WINGX's weekly Business Aviation Bulletin for 23th November, 2023

Overall

Global bizjet activity is exceeding last year’s November activity, still 1% behind November 2021, but almost 20% ahead of November 2019. Much of the lift is coming from strong demand in the US. European demand is wilting and Middle East has tapered from last year�s heights.

Global

Business jet and turboprop sectors are 1% ahead of comparable November 2022, 20% ahead compared to four years ago. Focusing solely on business jets, 192,000 sectors have been flown 19 days into November, on par with last year, 22% ahead of four years ago. Year to date, global bizjet activity is down by 4% YTD compared to 2022, and 19% ahead compared to 2019. Scheduled airline activity trails November 2019 by 9%, 15% ahead of November last year. Dedicated cargo sectors are down 8% compared to November last year, although 5% ahead of 4 years ago.

Chart 1: Global fixed wing flights by sector, 1st – 19th November 2023 (Note business aviation includes turboprops)

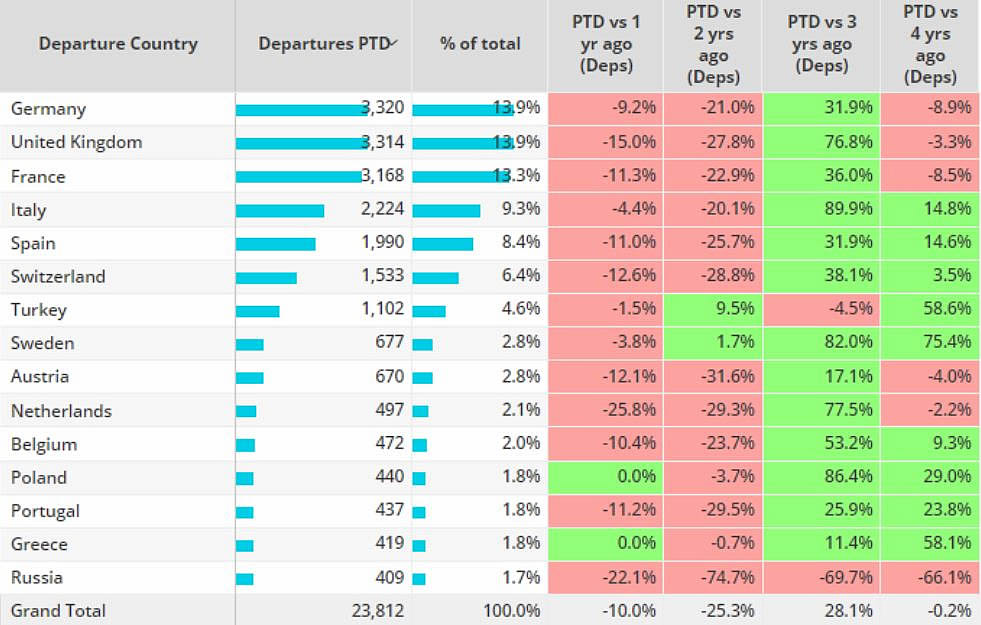

Europe

Nineteen days into November, European business jet activity is 10% behind the same dates last year, 0.2% behind November four years ago. Germany, United Kingdon and France are the top 3 markets, all seeing activity drop below 2019. 10 of the busiest markets are weighing regional activity down, all seeing activity drop below last year. Poland and Greece buck the regional trend, activity on par with last year.

Despite the overall market declines, fractional and private fleets are flying more than any November in the last 4 years. Contrast Corporate flight department�s, activity has fallen 23% compared to November last year, 27% behind four years ago. Paris � London is the busiest international metro connection for European fractional fleets, 41 bizjet flights so far this month. The Cirrus-SF-50 Vision has operated the most flights this month within private flight departments.

Chart 2: Top Business Jet countries Europe, 1st � 19th November 2023 compared to previous years.

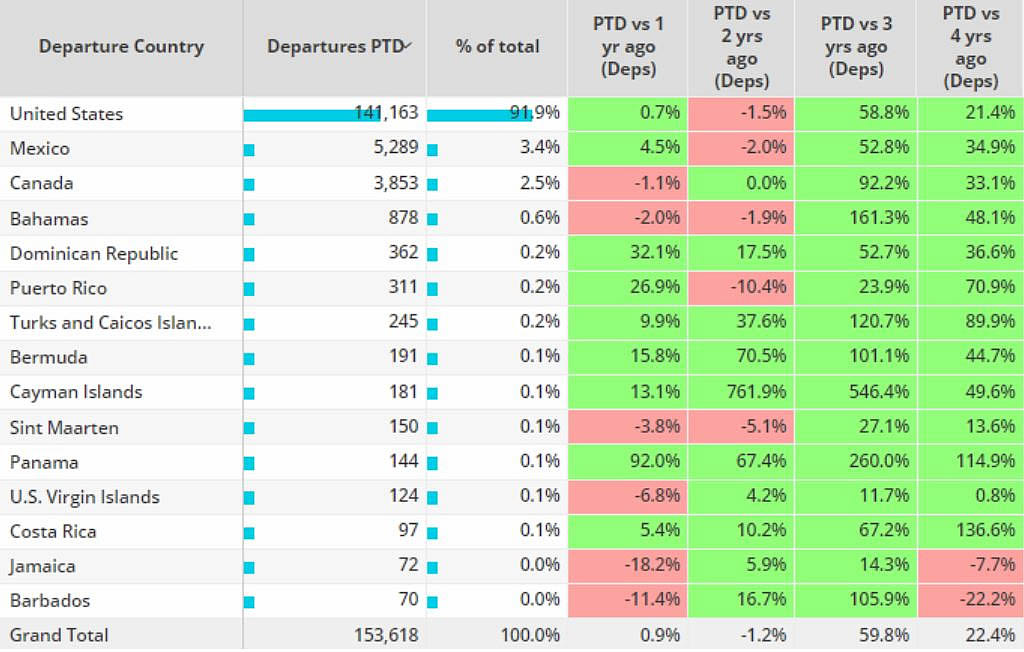

North America

So far this month North American business jet activity is 1% above comparable last year, 22% ahead of four years ago. Departures from the US accounted for 92% of regional business jet activity, with flights up 1% compared to last year, up 21% vs October 4 years ago. There has been strong growth in the Caribbean, whereas Canada and Bahamas are seeing slightly less YOY activity.

