WINGX's weekly Business Aviation Bulletin for 16th November, 2023

Overall

Economic stagnation and geopolitical turbulence has stalled bizjet usage in Europe and Middle East. The powerhouse US market is holding up, lopsided towards large cabin aircraft demand.

Global

Twelve days into November, business jet and turboprop activity is on par with last year, 19% ahead of 2019. Business jets are down 1% compared to last November, 19% ahead of four years ago. So far this year business jet and turboprop activity is 3% behind comparable last year, still 16% ahead of four years ago. Focusing on just business jet flights, there have been 3,100,000 sectors flown globally so far this year, 4% fewer than comparable last year, 19% ahead of four years ago. Year-to-date scheduled airline sectors are 16% ahead of last year, 10% behind 2019. Year-to-date dedicated cargo sectors are 6% behind 2022, 1% ahead of 2019.

Chart 1: Global fixed wing flights by sector, 1st January – 12th November 2023 (Note business aviation includes turboprops)

Europe

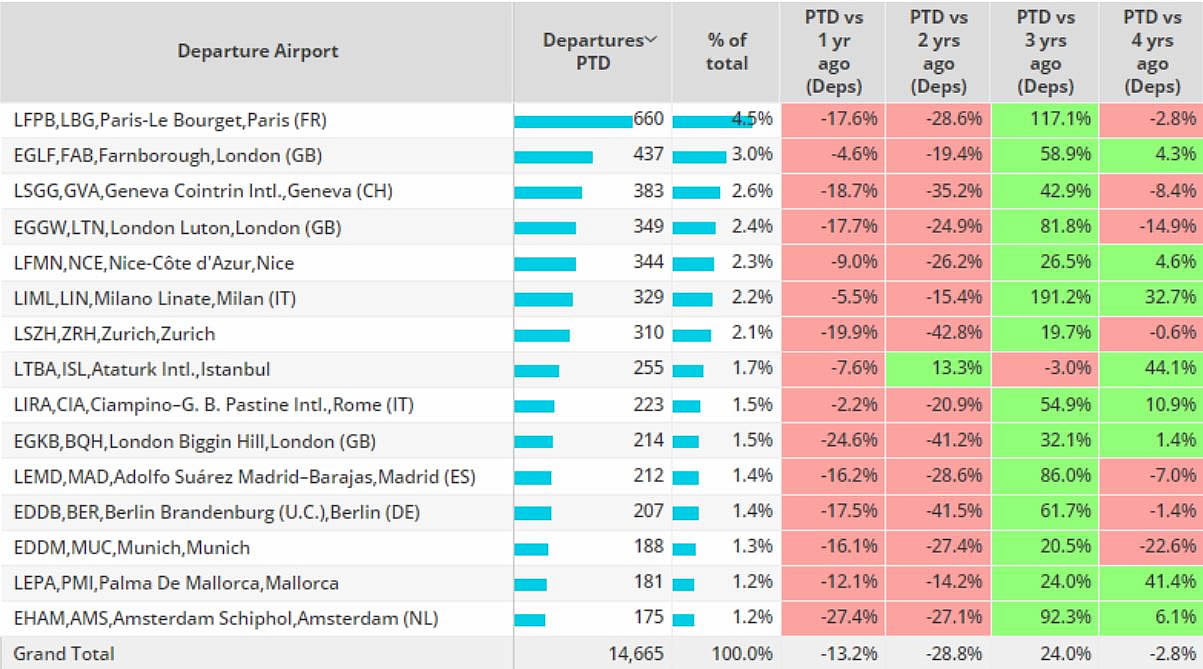

Twelve days into November, business jet activity in Europe is 13% behind the same dates last year, 3% behind comparable 2019. All major bizjet airports in Europe are seeing fewer activity this month compared to last year. Several airports are even behind November four years ago, namely Le Bourget, Geneva and London Luton.

