WINGX�s weekly Business Aviation Bulletin.

Summary

Business jet activity is holding up, losing some ground to last year’s record January activity, when the end of lockdowns released a surge of pent-up demand. Transatlantic flight activity is still growing. The US charter market has come off last year�s highs but is still much bigger than pre-pandemic. Regions like the Middle East are still seeing record business jet flight activity.

Global

Sixteen days into January 2023 and business jet and turboprop sectors are 3% ahead of the same 16-day period in 2022, 16% ahead of 2019. Focusing on just business jets, sectors are 1% ahead of last year, 20% ahead of 2019. Between January 16th 2022-2023 there were 3.7 million bizjet sectors flown, 11% more than the previous 12 months, Jan-21 to Jan-22. Between January 16th 2022-2023 there were 1.8 million turboprop sectors, 7% more than the previous 12-month period. Global scheduled airline sectors are up 21% compared to January last year, 11% down on 2019. Looking at the world�s busiest airlines (Southwest Airlines, American Airlines, Delta Airlines, Ryanair, United Airlines), passenger airline activity is up 20% compared to last year, 3% higher than January 2019. Freighter activity has dropped off compared to last year, sectors down 5%, activity is almost on par with January 2019.

Global fixed wing flights, 1st – 16th January 2023 compared to previous years.�(note business aviation includes turboprops)

North America

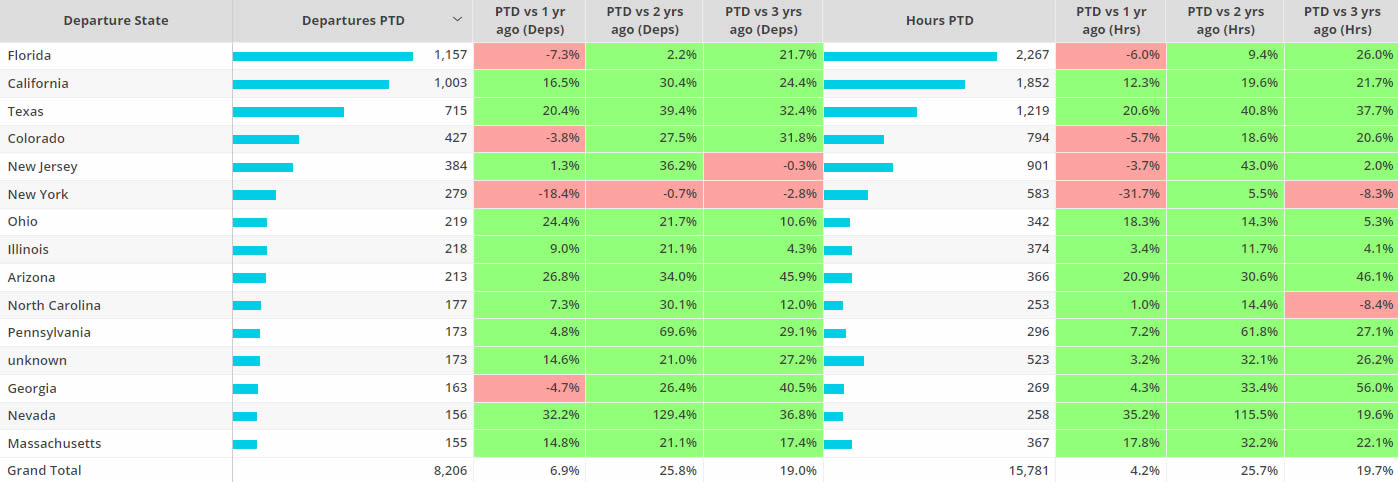

115,000 business jet sectors departed from locations in North America in the opening 16 days of January, on par with the same 16-day period last year, 19% more than in January 2019. Flight hours for the same period are down 1% compared to last year, 31% above 2019. So far this month fractional operators are seeing 41% growth in sectors flown compared to pre-pandemic January 2019. Private flight departments are flying 23% more sectors than in January 2019, demonstrating the effect of new aircraft owners. Despite an 18% drop compared to January last year, branded charter sectors are trending 20% higher than in January 2019.

Over half of all bizjet flights in North America this month have been less than 1.5 hours in length, flights of this duration are up 4% compared to last year, 12% higher than 2019. Flights between 6-12 hours have seen a large rebound compared to last year, departures up 18%. Despite 19% growth compared to 2019, Ultra Long-Haul flights (12+ hours) are down 17% compared to last year. There were 17,000 North America � Europe bizjet flights between January 16th 2022 � 2023, 54% more than the previous 12 months. Between 1st � 16th of January this year there were 700 flights, 29% more than last year, 35% more than 2019.

