Year on year, the latest week saw strong growth, keeping 2024 a little ahead of 2023. The US is providing the ballast, with strong growth in South America and Asia, offsetting a slide in European demand.

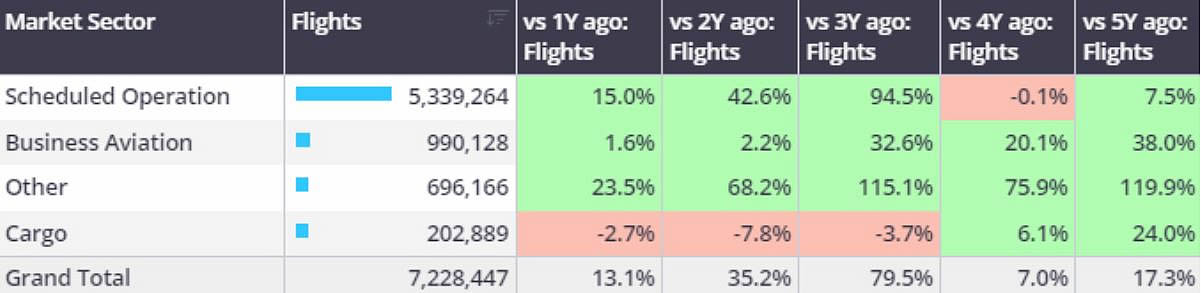

Global

For Week 10, through March 10th, global business jet activity was up 4% YOY compared to Week 10 of 2023. 73,128 business jet sectors were flown last week, 8% more than the previous week. So far this year, 1st January – 10th March, business jet and turboprop activity is 2% ahead of 2023. Business jet sectors and hours in the last four weeks are 5% ahead of comparable 2023, sectors 38% ahead of 2019, hours 42% ahead of 2019. At the start of March, turboprop sectors are 3% ahead of last year, Year to date turboprop sectors are 5% ahead of last year. Cargo sectors starting this month much slower than last year, sectors 11% behind last year, 26% ahead of 2019. In contrast, scheduled airline activity this month is 22% ahead of last year, 9% ahead of 2019.

�Chart 1: 1st January � 10th March activity by sector, compared to previous years.�(Business aviation includes business jets & turboprops)

*WINGX added new sources for global flight data in Feb-24, backdated to Jan-23, which has modestly inflated ROW trends vs 2019.

