Liberation Day and the associated enactment of global tariffs on imports into the US triggered market turmoil and expectations of a recession, but so far only a ripple in terms of declining flight activity, most notable in Florida. An uptick in transatlantic corporate flight department travel may have been linked to tariff policy changes. We shall have to wait to see impact in Europe as this week was affected by comparison with Easter holidays last year.

Global

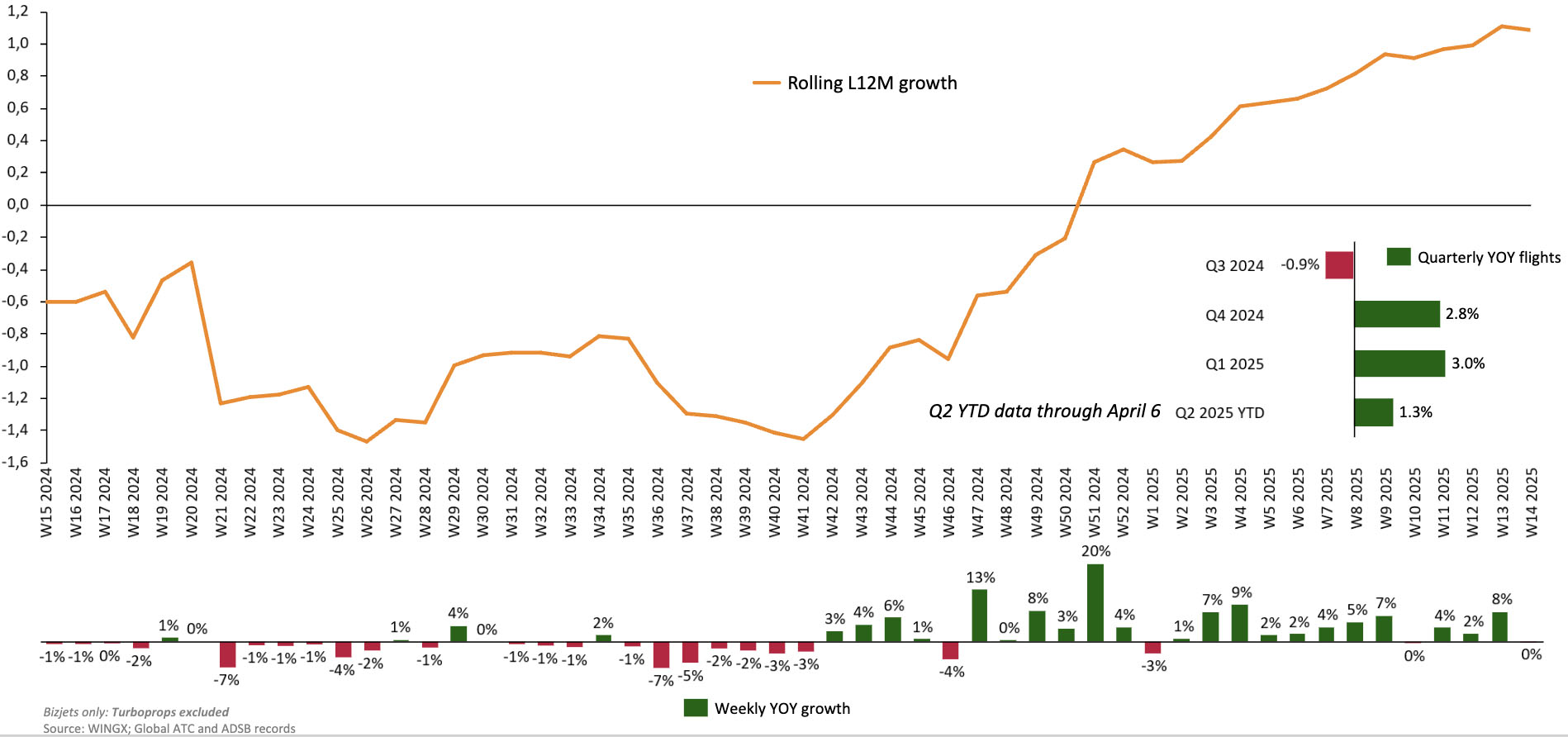

Between the date of the US presidential election in November 2024 and today, US business jet flights were up by 4%, compared to the previous years’ same period. However, Week 14 (31stMarch – April 6th), the week of Liberation Day, saw a 3% drop in bizjet travel compared to same Week in 2024. The global trend in bizjet traffic was flat overall. Bizjet activity in Europe was up 12% in Week 14, flattered by the comparison with the Easter Holiday in Week 14 2024.

