WINGX�s weekly Business Aviation Bulletin.

Summary

Trends in global business aviation activity are holding up pretty well through the summer compared to summer last year. In the Middle East, the trend compared to pre pandemic is close to 30%, in North America, 15%, and in Europe, 8%. Fractional operators have retained the strongest growth since the pandemic, with Private flight departments still well up in the US.

Global

20 days into August, global business jet and turboprop sectors fell 3% compared to the period last year, still 14% ahead of August 4 years ago. Comparatively, Scheduled Airline activity is 16% ahead of last year, 5% short of August 2019. The top 5 commercial airlines (Southwest, American, Delta, Ryanair & United Airlines) are flying 12% ahead of August 2022, 8% ahead of 2019. Global cargo activity is 7% down on last year, 2% up on 2019.

Focussing on just business jet activity, global sectors are 4% behind August last year, although 18% ahead of 2019. Just under a quarter of global bizjet flights are international flights, these flights are down 5% compared to last year, 13% ahead of 2019. Domestic flights are 19% ahead of August 2019, 3% ahead of last year.

Chart 1: Global fixed wing flights by sector, August 2023 compared to previous years. (Note business aviation includes turboprops)

Europe

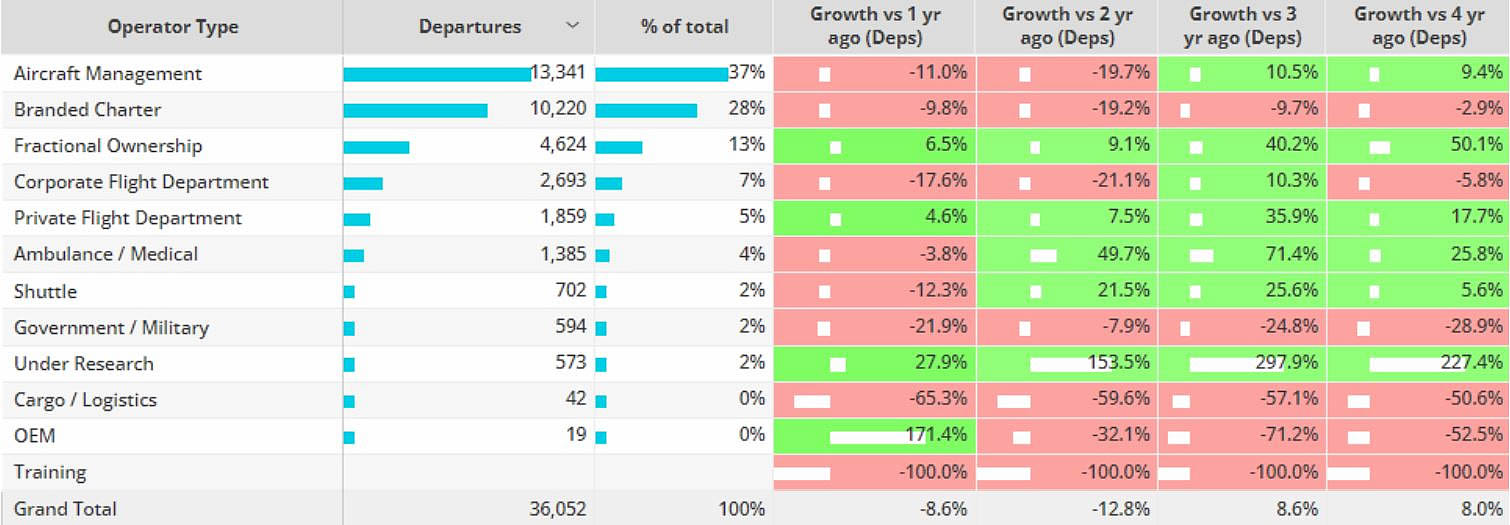

In Week 33 (ending August 20th) business jet activity in Europe was on par with Week 32, 10% below the same dates last year. These trends are slightly behind the last 4 weeks activity, 9% behind comparable 2022. So far this month activity is 9% behind last