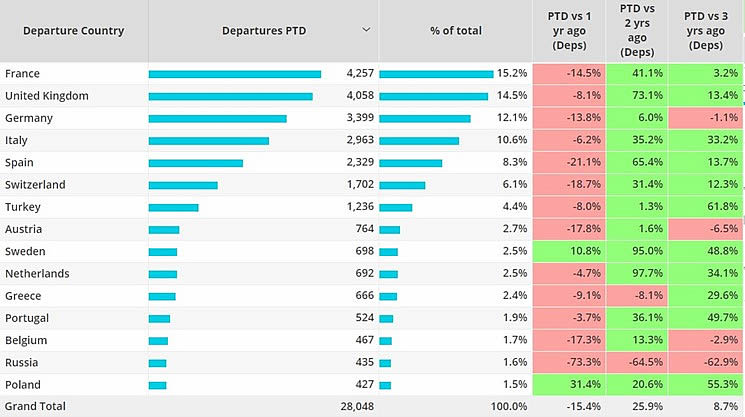

The business jet market in Europe continues to fall behind last year, flights so far in October are down 15% compared to last year, although up 9% compared to three years ago. In the last four weeks activity has fallen 13% behind last year, in Week 41 activity rebounded 1% compared to the previous week. Aircraft management and branded charter fleets are seeing the largest slowdowns so far this month. Private flight departments and fractional programmes are seeing huge gains compared to three years ago, 70% and 41% retrospectively. The biggest drop offs in activity are coming from most of the region’s hotspots. France and Spain are seeing double digit decline compared to last year, Germany down 1% compared to three years ago, UK and Italy seeing single digit declines compared to last year.

Business jet activity trends by European country in October 2022

Rest of World

Outside of North America and Europe, business jet activity is 15% above last year, 52% above three years ago. Just over 11,000 flights were operated between October 1 and 17, Brazil accounted for 16% of that activity. Flights from Brazil were down 2% compared to last year, up 57% compared to three years ago. Australia, the second busiest market, is seeing 76% growth in activity compared to last year, 68% above three years ago. São Paulo- Congonhas and Al Maktoum airports have seen a decline so far this month compared to last year, although both well up compared to three years ago. King Khaled Intl has seen 20% more activity this year compared to last, although 8% less than three years ago. Seletar is booming, more than 4x the activity so far this month compared to last year. Heavy jets are the busiest ROW aircraft segment, followed by ultra-long range jets. Bizliners are the only segment still behind pre-pandemic activity, down 8%, although 7% above last year.