WINGX�s weekly Business Aviation Bulletin.

Summary

This week´s year-on-year trend is flattered by the Labor Day dates, so the best guide to the key US market is the 4-week slide of 4% compared to last year. Europe is unaffected by the holiday blip, with the latest week 36 showing a widening deficit versus last year, with bizjet activity in Germany slipping almost 10% below 2019 levels.

Global

So far this month (1st – 10th September), business jet and turboprop sectors have fallen 4% compared to September last year, 19% ahead of 2019. Scheduled airline sectors have increased 15% compared to last year, 5% behind 2019. The top 5 commercial airlines (Southwest, American, Delta, Ryanair & United Airlines) are flying 7% ahead of last year, 12% ahead of 2019. Global cargo sectors have fallen 13% compared to the start of September last year, just 1% ahead of comparable 2019.

Chart 1: Global fixed wing flights by sector, September 2023 (Note bizav includes turboprops).

Europe

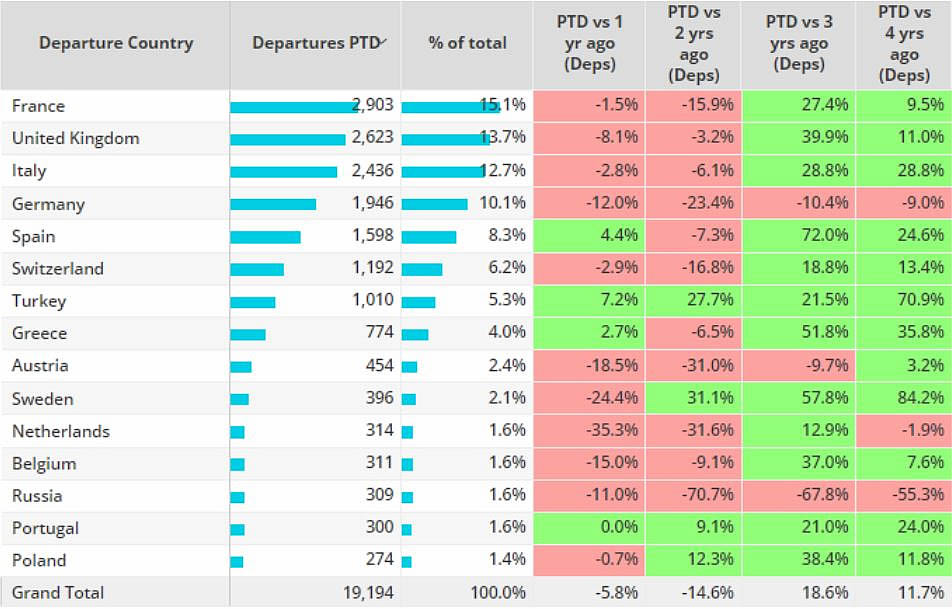

In Week 36, ending 10th September, business jet sectors fell 6% compared to the previous week, 8% behind the same dates in 2022. Month-to-date bizjet activity (1st � 10th September) is 6% behind last year in Europe, still 12% ahead of four years ago. Demand across the top markets is mixed. France the busiest market so far this month, departures 2% behind last year. Germany has seen bizjet departures fall 12% compared to September 2022, 9% behind September 2019. Elsewhere Portugal is on par with last year, Spain 4% ahead of last year, contrast United Kingdom 8% behind last year.

