WINGX�s weekly Business Aviation Bulletin.

Summary

There is always significantly less flying during the Easter holidays and as that came earlier this year, the trends are suppressed compared to 2022 and 2019. That said, the deficits compared to 2022 are widening as we move into Q2-2023. This reflects a weakening economic environment and sensitivity to the cost of flying private.

Global

Global bizjet sectors in Week 14, April 3rd through April 9th, amounted to 65,681 sectors, 5% fewer than the previous week, 16% fewer than the week last year. European bizjet activity this month is actually below 2019 levels, but this is largely due to an earlier Easter holiday this year. In the last 4 weeks the global trend for business jet activity has been at 10% below the same dates in 2022. In the last four weeks worldwide charter and fractional activity is trending 15% behind the same dates in 2022, but still up 24% vs comparable 2019. Scheduled airline activity continues to recover but still trends 16% below April 2019.

Chart 1: Global fixed wing flights, April 1st – 10th 2023 compared to previous years. (Note business aviation includes turboprops)

North America

In Week 14, North American bizjet sectors amounted to 51,772 sectors, 5% fewer than Week 13, 18% fewer than the same dates in 2022. In the last four weeks the trend has been 12% below the same dates in 2022. In Week 14 Part 135 and 91k sectors were 1% above Week 13, 18% below the same dates in 2022. 91% of all business jet departures in the region are from the United States, US sectors are 15% below last year, 13% ahead of 2019.

Teterboro is the busiest bizjet airport in North America through the first 10 days of April, activity 13% below last April, still 7% below April 2019. Private flight departments are flying 18% more out of Teterboro than they were in 2019 but have come down to 4% more compared to April last year. Corporate flight departments are flying 36% fewer flights than in April 2019, 29% fewer than 2022 out of Teterboro.

�

Demand across the top bizjet operators in North America this month is mixed. NetJets are flying 2% fewer sectors than April 2022, 30% more than April 2019. Flexjet and Jet Edge are seeing triple digit growth compared to April 2019, Wheels Up Private Jets flying 5% fewer flights than 2019. Year to Date (Jan 1st � April 10th), Net Jets is flying 5% more sectors than comparable 2022, FlexJet 11% more than 2022.

Chart 2: North American bizjet flights by operator, April 1st � 10th 2023 compared to previous years.