Chart 3: North America business jet countries, 1st � 19th November 2023 vs previous years.

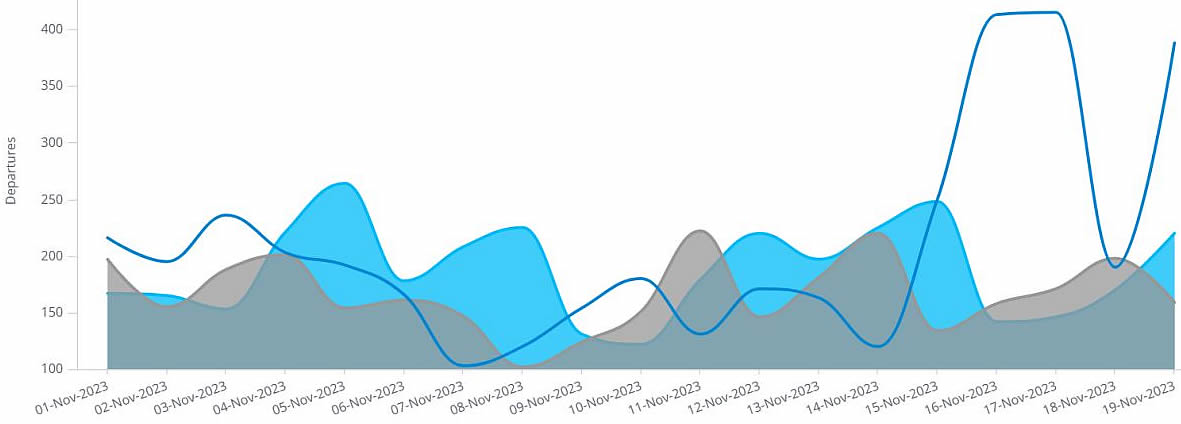

Over the weekend (17th � 19th November), Las Vegas hosted the F1 Grand Prix. There were 927 bizjet arrivals into Las Vegas airports during the Grand Prix weekend (17th � 19th), with most of the traffic coming from California. Van Nuys saw 131 bizjet departures bound for Las Vegas airports, 67% of all inbound flights to Las Vegas airports over the GP weekend flew less than 90 minutes. Fractional operators worked hard during the GP weekend, accounting for a third of all arrivals into Las Vegas airports.

Chart 4: Bizjet activity at Las Vegas airports during Grand Prix

Asia

Through the 19th November, bizjet activity in Asia is on par with last year, 49% ahead of 2019. Ultra Long-Range Jets flew the most flights this month, more than any other November in the last 4 years. Bizliners, Super Midsize and Super Light aircraft types are also flying more flights than any other November in the last 4 years. The Very Light Jet market has declined 37% in terms of flights compared to last year.

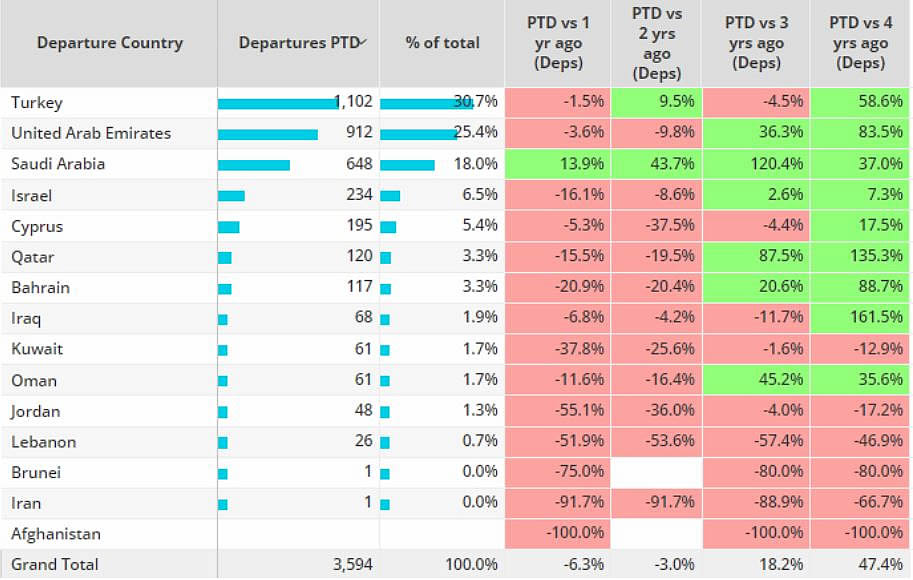

Middle East

Activity in the Middle East this month has fallen 6% compared to last November, 47% ahead of four years ago. Saudi Arabia is an outlier to the regional trend, activity is ahead of any November in the last four years. Most major markets are ahead of 4 years ago, despite declines compared to November 2022.

Chart 5: Middle East business jet activity by country, 1st � 19th November 2023