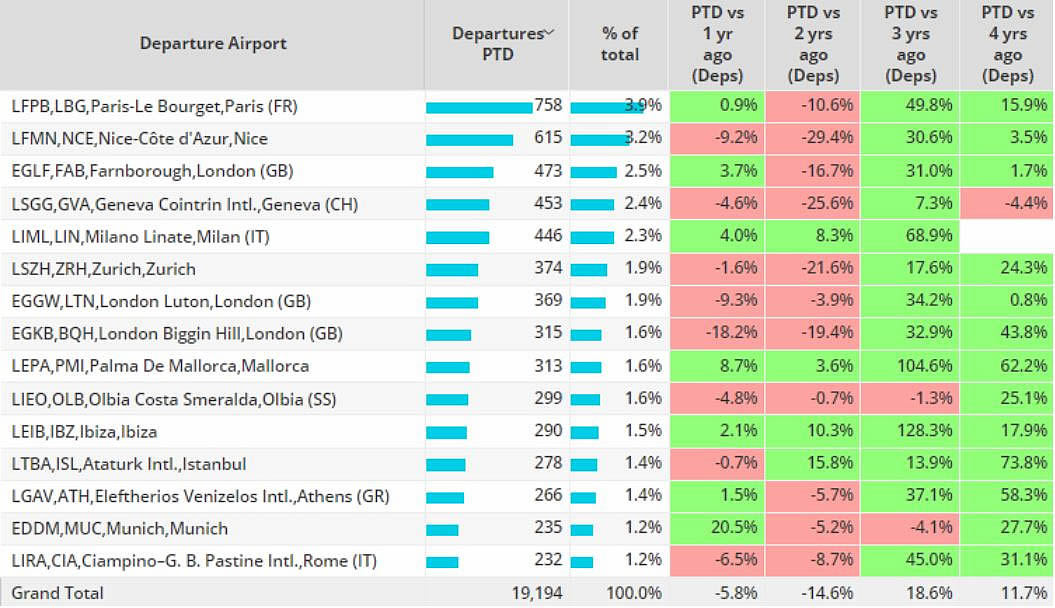

Le Bourget is the busiest airport this month, departures 1% ahead of September 2022, 16% ahead of 2019. Contrast Nice, departures 9% behind last year, Luton also 9% behind last year. Departures from Geneva have fallen 4% behind September 2019.

Chart 2: European business jet airports, September 2023 compared to previous years.

Chart 3: European bizjet activity by countries, September 2023 compared to previous years.

North America

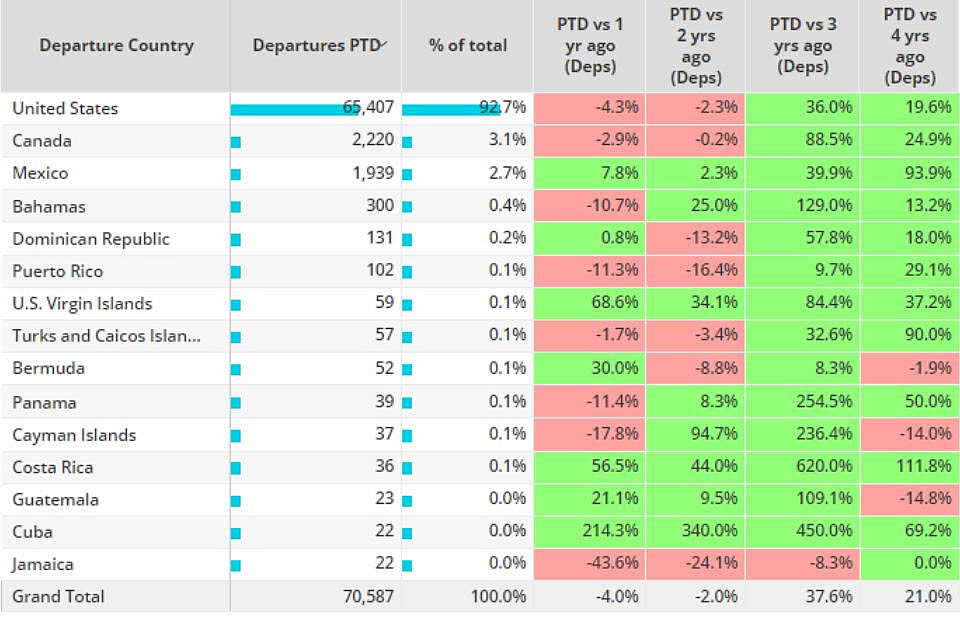

Business jet sectors in Week 36 grew 13% compared to the previous week, 3% ahead of the same dates in 2022. North American business jet activity has fallen 4% compared to September 2022, 21% ahead of 2019. Slower YOY start to the month for the US and Canada, departures 4% and 3% respectively behind last year, contrast Mexico which is 8% ahead of last year. Bizjet departures from Teterboro, the busiest airport in the region, have fallen 6% behind last year, 8% below 2019. Las Vegas McCarran is 12% behind last year, Washington Dulles -12%, Westchester County -7% compared to last year. Van Nuys and Palm Beach 1% and 4% ahead respectively.

Chart 4: North America Business Jet activity September 2023 compared to previous years.