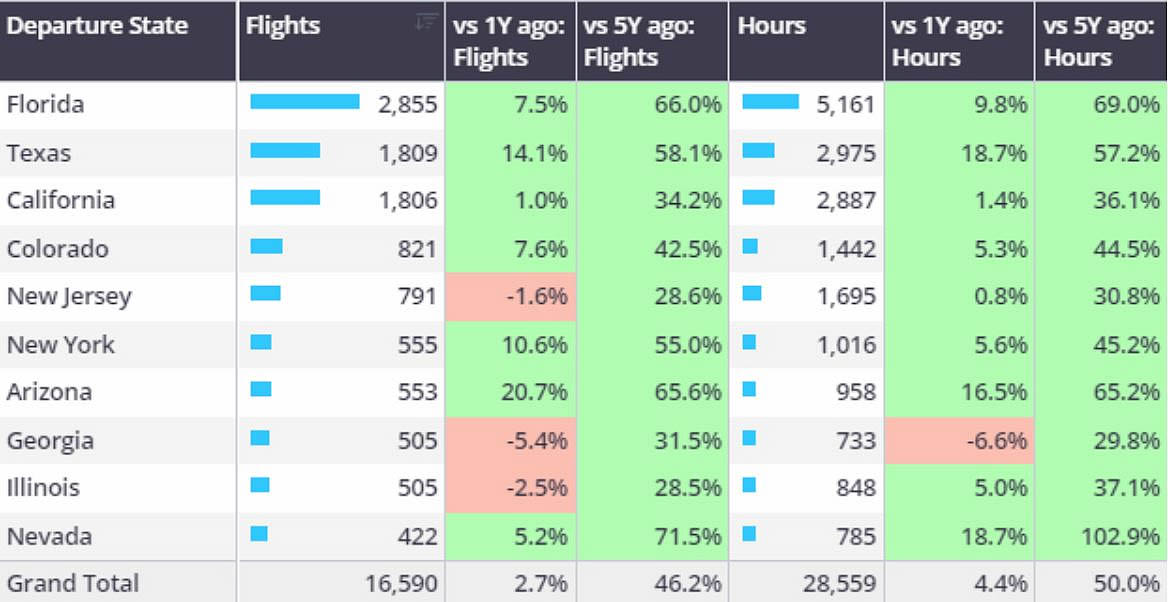

United States

In Week 10, 50,737 business jet sectors were flown in the United States, 9% ahead of the previous week, 2% ahead of Week 10 in 2023. The last 4-week trend for the US is 1% ahead of the same period last year.

So far this month, 69,321 bizjet sectors have departed US airports, 1% below March last year, 32% ahead of March 2019. Flight hours are on par with March last year, 37% ahead of March 5 years ago. Across the aircraft segments, demand is mixed at the start of this month. Entry level jets are flying less than any of the last 5 years, contrast Ultra Long Range and Super Midsize jets, flying more than the start of any March in the last 5 years. Several US states are seeing strong growth in Super Midsize activity this month, top state Florida 8% ahead of last year, 66% ahead of 2019. New Jersey has seen Super Midsize activity cool, sectors down 2% YoY. Corporate flight departments are flying 43% less than the start of March last year out of New Jersey, flights to Canada from New Jersey falling 17% compared to last year.

Chart 2: US Super Midsize departures and hours, 1st � 10th March 2024 vs previous years.

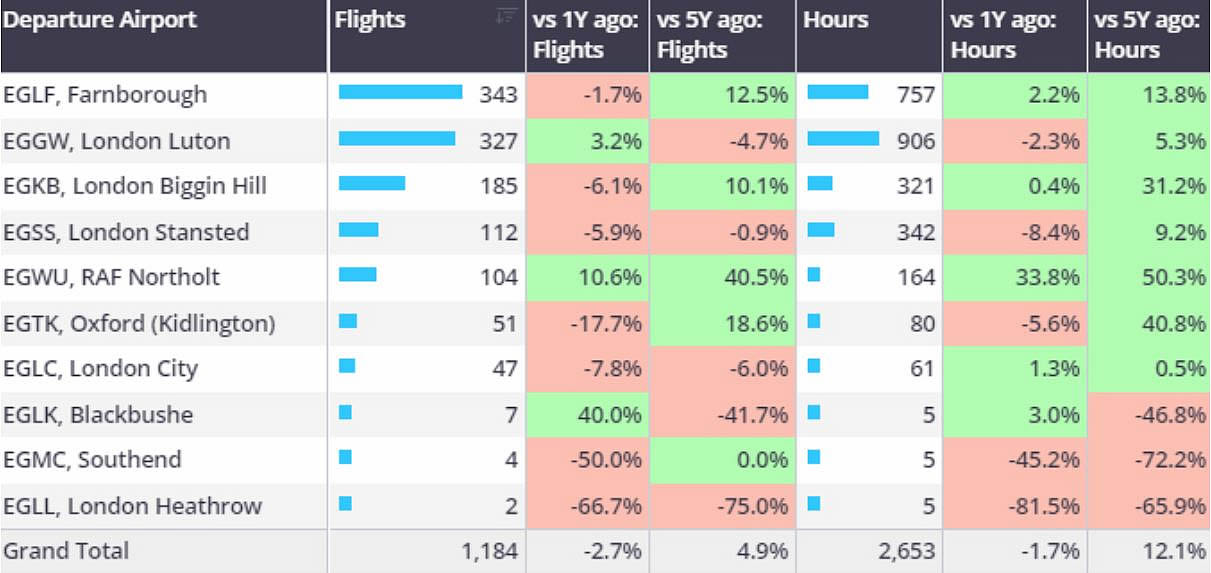

Europe

In Week 10, European business jet activity was on par with Week 10 2023, 5% ahead of Week 9 in 2024. The last four-week trend is trending 3% below the same four weeks last year. Year to date, European bizjet activity is 2% behind 2023, 2% ahead of 2019. London is the busiest departure city this month, activity is 3% behind last year, 5% ahead of 2019. Farnborough edges out as the busiest London bizjet airport this month, second ranked Luton seeing activity 3% ahead year-on-year. Fractional programmes are flying more sectors out of London than the start of any March in the last 5 years. France is the top fractional international connection from London airports this month, connections with Germany falling 17% YoY.