Chart 1: Global business jet flights and rolling 12-month trends

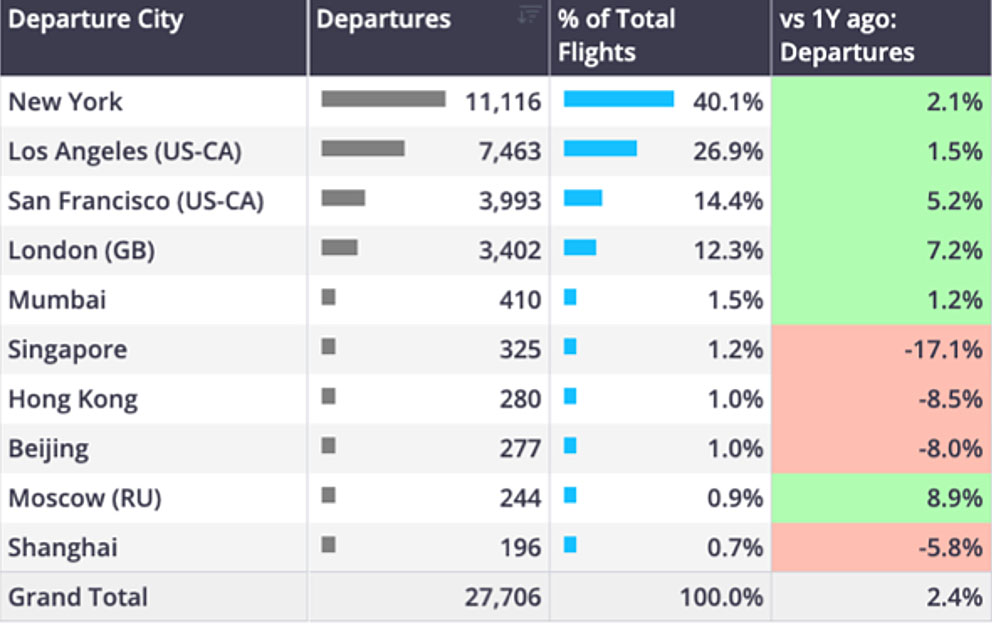

In the last four weeks (March 10th � 6th April), business jet departures from the 10 cities with the highest concentration of billionaires is up by 2%, varying from strong growth out of Moscow and London, whilst bizjet demand from Singapore has sagged almost 20%.

Chart 2: Business Jet departures from cities with highest concentration of billionaires, last four weeks (March 10th � 6th April 2025 vs previous years).�

North America

The hotbed of business jet activity since the pandemic, Florida, has seen a big drop-in flight activity in the week of ‘Liberation Day�, in Week 14, 5% fewer sectors flown from airports in Florida, in contrast to the 4% growth so far this year. In Week 14, downturns were most evident at West Palm Beach, departures down 32% compared to last year. Out of the operator types in West Palm Beach, Aircraft Management fleets fell the furthest, departures down 43% compared to Week 14 last year.