Business Jet sectors by duration, North America, 1st � 16th January compared to previous years.

The Bombardier Challenger 300/350 is the busiest jet so far this month, whilst light jets are the busiest aircraft segment. The Challenger 300/350 flew 7% more sectors in the opening 16 days of this month compared to 2022, 20% more 2019. Flight hours over the same period were 4% higher than last year, 21% more than 2019. Florida is the busiest state for Challenger 300 departures, departures down 7% compared to last year. Compared to January last year California and Texas are seeing double digit growth in Challenger 300/350 departures, whereas Colorado down 4% compared to last year. Van Nuys � McCarran is the busiest branded charter bizjet airport pair in the North America region, followed by Opa-Locka � Teterboro.

Bombardier Challenger 300/350 departures by State, January 2023 vs previous years

Europe

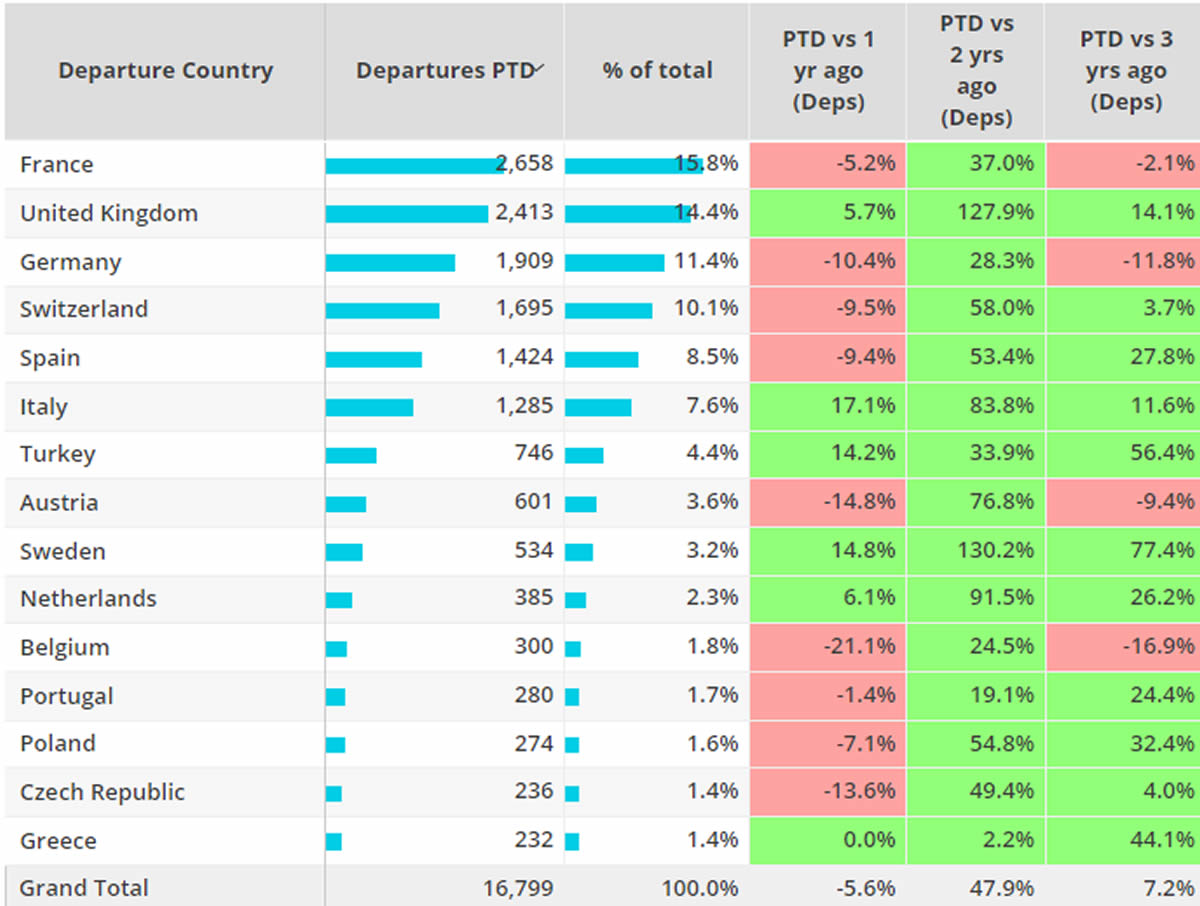

16 days into January business jet flights in Europe are down 11% compared to the same period last year, still 7% busier than pre-pandemic January 2019. Demand across the major bizjet markets is mixed so far this month. France, the busiest market is seeing a 5% decline in sectors compared to last year. The UK has started January faster than last year, sectors are up 6% compared to the same 16-day period last year, meanwhile Germany and Switzerland are seeing double digit declines compared to last year. Excluding Russia from European bizjet trends, departures are down 6% compared to last year, 7% more than 2019.

