WINGX�s weekly Business Aviation Bulletin.

Summary

Business jet activity in Q1 2023 is only modestly down from Q1 2022 but the gap has increased in the last few weeks. This may reflect the surge in demand following the lifting of lockdowns in the US following the end of the Omicron wave last Spring. In Europe, a few countries are still seeing record activity, but the overall trend is downwards, with increasingly negative optics around emissions impacts from business jet usage.

Global

Worldwide business jet sectors in Week 13 of 2023, March 27th through April 2nd, amounted to 69,385 sectors, 1% more than Week 12, 6% fewer than the same dates in 2022. The global trend for the last 4 weeks is 7% below the same dates in 2022. Global Part135 and Part91k bizjet activity in week 13 was 13% down compared to the same dates in 2022.

Bizjet activity in Q1 of 2023 was down 4% compared to Q1 2022, 15% up compared to Q1 in 2019. Combined business jet and turboprop activity was 2% down compared to Q1 last year, 12% ahead of comparable 2019. Turboprop activity finished Q1 1% ahead of comparable 2022, 7% higher than 2019.

Chart 1: Global fixed wing flights, Q1 2023 compared to previous years. (Note business aviation includes jets and turboprops)

North America

In Week 13, 54,371 bizjet sectors departed North American airports, 2% more than Week 12, 8% fewer than the same dates last year. In the last four weeks activity is 9% down on the same dates last year. Part135 and Part 91K activity during week 13 was 3% above week 12, 13% fewer than the same dates in 2022. In Q1 P135/91k activity was down 11% compared to last year, still 37% above 2019.

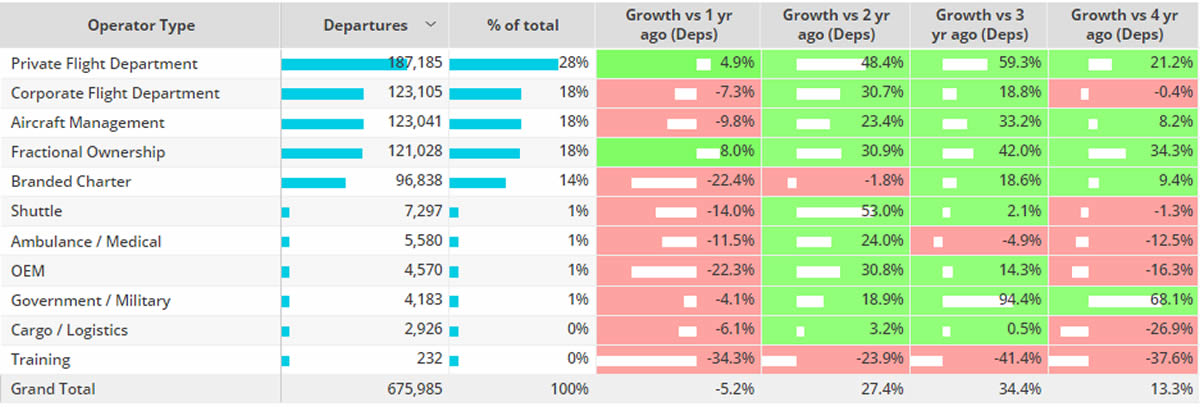

Business jet departures from North America in Q1 were 5% down compared to Q1 2022, 13% up compared to 2019. Light jets were the busiest aircraft segment in Q1, although departures were down 7% compared to 2022, 13% up compared to 2019. Super Midsize, Ultra-Long-Range Jets and Very Light Jets saw a growth in departures compared to Q122. Midsize and entry level jets are seeing declines compared to 2019. Teterboro was the busiest bizjet airport last quarter, although departures were down 1% compared to Q1 2022, down 3% compared to Q1 2019.

Chart 2: North American bizjet flights by operator type, Q1 2023 compared to previous years.

