WINGX�s weekly Business Aviation Bulletin.

Summary

With the gap closing between commercial airline activity in 2023 and 2019, business aviation trends are moving in the other direction, with just under 10% gain in April 2023 versus April 2019. In the US, fractional operators are still hitting record levels of activity. In Europe, bizjet flights out of Germany and Austria are now trending well below 2019 levels, and activity in France is now flat compared to 4 years ago. Other countries inside and outside Europe, including Spain, Italy, Turkey, UAE, Israel, are still seeing strong gains in bizjet activity compared to 2019.

Global

In Week 16 Global business jet activity fell 2% compared to Week 15, 6% fewer than the same dates in 2022. In the last four weeks activity is 8% below the same dates last year. So far this month, 1st – 24th April, business jet and turboprop sectors are 7% below last year, 9% ahead of 2019. Over the same period scheduled airlines flew 1.6 million sectors, 16% more than 2022, although 14% below 2019. Focussing on business jets, sectors are down 9% compared to last April, 13% ahead of 2019. So far this month the top 5 busiest global airlines are Southwest Airlines, American Airlines, Delta Airlines, Ryanair and United. Departures of these airlines are up 12% compared to last year, 5% above 2019.

Chart 1: Global fixed wing flights, April 1st � 24th 2023 compared to previous years. (Note business aviation includes turboprops)