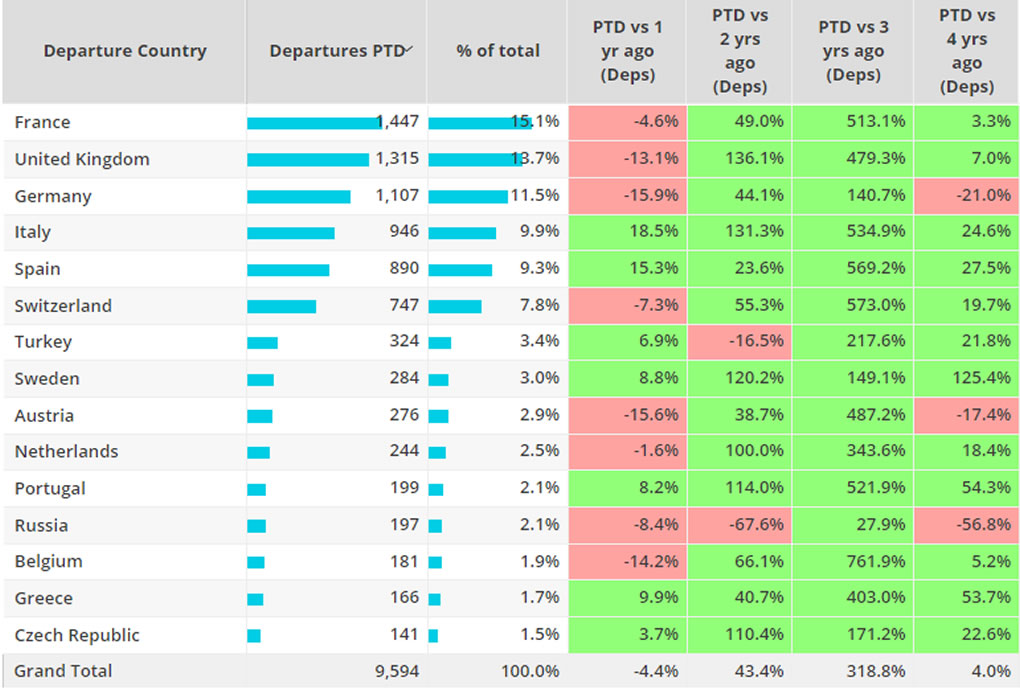

Europe

In Week 14 there were 8,880 bizjet departures from Europe, 8% fewer than Week 13, 15% fewer than the same dates in 2022. In the last 4 weeks the trend has been 7% below the same dates in 2022. The downwards trends has clearly been exaggerated by the much earlier Easter holidays this year compared to 2019 and 2022.

In the first 7 days of April European bizjet departures were down 4% compared to last year, 4% ahead of 2019. France was the top market, sectors down 5% compared to the same dates in 2022, 3% ahead of 2019. The United Kingdom and Germany complete the top 3 markets, both seeing declines compared to last year. Departures from Le Bourget are 10% below comparable 2022, 12% ahead of 2019. Nice was the only airport in the top 5 to see bizjet departures above last year.

Chart 3: Top European Business Jet Markets, April 1st � 7th 2023 compared to previous years

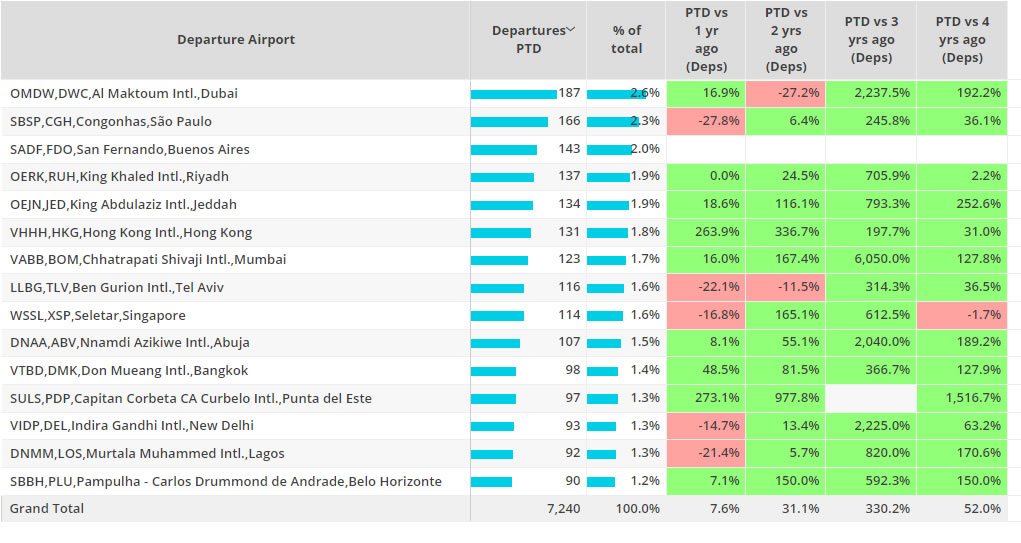

Rest of World

In Week 14 bizjet departures in Africa were 9% below the same dates in 2022, Asia up 19%, South America down 3%, Middle East up 5%. Excluding North America and Europe, bizjet activity in the Rest of World region is 8% ahead of the same dates in April 2022, 52% ahead of 2019. Brazil the top market this month has seen activity drop 4% compared to last year, although 94% ahead of 2019. Australia is also down compared to last year, India on par with last year.

China is seeing triple digit growth compared to April last year, reflecting the release of lockdown measures during Q1 2023. The recovery is still coming through; April 2023 business jet activity is still 13% down on comparable April 2019. Ultra-long-range jets remain the busiest aircraft segment in China this month, triple digit growth in sectors flown compared to last year, although 30% fewer than 2019. Beijing Capital is the busiest bizjet departure airport this month.

Chart 4: Top ROW airports, bizjets, 1st � 10th April 2022 vs previous years.