Europe

In Europe, 9702 bizjet sectors were flown in week 13, 1% more than in week 12, 4% fewer than the same dates in 2022. In the last four weeks activity is 5% below the same dates in 2022.

Business jet departures from Europe in Q123 were 8% down compared to Q1 2022, 5% ahead of comparable 2019. Excluding Russia and the Q1 trend was 5% down compared to 2022, 9% ahead of 2019. Light jets were the busiest aircraft segment in Q1 of 2023, departures down 10% compared to 2022, although still 6% ahead of comparable 2019. Across the aircraft segments demand was mixed in Q1, Heavy jets, entry level jets and Bizliner departures were behind 2019, although Super Light, Very Light and Midsize jets saw double digit growth compared to 2019.

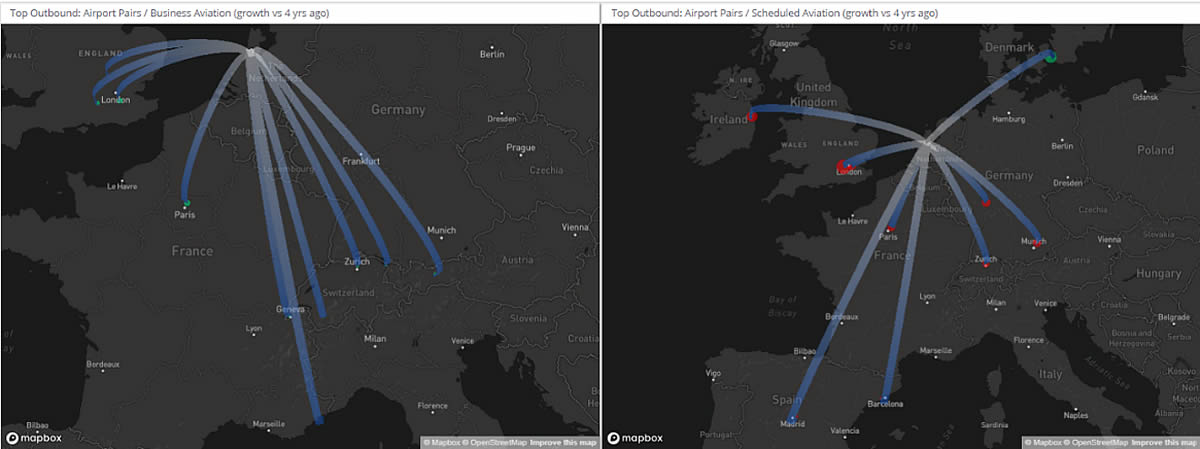

Bizjets out of Schiphol accounted for 3% of all departures in Q123 this year, departures were up 8% compared to last year, 38% ahead of 2019. In contrast, Schiphol airport saw 19% fewer scheduled airline flights in Q123 compared to Q1 in 2019, 13% more than last year. Bizjet flights from Amsterdam to London airports are up 80% compared to 2019, whereas the scheduled connections from Amsterdam to London are down 27%. Overall, 56% of scheduled airline departures were less than 90 minutes in length, 76% of bizjets flew under 90 minutes from Schiphol.

Chart 3: Business jets vs Scheduled airlines, Amsterdam Schiphol airport Q1 2023.

Rest of World

In Week 13 of 2023, March 27th through April 2nd, bizjet flight activity in Africa was 4% down compared with the same dates last year, Asia down 3%, Middle East down 30% and South America up 15%. In the Rest of World region there have been just under 67,000 business jet sectors in Q1, 20% more than 2022, 77% more than 2019. Brazil was the busiest market in Q1, 17% ahead of last year, triple digit growth compared to 2019. China saw bizjet sectors dip 5% behind Q1 of 2019, 31% above last year. Private flight departments generated 70% of sectors. Beijing Capital was the busiest departure point, departures up 23% compared to last year, although 44% below 2019. Ultra-long-range jets were the busiest aircraft segment, flights up 28% compared to last year, although lagging 26% behind 2019.