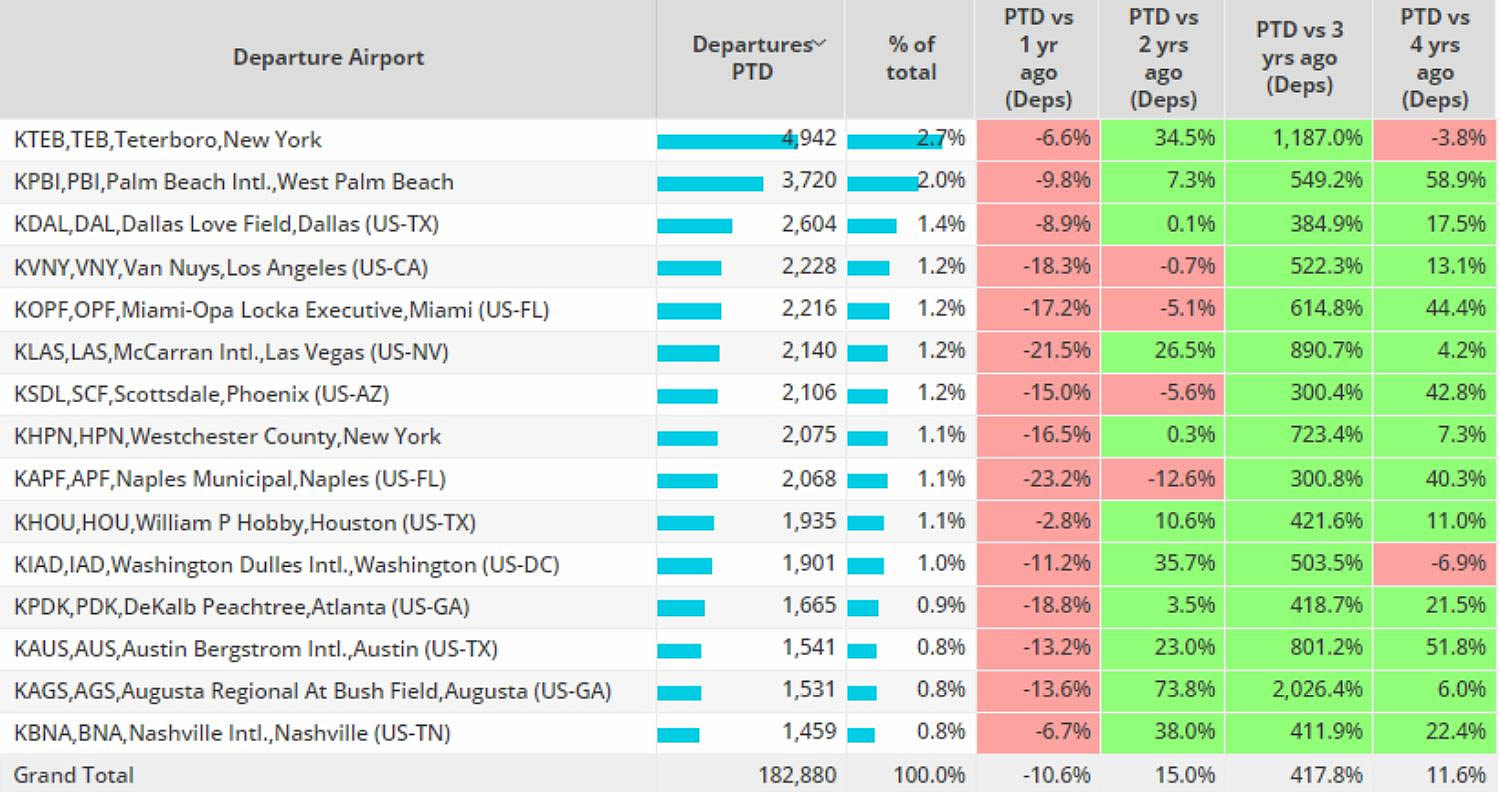

North America

US bizjet departures are down 11% compared to last April, although well ahead of 2019, departures up 14%. Mexico is the second busiest market this month, departures are down 7% compared to last year, 37% below 2019.

Light jets are the busiest aircraft segment this month, although departures are down 9% compared to last year, 13% ahead of 2019. Heavy, Midsize and Entry level jets have seen activity in decline compared to 2019, Very Light Jets the only type to see growth compared to last year.

Trans-Atlantic (North America � Europe), bizjet sectors have fallen 1% compared with April 2022, although 18% ahead of 2019. Teterboro is the busiest departure point for Trans-Atlantic bizjet flights, flights are up 2% compared to last month, 11% ahead of 2019. United States � United Kingdom is the busiest Trans-Atlantic country flow, flights are up 7% compared to last April, 32% ahead of 2019. Elsewhere flights between the United States and France are down 9% compared to last year, Italy up 7%, Ireland down 8%.

Chart 2: North American bizjet airports, April 1st � 24th 2023 compared to previous years.