year, although 8% ahead of 2019. YTD (1st January – 20th August), European bizjet activity has dropped 9% below last year, 8% ahead of 2019. France is the busiest market, followed by the United Kingdom, both markets down 9% and 11% compared to YTD 2022 respectively. YTD Germany and Austria are 2% and 4% below 2019 respectively. Activity across the operator types in Europe is mixed this month. Aircraft management programmes are flying the most, departures 11% below last year, 9% ahead of 2019. Branded Charter sectors have fallen 10% below last year, 3% below 2019. Fractional fleets are flying more than last year, corporate flight departments seeing double digit declines compared to last August.

Chart 2: European business jet operator types, August 2023 compared to previous years

North America

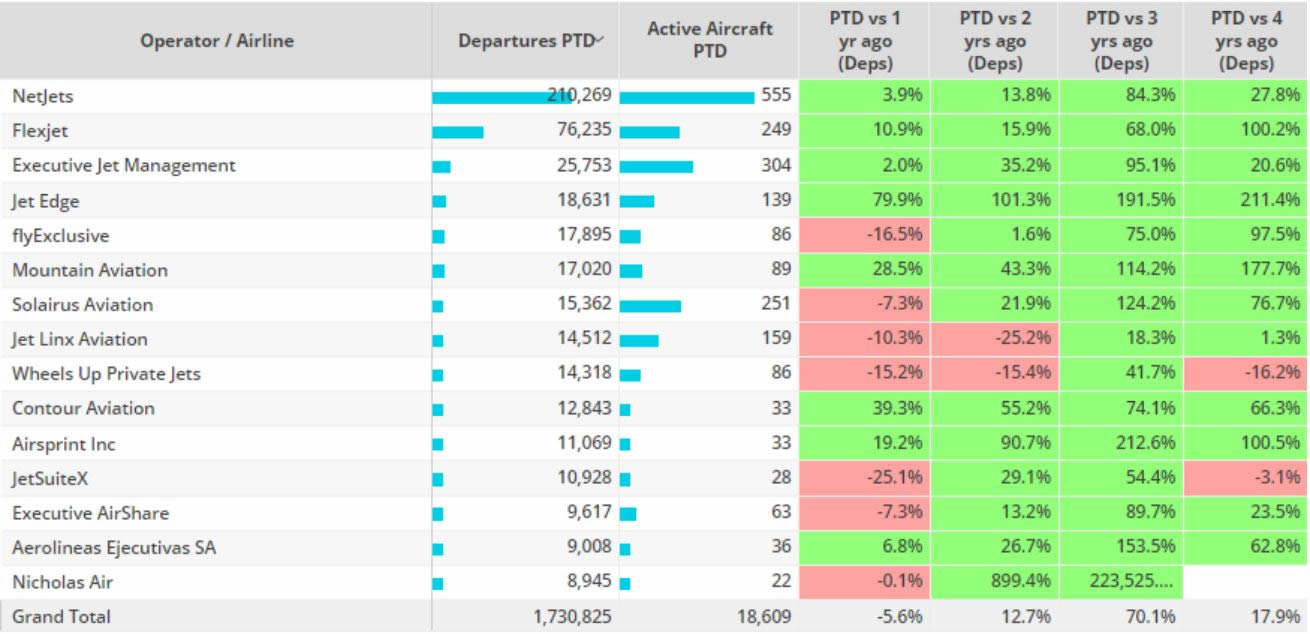

In Week 33 (ending 20th August), business jet activity across North America was on par with the previous week, fell 3% below the same dates in 2022. Year � to date (1st January � 20th August) North America business jet activity is 6% behind last year, 18% ahead of 2019. There have been almost 1.6 million departures from the United States, 6% fewer than the previous year, 17% ahead of 2019. Elsewhere Mexico and Canada seeing double digit growth compared to YTD 2019, both 3% ahead of 2022. So far in August North America business jet departures are 4% below August 2022, 16% ahead of 2019. 92% of flights in the region are domestic, domestic flights down 4% compared to August 2022, 16% ahead of 2019. International bizjet flights have fallen 2% compared to last year, 14% ahead of 2019.

