We are seeing the usual drop in bizjet demand following the holidays, with a dent in year-on-year activity due to the severity of the winter storms currently pummelling the US. In Europe, although the 4-week year on year decline is only 2%, the drops in bizjet activity out of Germany and France is eye-catching.

Global

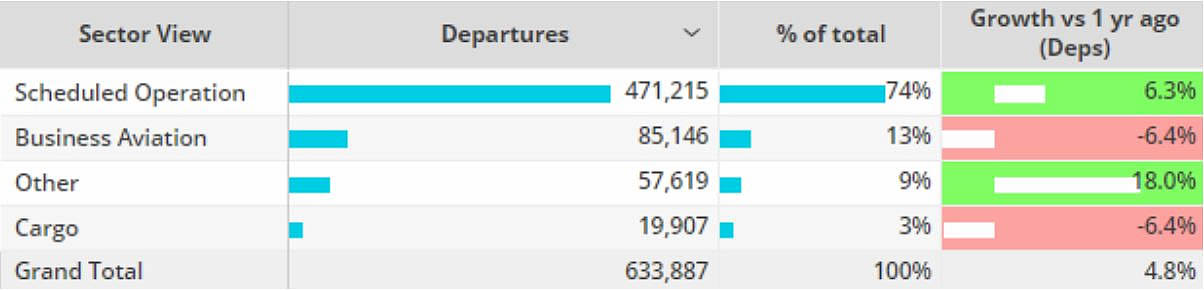

Week 2 of 2024 (January 8th – 14th) saw global business jet traffic drop 9% compared to the previous week, flights falling 7% behind the same dates in January 2023. In the last four weeks, bizjet flight sectors trending down 4% year on year. Following the end of the holiday, and affected by winter storms, Part 135 & Part 91k activity fell back 15% compared to Week 1, comparatively down 4% relative to Week 2 in 2023. Scheduled airline sectors in Week 2 were 6% ahead of the same dates last year, whilst cargo operator sectors were down 6% compared to comparable 2023.

Chart 1: Week 2 2024 activity by sector, compared to 2023.�(Business aviation includes turboprops and business jets)

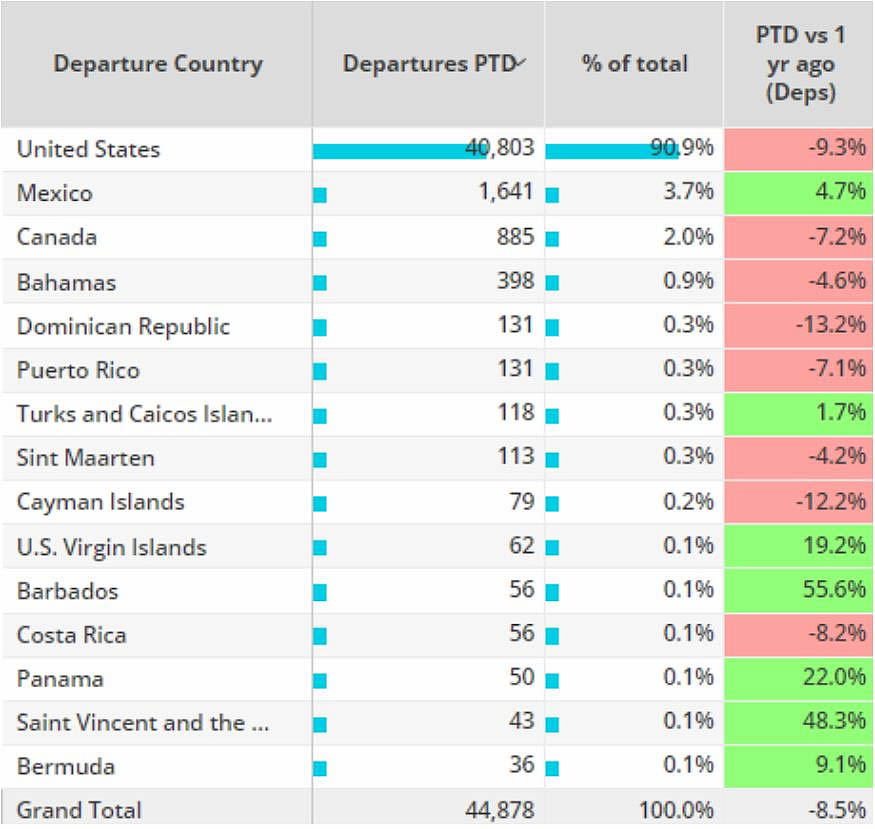

North America

Business jet sectors in Week 2 in North America fell 11% compared to Week 1, largely due to storms that have hit the United States. Across the region activity was mixed, Mexico for example saw Week 2 sectors 5% higher than comparable last year. Canada saw sectors drop 7% compared to the same dates last year, several Caribbean countries also seeing single digit declines compared to 2023.