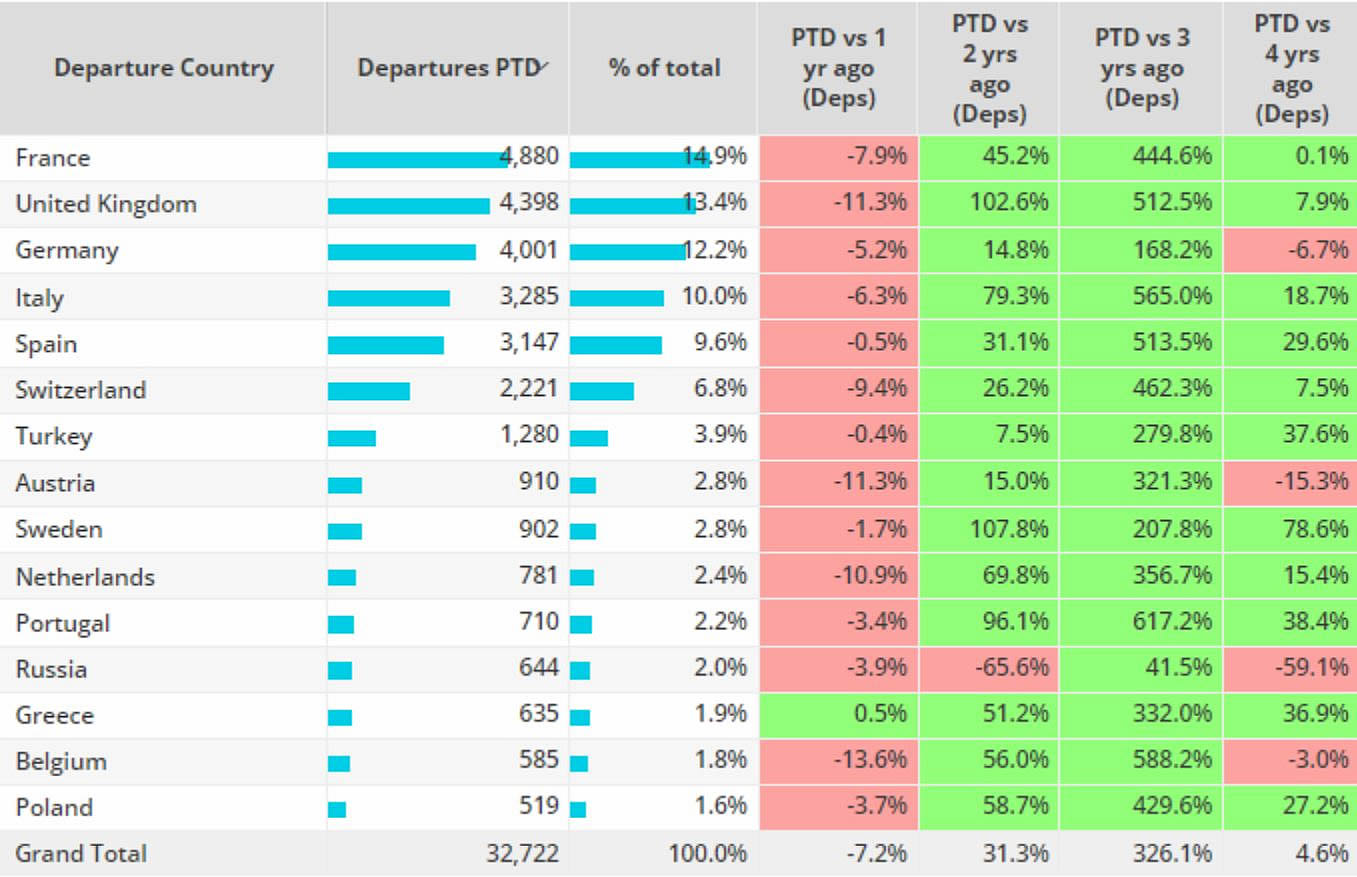

Europe

In Week 16 European bizjet sectors grew 9% compared to Week 15, 2% below the same dates last year. In the last four weeks activity has fallen 6% behind the same dates last year. Despite departures falling 11% compared to last April, Le Bourget is the busiest airport in the region, departures are up 3% compared to 2019. Elsewhere departures from Nice are up 3% compared to last year, 12% ahead of 2019. Geneva is seeing a 12% drop compared to last year, Milan Linate up 20%.

The only aircraft segments this month to see growth compared to last April are Ultra-Long-Range jets, flights of these aircraft types are up 2% compared to last year, up 5% compared to 2019. Bizliners are still way behind pre-pandemic activity levels, sectors down 61% compared to April 2019, down 11% compared to last year. Light jets are the busiest aircraft segment in Europe this month, although departures are down 8% compared to last year, 8% ahead of 2019.

Chart 3: Top European Business Jet Markets, April 1st � 24th 2023 compared to previous years.