Chart 3: Business Jet departures from London airports 1st � 10th March 2024 vs previous years.

France is the largest domestic bizjet market this month, although activity has dropped 18% YoY. Nice � Le Bourget is the busiest domestic bizjet airport pair this month, activity ahead of the last 5 years. Le Bourget to Bordeaux�Mérignac Airport has seen activity drop 38% compared to March last year. Branded Charter fleets are flying more domestic routes than the last 5 years, private flight departments 39% less than last year.

Elsewhere bizjet activity in Italy is on par with the start of March last year, Malpensa, Pisa and Peretola airports seeing large gains on March last year. Connections with France are up 23% YoY, Switzerland up 17%. Contrast domestic bizjet sectors, down 5% YoY, connections with the UK down 1% YoY.

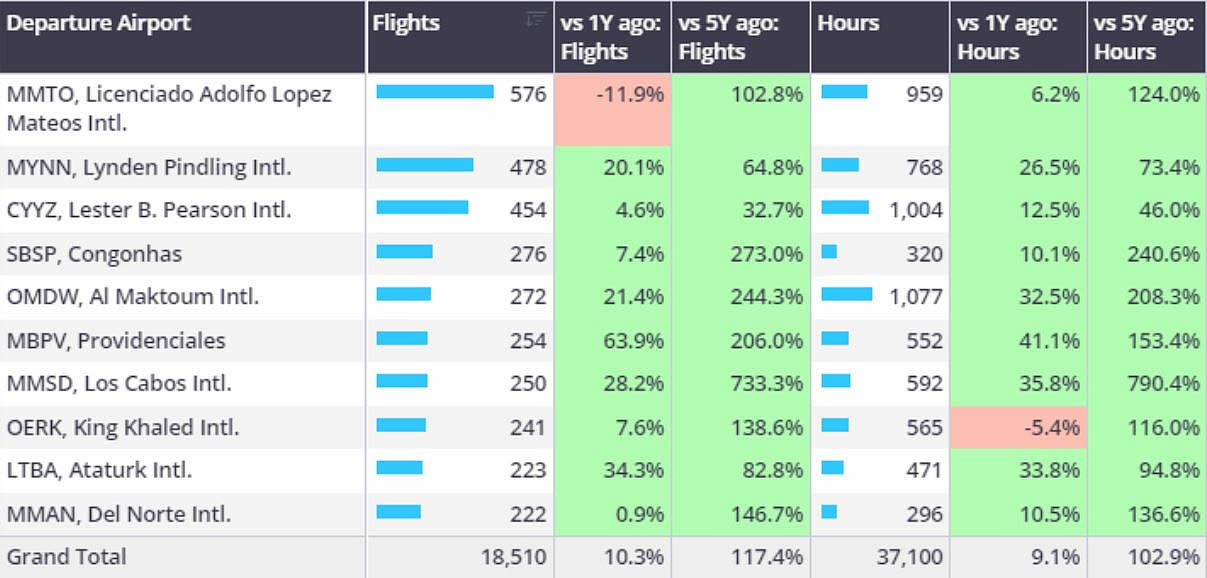

Rest of World

In Week 10, bizjet activity in the Middle East fell 6% compared to the previous week, 6% ahead of Week 10 in 2023. So far this month bizjet sectors in the Middle East are 9% ahead of 2023, 80% ahead of March 2019. At the start of this month the United Arab Emirates and Saudi Arabia are 4% and 7% ahead of last year respectively, in Saudi Arabia, King Abdulaziz International Airport (OEJN) saw 26 arrivals during the F1 Grand Prix weekend (7th � 9th March) last week. Elsewhere outside of Europe and the United States, India and China seeing strong gains on March 2023. Departures out of India are 92% ahead of 2023, departures out of China 126% ahead of last year.

Chart 4: Business jet departure airports, outside of Europe and United States, 1st � 10th March 2024 vs previous years.