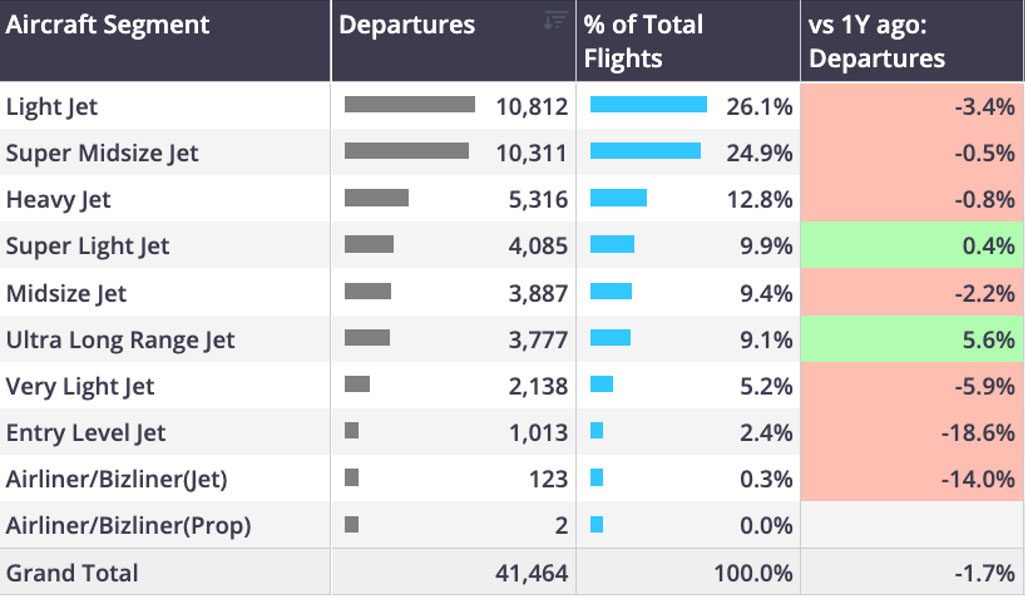

In terms of business jet segment across the US, there is still growth in Super Mid and Ultra Long-Range Jets, both flying more in the last 7 days. The biggest drops are at the top and bottom end of the scale, with Bizliner traffic down by 10% and Entry Level flight activity down 6%. Overall, the smaller aircraft segments are clearly losing demand this year.

There were 780 bizjet connections from the United States to Mexico, down 19% compared to Week 14 last year. Declines in flights to Mexico are mostly coming evident in Aircraft Management and Branded Charter fleets, US connections to Canada increased 8% compared to last year, and transatlantic flights to the UK grew 12% compared to last year. There was a notable increase in Corporate Flight activity on transatlantic connections between London and New York

Chart 3: US Bizjet departures by segments April 1st � 7th 2025 vs last year.

European Region

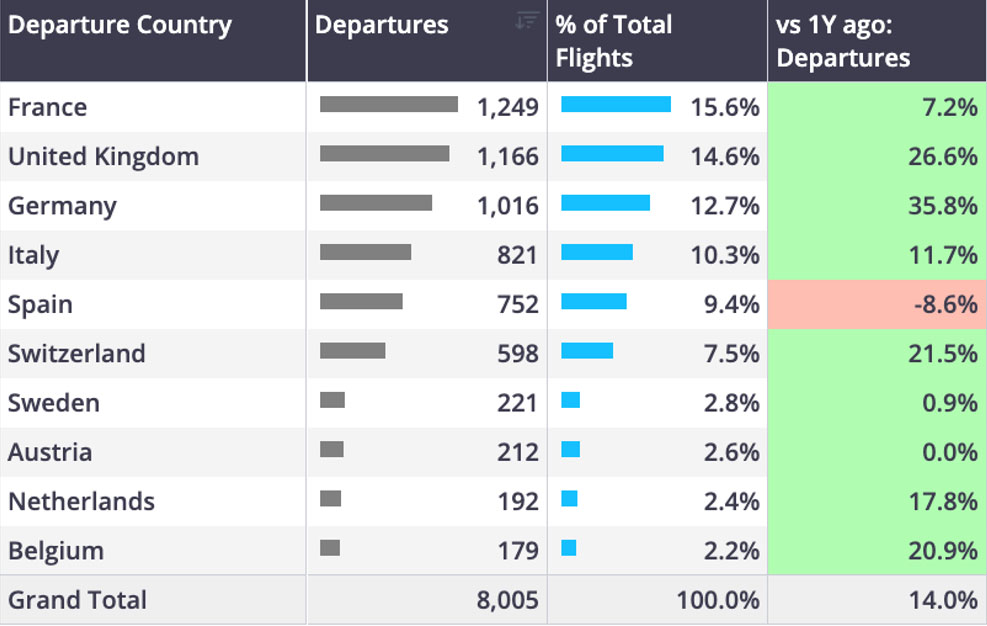

In Week 14 (31st March � April 6th), European bizjet activity grew 12% compared to Week 14 last year, streaking ahead of the last four-week trend which stands at just +2%. The trend is flattered by comparison with Easter holiday in Week 14 in 2024. This may explain why the largest YOY growth was evident in strong corporate markets like Germany (+31%), Switzerland (+20%) and the UK (+18%). In Germany, the strongest YOY growth was on domestic flights from Berlin, Hannover, Stuttgart and Frankfurt, with the Super Mid category particularly busy.

Chart 4: Business jet departures by European country, April 2025.

Rest of World

In Week 14, business jet activity outside of North America and Europe was up 8% compared to Week 14 last year. Middle East provided most of the boost, strong growth in flights in the Gulf countries, which may also reflect the differing Eid dates in 2025 and 2024. Brazil continues to be a strong business aviation market, bizjet sectors up 14% this year. Light and Midsize jets are providing the momentum. Business jet activity out of China were also up, 11% YOY in Week 14.