Asia

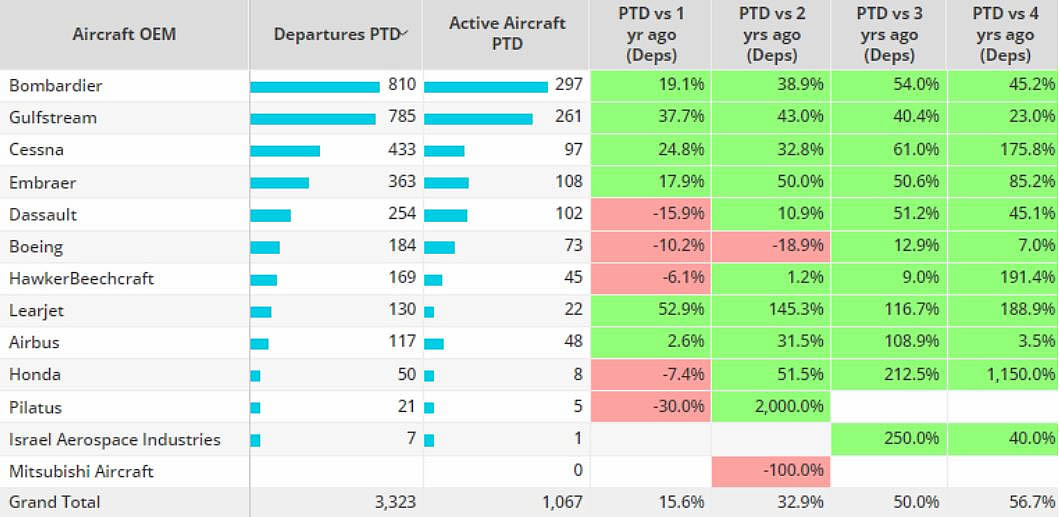

In Asia business jet activity is 16% ahead of September 2022, 57% ahead of 2019. India, the busiest market this month is 21% ahead of last year, triple digit growth compared to 2019. Second ranked China is now seeing more activity than in 2019. Almost 300 active aircraft this month make Bombardier the busiest OEM in the Asia region in terms of activity and active aircraft. Dassault and Boeing VIP fleets have seen activity drop double digit figures compared to September 2022, Cessna types triple digit growth vs 2019.

Chart 5: Business Jet OEMs, Asia, September 2023.

Middle East

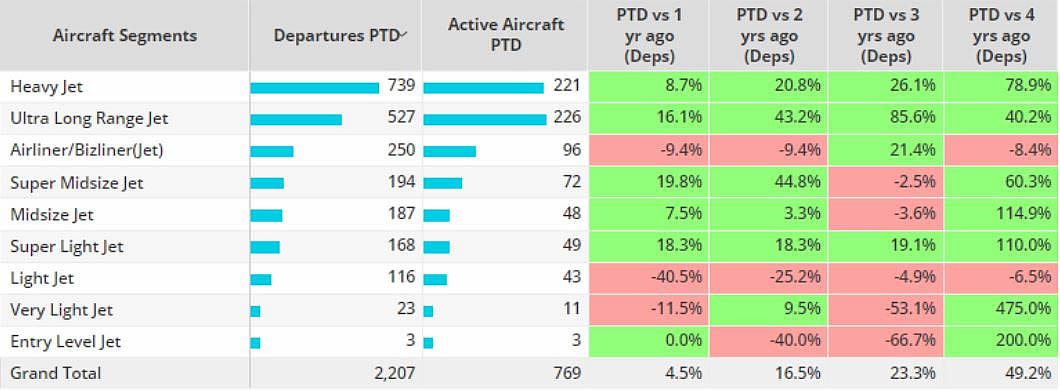

Business jet activity in the Middle East is 5% ahead last year, still 49% ahead of 2019. Israel and Cyprus buck the regional trend, departures down 6% and 15% respectively. Elsewhere, Saudi Arabia and United Arab Emirates have started September well ahead of last year, +16% and +5% respectively, both double digit growth compared to 2019. Heavy and Ultra Long Range jets have flown more than half all sectors this month, more active than last September. Bizliners are flying 9% fewer flights than 2022, 8% fewer than September 2019. Very Light Jet and Light Jet departures also behind last year.

Chart 6: Business Jet aircraft segments, Middle East, September 2023