Chart 3: Top bizjet operators, North America, 1st January � 20th August 2023

Asia

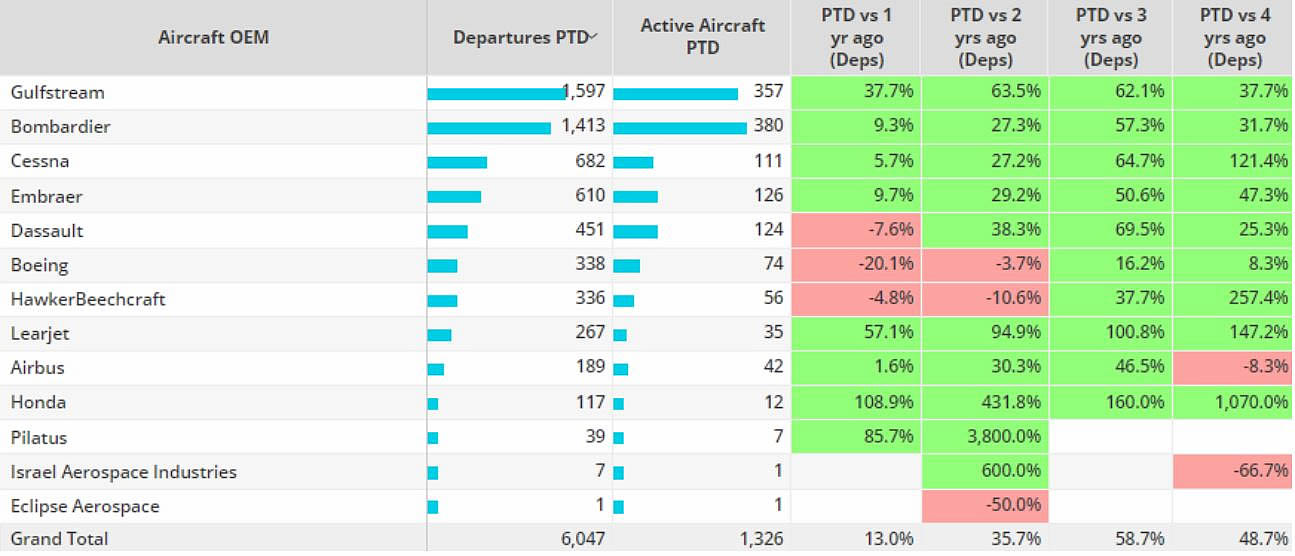

So far this month, business jet activity in Asia is 13% ahead of last year, 49% ahead of 2019. India remains the top market, departures 8% ahead of last year, triple digit growth vs 2019. Second ranked China is well ahead of last year, triple digit growth, double digit growth vs 2019. Gulfstream aircraft are flying the most this month in the region, activity 38% ahead of August 2022 and 2019. Dassault, Boeing and Hawker Beechcraft fleets down on last year, Airbus fleets down on 2019.

Chart 4: Asia Business Jet Aircraft OEMs, August 2023 compared to previous years.

Middle East

Bizjet activity in the Middle East has fallen 3% behind August last year, although still 30% ahead of 2019. Turkey is the busiest market in the region this month, activity 6% ahead of last year, double digit growth vs 2019. Just over 1,000 domestic bizjet flights have been flown in Turkey, 8% more than last August. Turkey � Greece is the busiest international connection in the region, flights up 15% compared to last year, 56% ahead of 2019.

Chart 5: Middle East Country flows, August 2023 compared to previous years.