61% of bizjet flights in Europe this month have been under 90 minutes in length, flights of this duration down 15% compared to last year, 6% below 2019. Long haul flights (6-12hours) are ahead of last year by 6%, ultra long haul (12+ hours) are down 38% compared to comparable 2022, 11% ahead of 2019.

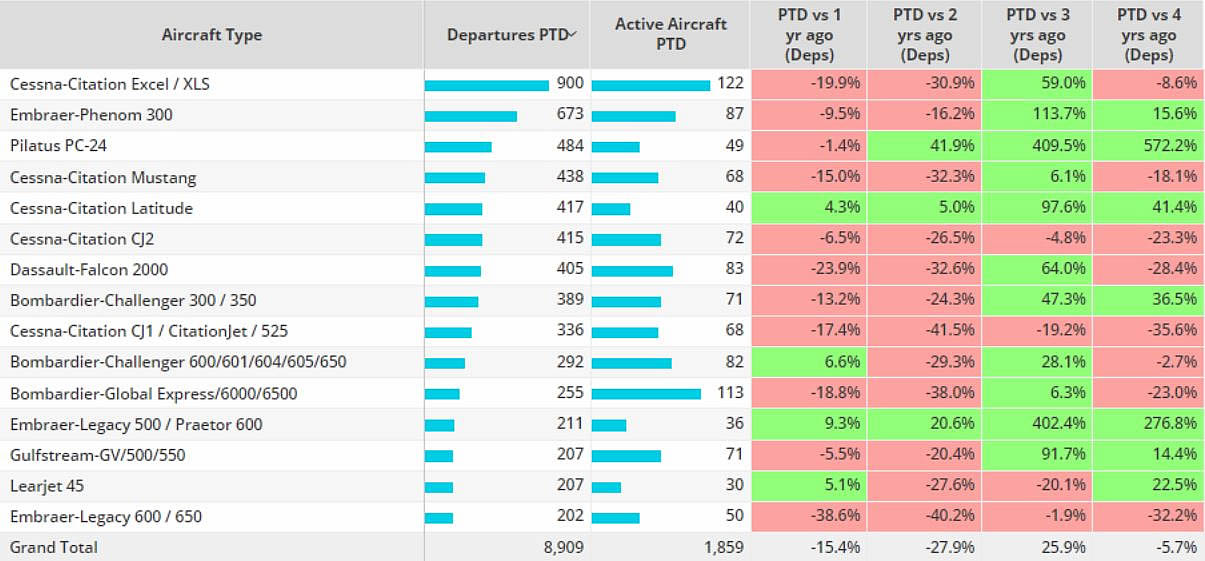

The Cessna Citation Excel has flown the most flights under 1.5 hours across Europe this month, although 20% less sectors than last year, 9% below 2019. Contrast the Citation Latitude, flying more flights under 1.5 hours than any November in the last four years.

Chart 2: Top Business Jet airports, Europe, 1st � 12th November 2023 compared to previous years

Chart 3: Business Jet aircraft types on flights under 1.5 hours, Europe, 1st � 12th November 2023 compared to previous years.