European bizjet markets, excluding Russia, 1st � 16th January 2023 compared to previous year.

International flights account for 71% of bizjet flights in Europe so far this month. International sectors are up 7% compared to 2019, although down 12% compared to last year. Domestic bizjet flights are up 8% compared to 2019, 7% below last year. 64% of bizjet flights so far this month are less than 1.5 hours in duration, sectors of this length are up 11% compared to 2019, although down 2% compared to last year.

Business Jet sectors by duration, Europe, 1st � 16th January compared to previous years.

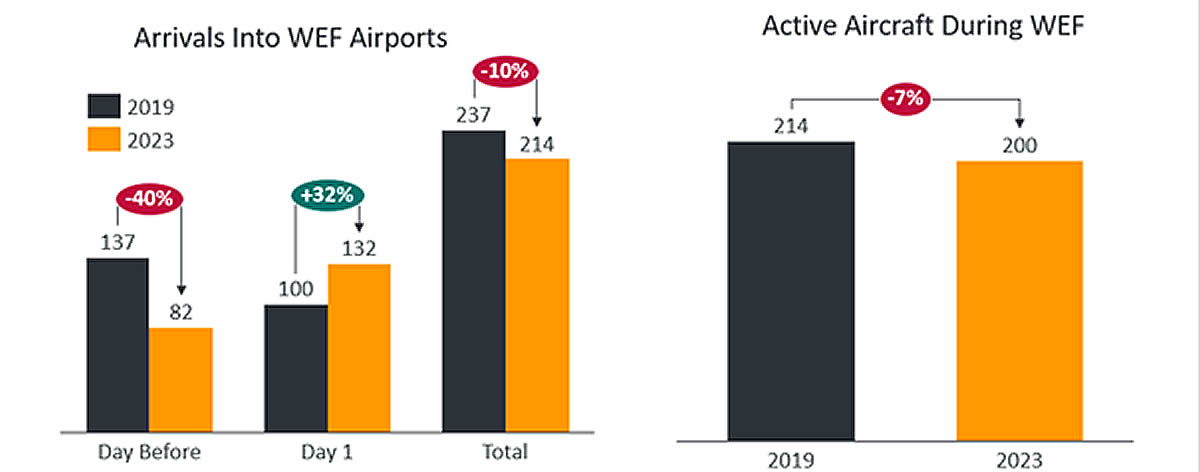

Davos hosts the World Economic Forum this week (January 16th � 20th), the event opening on the 16th of January. Business jet arrivals into nearby airports (LSZS, LSZH, LSMD, LSZR) on the day before the 2023 event were down 40% compared to the 2019 event, although up 32% compared to the opening day in 2019. Overall business jet arrivals are down 10% compared to the same 2 day period during the 2019 event. There were 200 active bizjet aircraft during the day prior and day 1 of this years event, 7% fewer than the same period in 2019. The top airport pair in the 2-day event period this year is Luton � St Gallen Altenrhein, followed by Luton � Zurich.

Business jet arrivals & active aircraft into WEF airports (LSZS, LSZH, LSMD, LSZR), day prior and day 1 of WEF 2023 compared to 2019.

Rest of World

Outside of North America and Europe, bizjet activity is 35% above the same 16-day period in January last year, 83% above pre-pandemic 2019. Half of all flights in the Rest of World region are less than 1.5 hours in duration. Ultra-Long-Range flights are still behind pre-pandemic 2019 by 14%, although triple digital growth compared to last year. Brazil is the busiest ROW market so far this month, sectors up 23% compared to last year. India and Argentina are seeing triple digit growth compared to last year, departures from the United Arab Emirates are on par with last year. China is seeing a rebound in activity, bizjet sectors up 31% compared to January last year, Beijing is driving the activity, departures up 51% compared to last year, Sanya up 63%, Shanghai up 12%.