WINGX�s weekly Business Aviation Bulletin.

Summary

The downwards drift in bizjet demand in Europe is starting to get concerning, with the charter market seeing the biggest drops, especially in central Europe. Conversely, transatlantic jet traffic is still well up. In North America, activity trends are mixed, with light jet charter falling back. In China, bizjet activity is rebounding post covid, but still behind 2019.

Global

30 days into January business jet and turboprop sectors were 2% ahead of comparable 2022, 15% ahead of 2019. Turboprop sectors over the same period are 6% ahead of last year, 10% ahead of 2019. Business jet sectors are seeing slower growth, 1% more than January last year, 17% more than in January 2019. Looking back at the last 3 months (30/10/23 –30/01/23) business jet sectors have fallen 2% compared to the same period last year, still 18% above three years ago. In the last 30 days scheduled airline sectors are 24% above the same period last year, down 11% compared to January 2019.

�

Focussing on the top 5 global airlines (Southwest Airlines, American Airlines, Delta Airlines, United Airlines and Ryanair), flights this month are up 22% compared to last year, 5% above 2019. Despite 8% growth compared to pre-pandemic January, dedicated freighter sectors are down 7% compared to January 2022.

Global fixed wing flights, 1st � 30th January 2023 compared to previous years. (Note business aviation includes turboprops)

North America

214,000 business jet sectors flew out of airports in North America between 1st � 30th January, on par with last year, 15% ahead of 2019. Flight hours for the same period are 1% behind last year, 17% ahead of January 2019. As January draws to a close private flight departments have flown 8% more sectors than January last year, 21% more than in 2019. Aircraft management programmes are flying 5% less than last year, although 11% ahead of 2019. Branded charter declines have picked up, sectors between 1st � 30th January this year 18% below comparable January last year, 13% ahead of 2019.

Teterboro is the busiest departure airport for branded charter flights in North America so far this month, followed by Van Nuys.

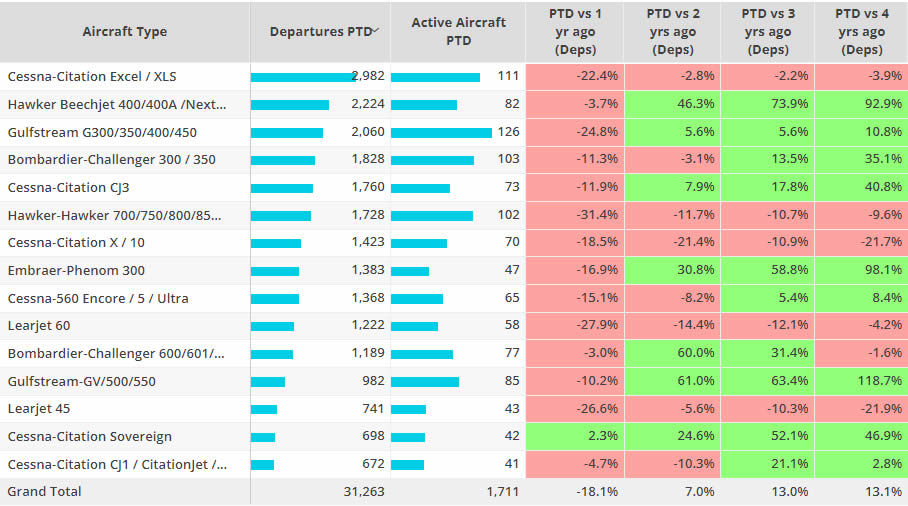

Light jets are the busiest in the branded charter fleets this month, flights down 15% compared to last year, 24% above 2019. The Cessna Citation Excel /XLS is the busiest branded charter aircraft type so far this month, although flights are down 4% compared to January 2019. Van Nuys � Las Vegas McCarran is the busiest branded charter airport pair, flights are down 15% compared to last year.

North America branded charter bizjets ranked by departures, January 1st � 30th 2023, compared to previous years.

