WINGX�s weekly Business Aviation Bulletin.

Summary

The last few months have seen the post-covid bounce in business jet demand fall away, and in Europe this winter we are starting to see lower activity levels than in 2019. The recessionary outlook for the economy is likely to bake this decline into 2023. The US market looks more resilient, with modest declines compared to last year, edging the market towards a trajectory of 5%-10% gains over 2019 during 2023.

Global

Business jet and turboprop flights fell 2% in the first 18 days of December this year versus December last year, still 10% above three years ago. For the almost-complete year of 2022, global business aviation activity is up 10% on 2021, up 54% on 2020, up 14% on 2019. For the most recent week, Week 50, global bizjet flights were up 6% on week 49, but down 3% on week 50 last year. Scheduled airline sectors are flying 12% ahead of last year so far this month, 20% behind December three years ago. Global freighter activity is down 9% compared to last year, 5% above three years ago.

Global fixed wing flights, December 2022, compared to previous years

North America

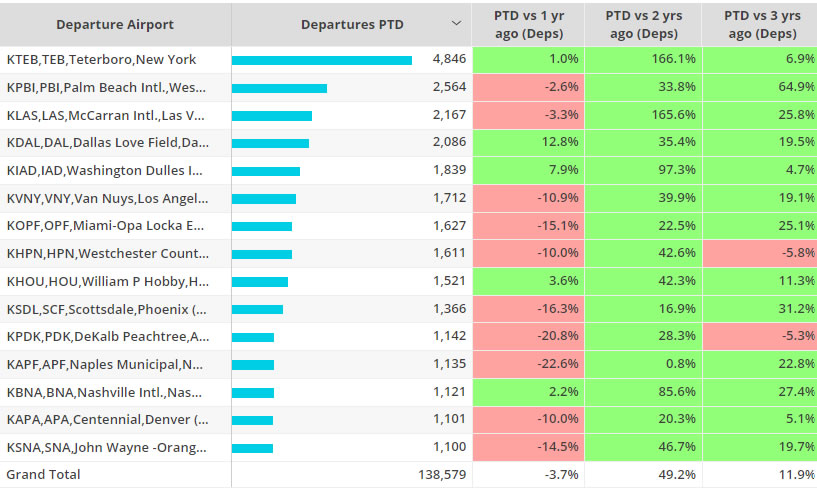

Business jet activity in North America in terms of flights operated is trending down by 4% this month compared to last year, though still 12% up on December 2019. In terms of flight hours, the gain on December 2019 is 17%. On a year-to-date basis, the bizjet market in North America is up 12% compared to 2021, up 18% versus 2019. The 50,456 business jet sectors flown in Week 50 compare to 57,147 sectors flown at the record high point flown in Week 14 this year. Week 50 was 3% busier than Week 49 as the holidays approach, but 4% down on comparable Week 50 in 2021.

Bizjet departures by North America airport, ranked by departures December 2022 compared to previous years

Bizjet activity is varied by operator type this month. Branded charter activity is down 21% compared to December 2021, whereas Private Flight departments are up 9% compared to last year, up 25% compared to three years ago. The year-to-date trend for Charter and Fractional fleets is almost 30% up on 2019, although the charter market is a few points down on full year 2021. Corporate fleets are 18% busier this year than last year, with 5% gains on 2019. Private flight departments have the biggest share of total activity, about 25%, and the largest growth compare to 2021, up 22%.

