The 3% drop in flight activity during 2023 compared to 2022 was in line with expectations, representing the market reset which followed the frothy demand during the pandemic era. Demand has petered out in Europe, where the Ukraine war has compounded the effects of economic stagnation. In the US, 17% growth in bizjet traffic since 2019 represents 4% compound annual growth rate, not spectacular but much stronger than the anemic growth in bizjet demand in the previous decade.

Global

5.1 million business jet and turboprop flights were flown in 2023, 3% fewer than 2022, 15% more than during pre-pandemic 2019, representing a compound annual growth rate of 3.4% over the 4 years. Flights recorded from North America and Europe accounted for 92% of global activity, with declines in these regions dampened global trends compared to last year. Business aviation activity is still rising in other regions around the globe, particularly in South America and Africa where recorded flights have more than doubled since 2019. Globally turboprop aircraft flew 1.6 million flights in 2023, busier than any other year previously, whilst business jet traffic was down 4% versus 2022, still 18% ahead of 2019. In December, bizjet activity was 3% lower than in December 2022, 6% lower than December 2021, 16% ahead of December 2019.

Chart 1: Global business jet and turboprop flights, by region, January – December 2023

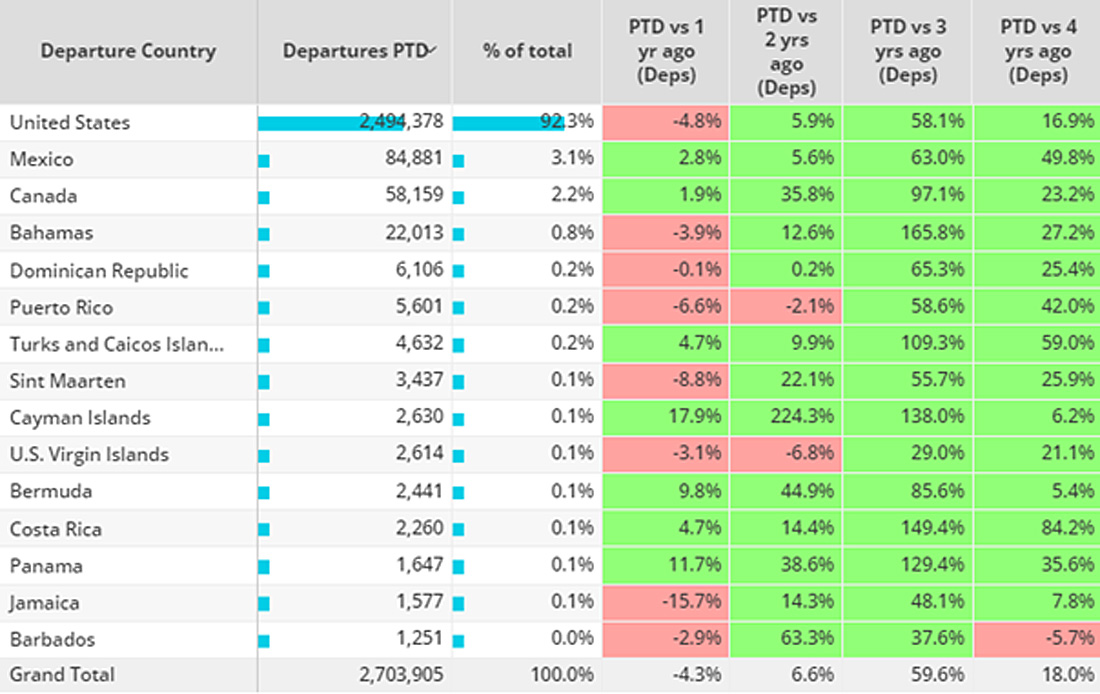

North America

2.7 million business jet flights were flown in North America during 2023, 4% fewer than the full year of 2022 18% more than 2019. Almost a quarter of business jet activity last year came from Corporate Flight departments, although these fleets saw sectors drop 2% behind 2019, and 8% behind last year. Fractional and Private Fleets were busier than ever, 42% and 39% ahead of 2019 levels respectively. With 92% of the region’s share of traffic, US trends were closely aligned with the region as a whole. 2023 saw bizjet activity in Mexico and Canada reach new record levels. Bizjet flights from Costa Rica were up 84% in 2023 vs 2019.

Chart 2: North American business jet markets, 2023 compared to previous years.

Focusing solely on the US bizjet market, 2023 saw new record levels of activity across Bombardier Challenger 300/350, Embraer Phenom 300 and Cessna Citation Latitude jets. As a whole, only the Ultra Long Range jet segment continued fly more in 2023 than in 2022. Florida topped the rankings for the busiest US State in 2023, 38% up on 2019, although 7% fewer flights than in 2022. Notably, California and New Jersey ended 2023 with fairly small, single digit gains compared to 2019. 2023 was the busiest year in the last four years for Teterboro airport, the only major bizjet airport to see growth compared to 2022.