North America

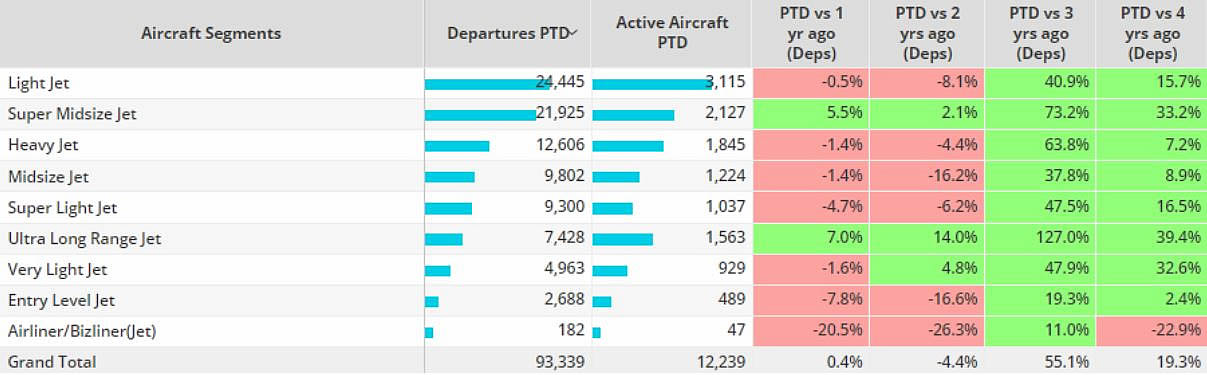

Week 45, ending November 12th, saw business jet activity rebound 6% compared to the previous week, 3% ahead of the same dates in 2022. So far this month, activity across the region is on par with last year, 19% ahead of 2019. Super Midsize and Ultra Long-Range Jets are flying more than any comparable November in the last four years. Bizliner activity is stalling, still 21% behind last year, 23% down on pre-pandemic 2019.

Chart 4: North America business jet aircraft segments, 1st � 12th November 2023 vs previous years.

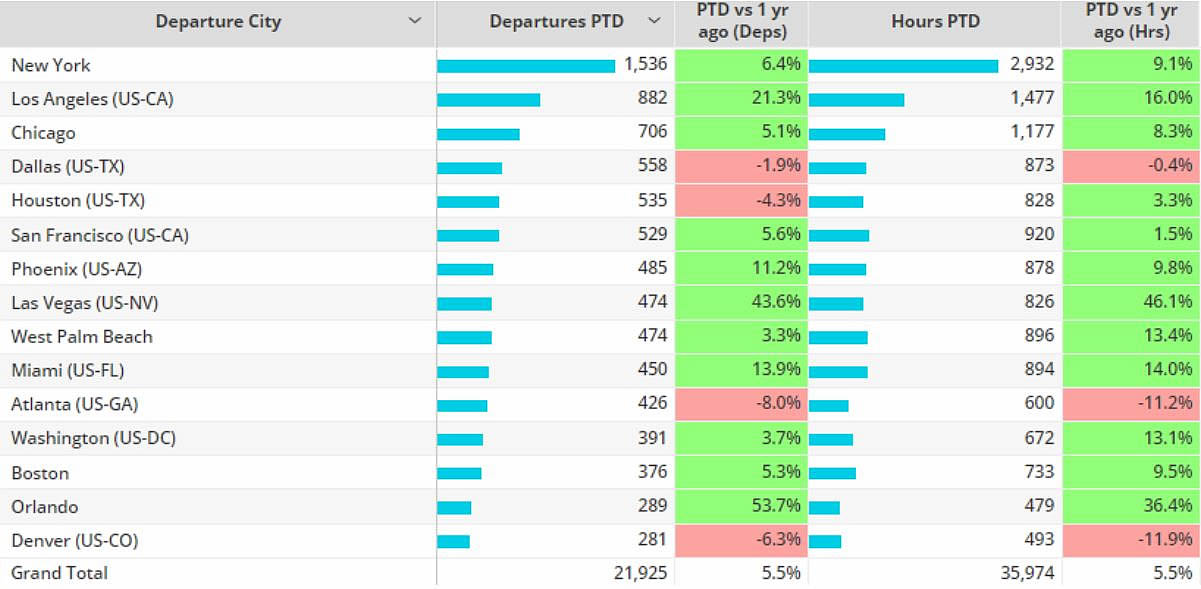

Teterboro is the busiest departure point for Super Midsize aircraft types, sectors up 6% compared to last year, 14% ahead of 2019. New York is the top metro area for Super Midsize aircraft, sectors are 6% ahead of last year, hours 9% ahead of last year. California � Nevada is the busiest Super Midsize cross state flow, activity 50% ahead of comparable last year.