Europe

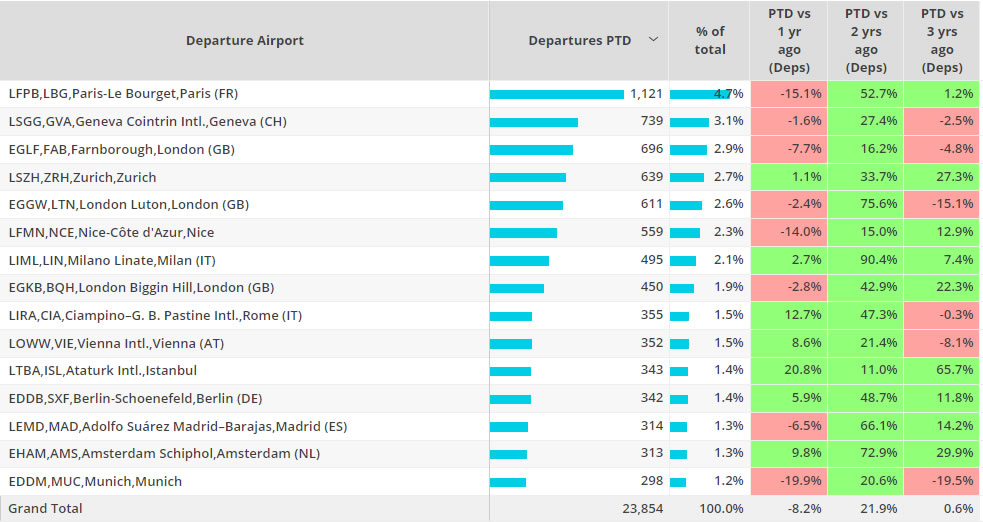

Business jet flights in Europe are trending 8% down on December last year, converging to the same volume we saw in December 2019. For Week 50, business jet departures in Europe were 7% down on Week 50 last year, slightly improved on the 11% downward trend in the last 4 weeks. France has the weakest trend in Week 50 with an 18% drop-off in flight activity. For December so far, the UK is the busiest market, and still growing compared to last year. In contrast, France, Germany and Spain are all seeing declines in December 2022 versus December 2021. At the airport level, trends vary between 15% declines at French airports like Nice and Le Bourget, and 12% gains at Ciampino and Ataturk.�

Bizjet departures by airport from Europe, December 2022 compared to previous years

Rest of World

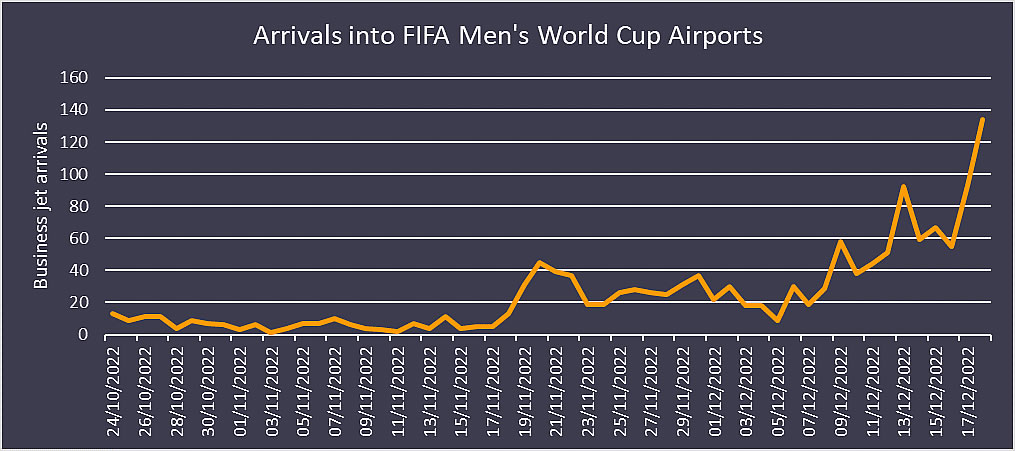

Business jet sectors outside of North America and Europe continue to trend well above pre-pandemic December, activity is 57% higher than in 2019, 18% higher than last year. In the last four weeks activity in Africa is up 16% compared to 2021, Asia up 32%, South America down 5%. In the Middle East activity is up 33% compared to last year. As the FIFA Men’s World Cup drew to a close last weekend (December 18th), key World Cup airports OTHH, OTBD, OTBK saw 451% growth in average daily arrivals during the 29 days of the tournament compared to the previous four weeks. On December 18th, the day of the final, key World Cup airports saw 198% more arrivals compared to November 20th, the day of the opening ceremony.

Arrivals into FIFA World Cup Airports