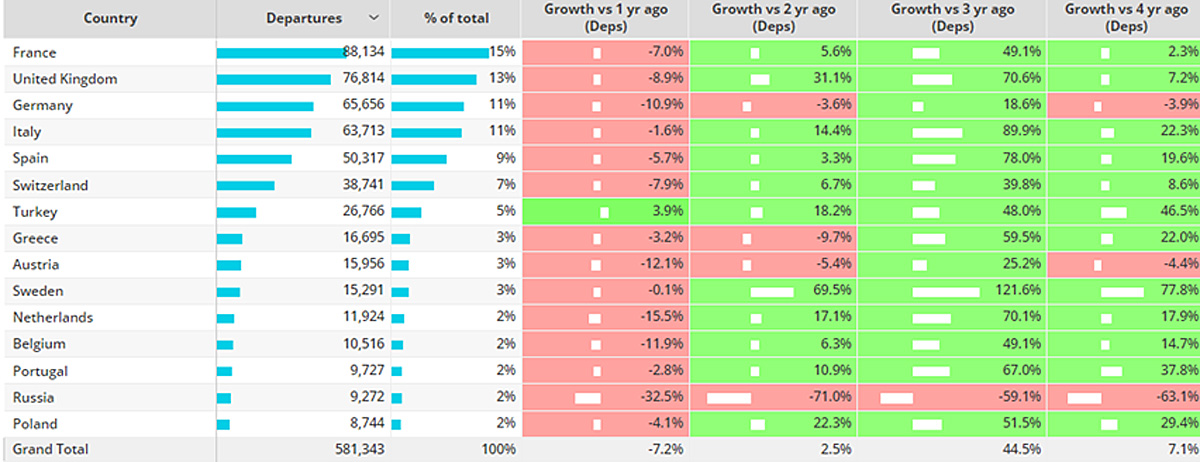

Europe

In Europe, business jet activity in 2023 was more subdued than in North America. Sectors fell 7% behind 2022, chalking up only 7% gains compared to pre-pandemic 2019. Germany was the only top bizjet market to end the year below 2019 levels. Turkey bucked the regional trend, with bizjets flying more than any year in the last 4 years. Bizjet activity in Russia last year was nearly two thirds below 2019, 33% behind 2022. Paris Le-Bourget was the busiest bizjet airport in the region in 2023, activity dipping 9% below 2022, 8% ahead of 2019. Milan Linate and Ciampino saw bizjet activity reach new heights, sectors well ahead of the last four years. London Luton finished the year as the only major bizav airport with declines compared to 2019. All OEM fleets except Pilatus and Cirrus saw some declines in 2023 vs 2022.

Chart 3: Business jet activity by country, 2023 compared to previous years.

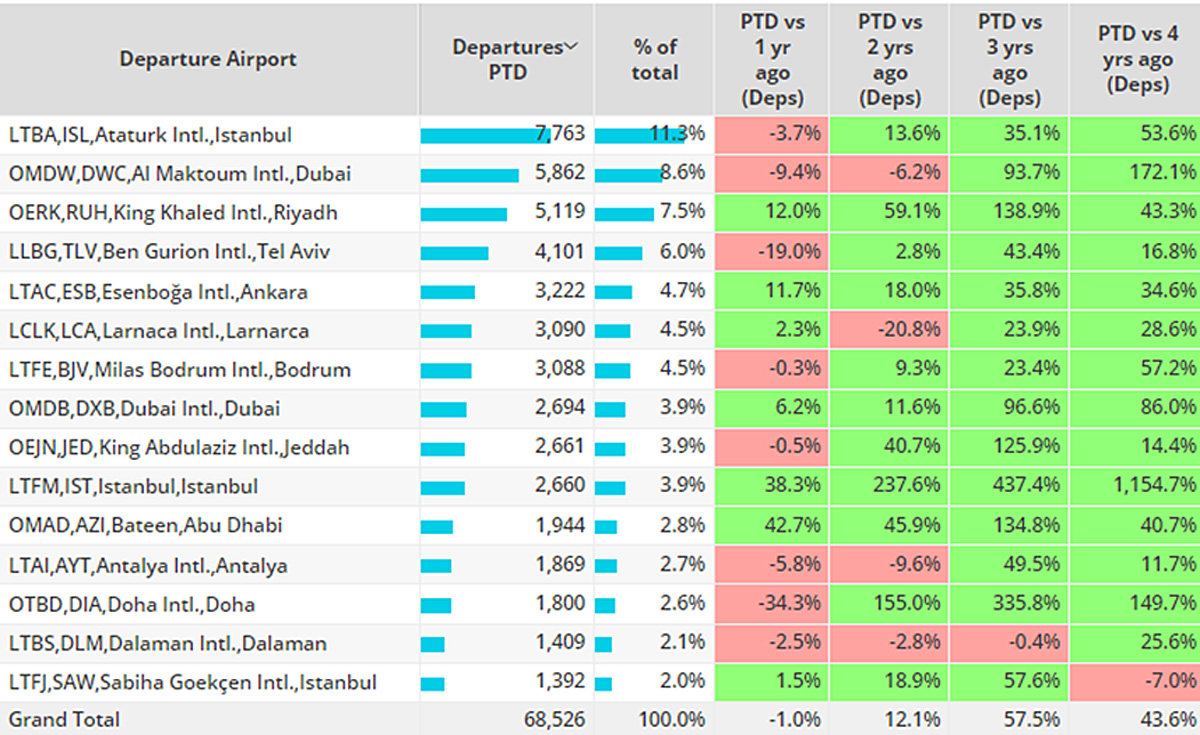

Asia & Middle East

In 2023, bizjet activity in Asia grew 9% compared to 2022, 43% ahead of pre-pandemic 2019. Whilst most aircraft segments were busier than the last four years, bizliners, midsize and light jets were in less demand compared with 2022. In the Middle East bizjet activity dipped slightly, sectors down 1% compared to 2022. Saudi Arabia and Jordan were busier last year than at any point in the last four years, contrast Lebanon where activity fell to its lowest point in the last few years. Despite 90% growth compared to 2019, sectors in the United Arab Emirates fell 2% compared to 2022.

Chart 4: Middle East business jet airport trends, 2023 compared to previous years.