Chart 5: Super Midsize Metro Areas, North America, 1st � 12th November 2023 compared to previous years.

Asia

In Asia the market is 5% ahead of comparable November last year, 50% ahead of 2019. Aircraft management fleets are flying the most, 1576 flights so far this month, 3% fewer than last year, 33% more than 2019. Branded Charter fleets are flying 5% fewer than last year, 46% ahead of four years ago, Corporate flight departments ahead of every November in the last four years.

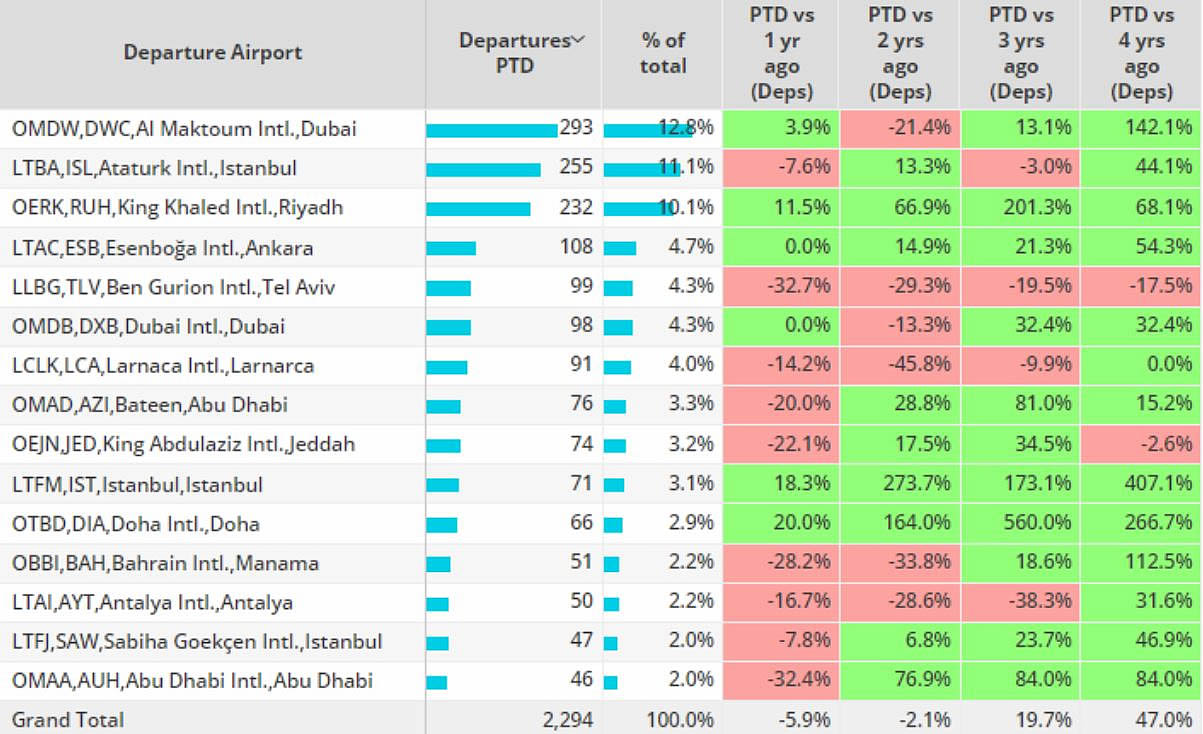

Middle East

So far this month bizjet activity in the Middle East is 6% behind last year, although 47% ahead of 2019. Top airport Al Maktoum Intl is soaring ahead of comparable 2019, 4% ahead of last year. Elsewhere Doha Intl is seeing large gains compared to 2019, 20% ahead of last year. 99 Departures this month from Ben Gurion Intl, 33% fewer than last November.

Chart 6: Middle East business jet activity by airport, 1st � 12th November 2023.