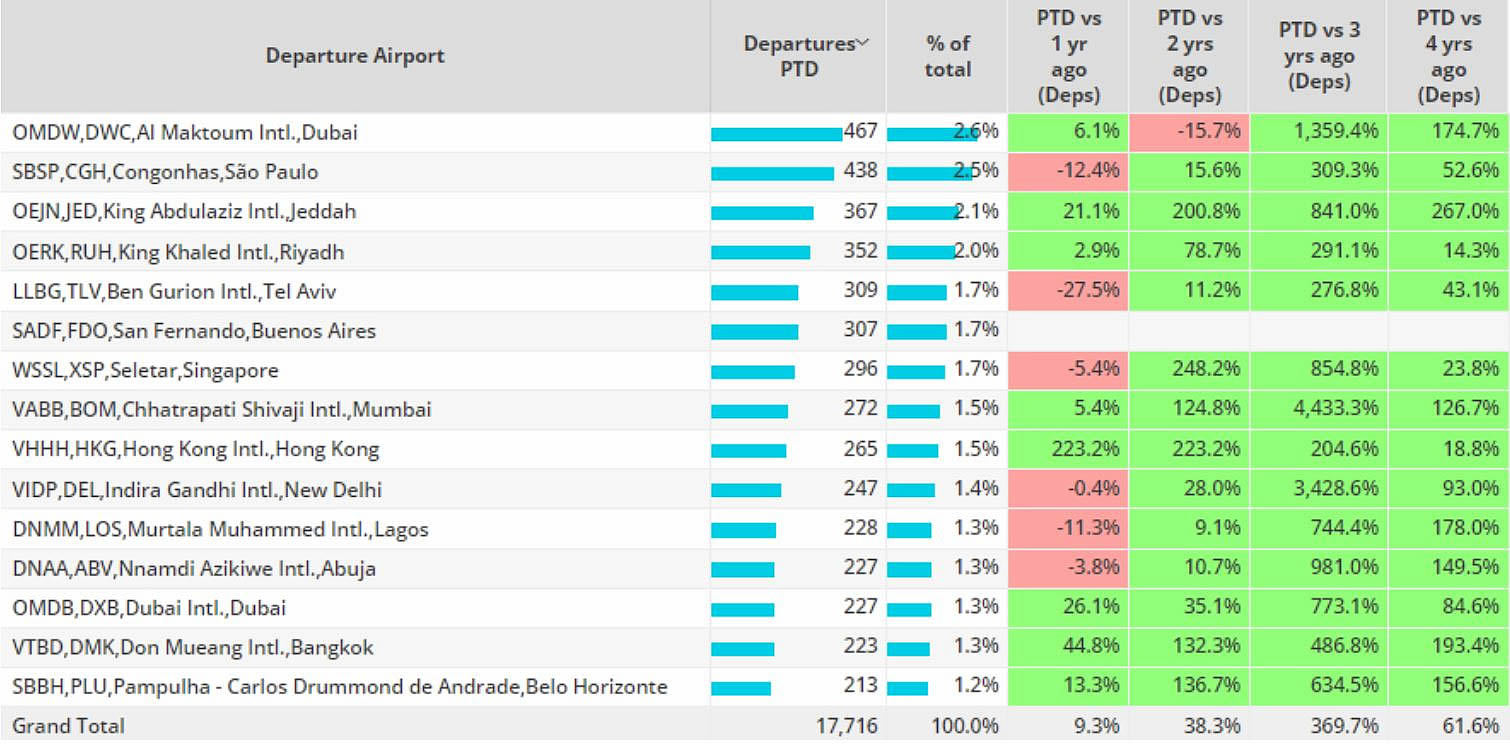

Rest of World

In Week 16 bizjet departures in Africa were up 11% compared to 2022, Asia up 9%, South America up 15%, Middle East down 6%.

Brazil remains the busiest Rest of World market so far this month, departures up 5% compared to last year, triple digit growth compared to 2019. Australia and India have seen sectors fall compared to last year, although still well ahead of 2019. Departures from the United Arab Emirates are up 6% compared to April last year, 81% ahead of 2019.

China is seeing triple digit growth in bizjet departures compared to last year, although activity remains 5% behind 2019. The Bombardier Global 6000 series is the busiest type this month in the country, departures are up 260% compared to last April, 43% ahead of 2019. Other types seeing triple digit growth compared to last year are the Gulfstream G600/650, Challenger 800/850, Dassault Falcon 8X and the Gulfstream G400/450.

Chart 4: Top Rest of World airports, bizjets, 1st � 24th April 2023 vs previous years.