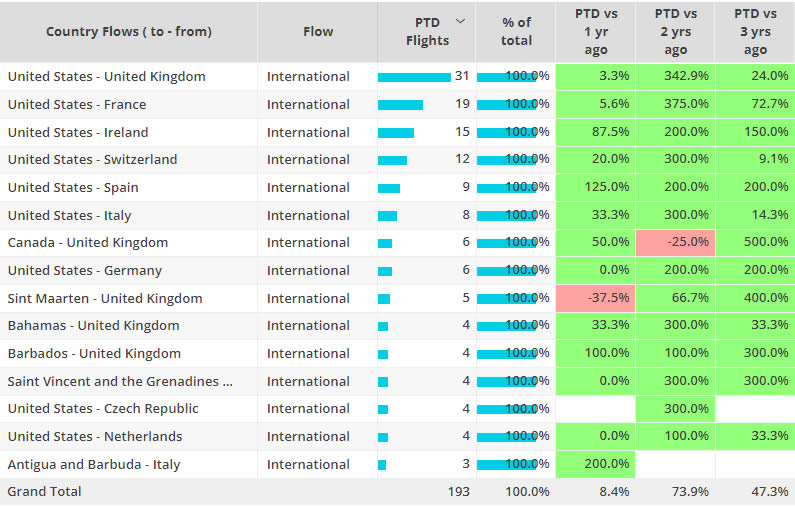

Over half of all branded charter flights in North America this month have been under 90 minutes in length, sectors of this length are down 15% compared to last year, 9% above 2019. Long haul flights (6-12 hours in duration) are up 2% compared to last year, 18% above 2019. So far this month there have been almost 200 Trans-Atlantic branded charter bizjet sectors (North America � Europe), 8% more than last year, 57% more than 2019.

As January draws to a close Florida remains the busiest state, although departures are down 6% compared to last year. Demand across other top states is mixed, Texas up 2%, California down 4%, Colorado down 12% compared to last year.

Trans-Atlantic bizjet country flows, Branded Charter, 1st � 30th January compared to previous years.

Europe

30 Days into January business jet flights in Europe are down 7% compared to the same period last year, 6% ahead of January 2019. The erosion of bizjet activity in Russia is contributing significantly to the overall trend; excluding Russia bizjet demand is down 3% compared to last year, 9% ahead of 2019. 65% of bizjet flights this month have been under 90 minutes in length, flights of this duration are down by 1%, 7% above the same period in 2019. Short haul flights, 1.5-3hours are down 15% compared to last year, 7% more than 2019. Ultra-long-haul flights (12+ hours) are up 56% compared to January last year, triple digit growth compared to 2019.

Bizjet activity across the top markets is mixed this month, France the busiest market, although sectors are down 3% compared to last year. Activity in the UK is on par with last year, Germany slightly down. Spain is seeing 11% decline compared to January 2022, departures out of Russia are 74% below January last year.

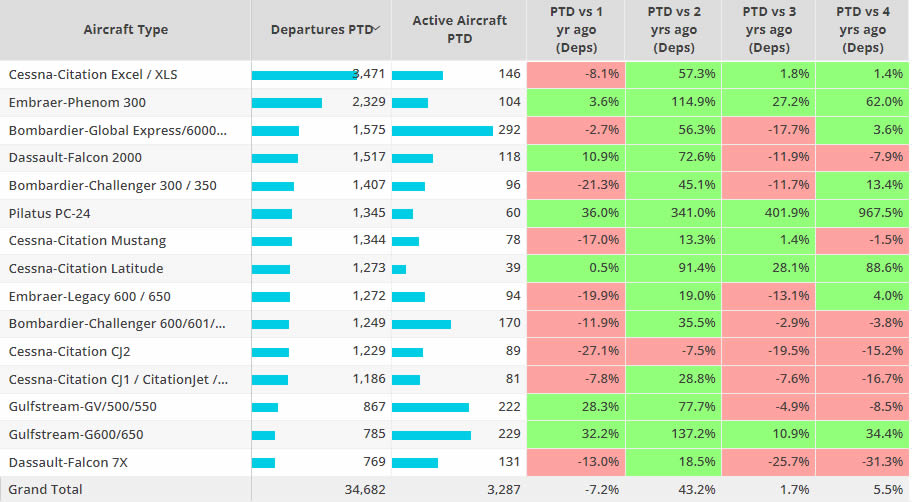

The Cessna Citation Excel / XLS is the busiest bizjet model so far this month, although flights are down 8% compared to last year. Long-range jets have been more active this month compared to 2019. The Bombardier Global Express / 6000 series has been the most active aircraft model this month, 4% more than 2019, there have been 34% more Gulfstream G600/650 aircraft active compared to 2019.

Business jet aircraft ranked by departures, Europe 1st � 30th January 2023 compared to previous years.

Rest of World

Outside of North America and Europe, bizjet activity is trending 31% above comparable January 2022, 85% above 2019. Brazil is the busiest ROW market for bizjets, sectors are up 20% compared to last year, India up by triple figures compared to last year, Australia up 22%. Activity out of China is up 29% compared to last year. Almost 80% of bizjet flights in China are domestic. International flights are seeing triple digit growth compared to last year and versus 2021, still down 39% compared to 2019.