Chart 2: North American Business jet activity by country Week 2 2024, vs same dates in 2023.�

Focussing solely on the US bizjet market, the winter storms appear to have had most impact in California which saw a 10% drop in year on year operations. Florida saw a 20% fall in bizjet departures compared to Week 1 of 2024, with year on year activity down by 6%. Despite the storms, bizjet activity out of Texas was flat year on year. Top ranked Teteboro was unaffected in Week 2 compared to the previous week, departures on par with W1. The overall year on year bizjet demand in the US may have been affected by this year’s earlier dates for the MLK holiday.

Europe

In Europe, business jet activity in Week 2 of 2024 was up 3% compared to Week 1, down 6% versus the same dates in 2023. In the last 4 weeks bizjets activity is trending 2% down Year-on-Year. Light jets were the busiest aircraft segment in W2, departures surpassing 1,600 flights. Ultra-long-range jets were the most active in W2, just over 500 active unique aircraft during the week. There is a lot of variance geographically, with bizjet out of France down 15% year on year, whereas connections to and from Switzerland were up 6% compared to 2023.

The trend boost in Switzerland is linked to the hosting of the WEF annual general meeting this week (January 15th � 19th, one day earlier than last year), which has already been driving bizjet demand to airports near Davos (LSMD, LSZH, LSZR, LSZS). 103 Bizjet arrivals were recorded on the 14th January, one day before the event, more than double the amount of arrivals recorded on the 13th. There were 140 bizjet arrivals on the opening day (January 15th), 6% more than the opening day of the 2023 event.

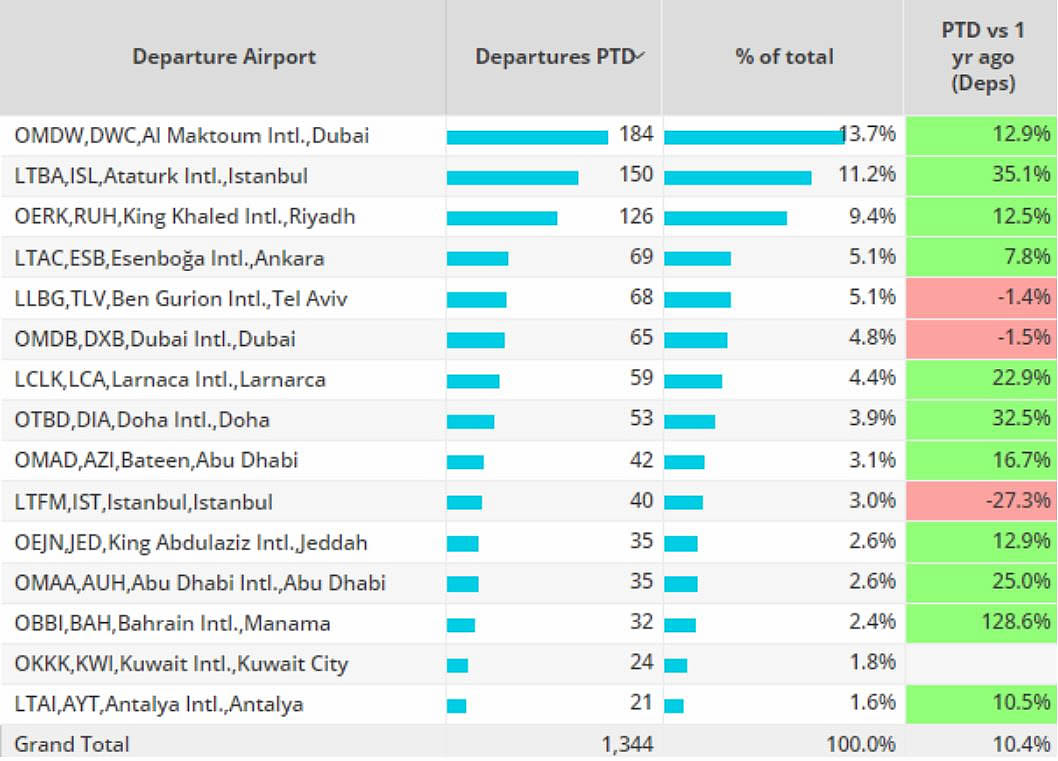

Asia & Middle East

In Asia bizjet activity in Week 2 of 2024 (7th � 14th January) rebounded 4% compared to Week 1, 2% ahead of the same dates in 2023. In the Middle East, bizjet sectors grew 15% compared to last week, 10% ahead of the same dates in 2023. Strong demand for bizjets continues in Saudi Arabia and the United Arab Emirates, sectors 4% and 12% ahead of the same dates last year, Al Maktoum and King Khaled both in the top three airports for departures. W2 bizjet activity in Israel fell 18% behind the same dates in 2023. Flights out of Dubai are also falling year on year.

Chart 3: Middle East business jet airports, Week 2 2024 compared to the same dates in 2023.